Financial incentives play a large role in retirement decisions

Courtney Coile of Wellesley College finds that the availability of Disability Insurance encourages early retirement, particularly for those in poor health or with low education. Coile suggests that if medical screening for Disability Insurance were tightened significantly so that two-thirds of applicants were denied benefits, the labor supply of the applicant pool would increase by roughly 10%.

Increased public employment does not reduce the unemployment rate in the long run

In an examination of 24 middle-income countries, Ara Stepanyan and Lamin Leigh of the International Monetary Fund conclude that increased public employment does not lower the unemployment rate in the medium- or long-term, and may even do the opposite. They find that an increase in public employment induces people to acquire skills that are not demanded by the private labor market, and that a significant crowd-out effect exists: for every 100 public sector jobs created, roughly 70 private sector jobs are destroyed.

Nominal GDP targeting a viable alternative to inflation targeting in some developing countries

Pranjul Bhandari and Jeffrey A. Frankel of Harvard University argue that a nominal GDP target could be more beneficial than an inflation target for some developing countries. The authors explain that with nominal GDP targeting, the impacts from a supply shock are split between inflation and real GDP growth, whereas with inflation targeting, the impacts all fall on real GDP growth. As a result, policymakers can avoid making excessively tight (or loose) monetary policy responses to supply shocks.

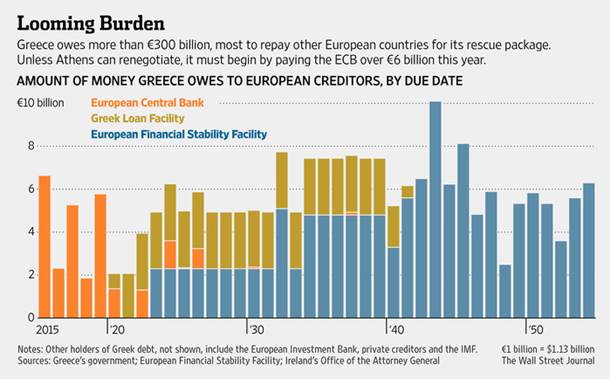

Chart of the week: Greek Debt

Quote of the week: European Central Bank doesn’t expect deflation, but the risk is real

Can the risk of deflation be regarded as real at present?

“We are not expecting deflation, but there are risks that need to be addressed. Prevention is better than cure. That is why we had to take action before the damage is done, because the inflation expectations of consumers and businesses are falling. That is dangerous. Also, a period of low inflation that is too prolonged entails significant risks.”

– Peter Praet, Member of the Executive Board of the European Central Bank

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Hutchins Roundup: Disability Insurance, Public Employment, and More

February 5, 2015