The working paper underpinning this article, “Building the SDG economy,” was published in October 2019 and can be accessed here. It includes some minor updates to the results described below.

Pouring several colors of paint into a single bucket produces a gray pool of muck, not a shiny rainbow. So too with discussions of financing the Sustainable Development Goals (SDGs). Jumbling too many issues into the same debate leads to policy muddiness rather than practical breakthroughs. Financing the SDGs requires a much more disaggregated mindset: unpacking the specific issues, requiring specific resources, in specific places.

In a forthcoming paper, we zoom out on the global SDG financing landscape in order to zoom back in on country-specific contexts and gaps. In particular, we consider how much the world’s governments are already spending on SDG-related issues every year, how spending varies across income levels, and how the spending patterns link to country-by-country estimates of needs. We focus on the public sector due to its lead responsibility for tackling both the public goods and the “no one left behind” issues embedded in the SDGs and the 2015 Addis Ababa Action Agenda on financing for development, the latter including a “social compact” commitment to provide universal access to basic services. This research can be considered as complementary to assessments of where the private sector can best contribute to SDG financing. Below we summarize some preliminary findings, noting that all results are subject to refinement as we complete the analysis.

1. Global public sector SDG spending is already more than $20 trillion per year

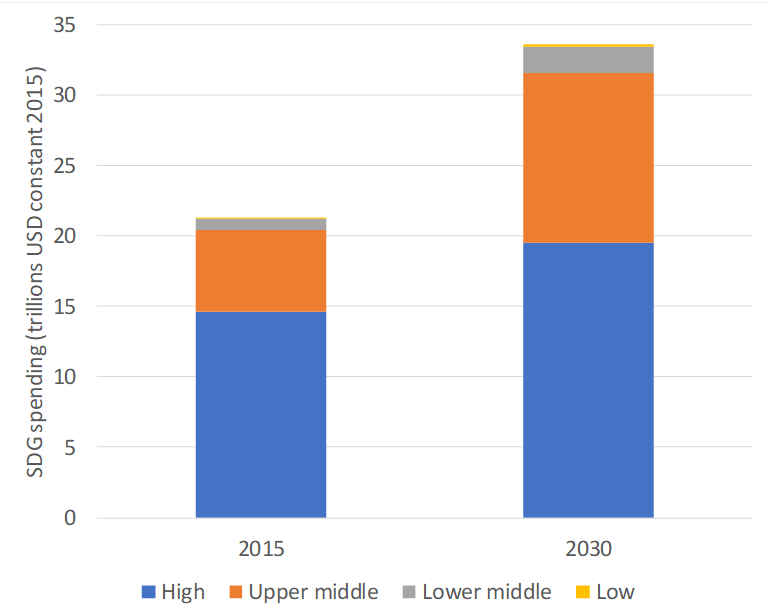

Our first key finding is that, as of 2015, governments around the world were already spending approximately $21 trillion per year on SDG-related sectors: health, education, agriculture, social protection, infrastructure, justice, and conservation. If recent global economic trends continue under a business-as-usual scenario, SDG-related public spending (hereafter described more simply as “SDG spending”) likely reaches $33 trillion or more by 2030, in constant dollar terms. In other words, global SDG spending in the public sector alone will grow by around $12 trillion per year, simply through the world’s ongoing processes of economic growth.

Does this extra $12 trillion per year of SDG spending tell us anything about prospects for SDG achievement? Not at all. The global aggregates are about as useful as tracking world rainfall totals when trying to grow a plant in the Sahel. First of all, as Figure 1 shows, the majority of current global SDG spending is taking place in high-income countries, telling us very little about how well each dollar is linked to SDG outcomes in each of those countries, and telling us even less about financing adequacy in lower-income countries. Second, a majority of the SDG spending growth out to 2030 is likely to take place in fast-growing upper-middle-income countries (UMICs), but this again tells us little about how the new resources might shape better SDG outcomes in those places, or what will generate outcomes in less economically prosperous places.

Figure 1: Public Spending by country income group on SDG-related sectors, 2015 and 2030

Source: Authors’ calculations, based on: FAOSTAT (2017) and IFPRI SPEED (2015) (agriculture); UNESCO (2018) (education); WHO (2015) (health); ILO World Social Protection Report (2019) (social spending); IMF Investment and Capital Stock database (2017) (infrastructure); PNAS (2008) (biodiversity); IMF Governance Finance Statistics (2016) and UNStats (2017) (justice)

In lower-middle-income countries, we estimate that total SDG spending will increase from around $780 billion in 2015 to more than $1.9 trillion in 2030. This is spread across a population likely to grow from 2.9 billion people to 3.5 billion people over the same period, equivalent to a growth in per capita spending from around $265 to around $530. Meanwhile, in low-income countries (LICs) with even faster population growth, we estimate that SDG-related spending will increase from only around $70 billion in 2015, roughly $115 per capita, to almost $180 billion in 2030, roughly $210 per capita. This per capita figure works out to a steady 4 percent annual growth rate in the LICs.

Altogether, these numbers indicate considerable growth in SDG spending across income levels. But the huge variations in orders of magnitude also underscore how little the multitrillion-dollar growth in global annual SDG spending aggregates mean, for instance, in the world’s poorest countries.

2. SDG spending rises proportionately with GDP per capita

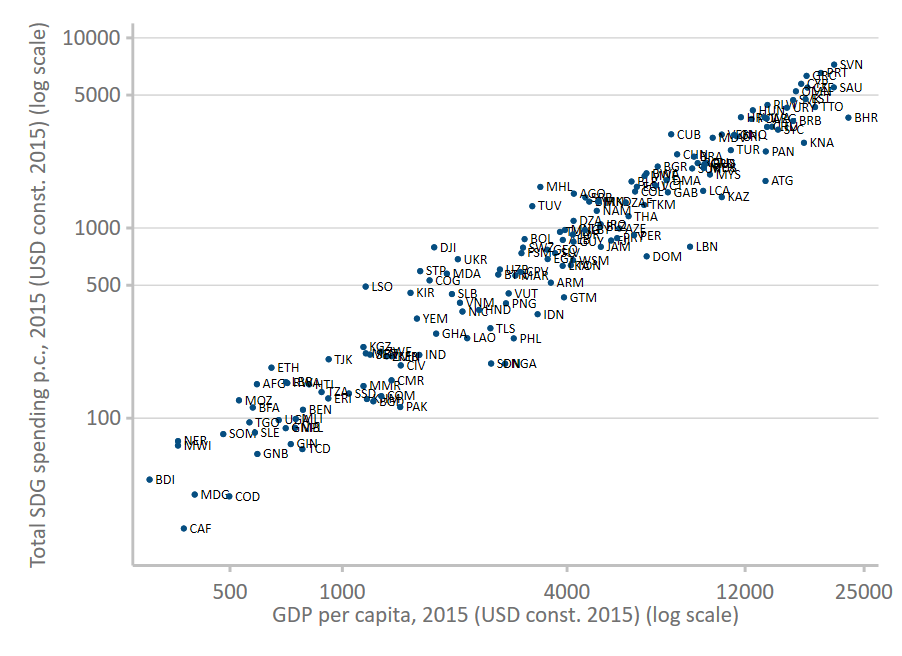

Delving a layer deeper, our research draws attention to the limits even of considering averages by country income category. As shown in Figure 2, there is a clear relationship between public SDG spending and GDP per capita. For every dollar of higher income, countries have, on average, a correspondingly higher level of average SDG spending. Importantly, when drawing a line through the cross-section, its slope is greater than one, suggesting that SDG spending rises faster than GDP per capita. For every 10 percent higher level of average GDP per capita, we find average SDG spending to be 13 percent higher.

Figure 2: Estimated SDG public spending per capita, 2015

Source: Authors’ calculations, based on: FAOSTAT (2017) and IFPRI SPEED (2015) (agriculture); UNESCO (2018) (education); WHO (2015) (health); ILO World Social Protection Report (2019) (social spending); IMF Investment and Capital Stock database (2017) (infrastructure); PNAS (2008) (biodiversity); IMF Governance Finance Statistics (2016) and UNStats (2017) (justice)

3. Minimum SDG spending needs are approximately $300 per capita

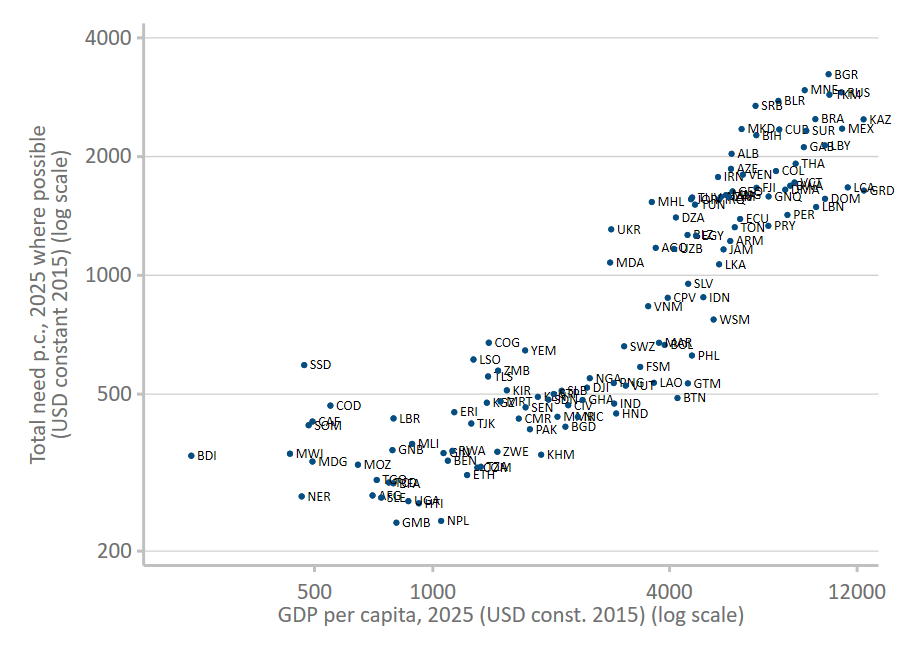

We next turn to a bottom-up, country-by-country estimation of minimum public spending needs for achieving the SDGs. This is in the spirit of the commitments for universal access to basic services embedded in both the SDGs and the Addis Ababa agreement. Specifically, we synthesize results from a variety of other studies that have considered public sector resource requirements for 10 distinct sectors: health, education, agriculture, flood protection, energy systems, transport infrastructure, social assistance, conservation, water and sanitation, and justice. Again, this is not meant to imply that spending equals results; it is only meant to help address the underlying reality by which a universal package of basic services, which countries promised to deliver in Addis Ababa, requires a minimum amount of appropriately targeted resources. We do not assess the quality or precision of each underlying study’s results, some of which are more tailored to specific country conditions than others, although we do make an effort to avoid double-counting across estimates. For example, we aim to ensure the road infrastructure needs are only included in the transport sector and subtracted from the estimated requirements for rural agriculture.

In this spirit of indicative estimates, Figure 3 shows minimum public SDG spending needs for all developing countries, plotted against GDP per capita. (The figure excludes high-income countries, for which the cross-country estimates of SDG-relevant spending needs are not available, and arguably not relevant.) Estimates are presented in log scale, and hence represent proportionate changes on both axes. Notably, the figure shows something of a flat slope at low income levels and then a steep slope at higher income levels. The flat portion is at an average needs estimate of around $270 to $350 per capita for LICs, although countries like Gambia and Nepal have the lowest per capita needs estimates at around $235. Then, as countries get richer, prices rise, the cost of providing social services rises, systems and networks must be maintained, and demand increases for higher quality services, all of which leads to greater overall spending.

Figure 3: Estimated minimum SDG public spending needs in 2025

Source: Authors’ calculations, based on: Achieving Zero Hunger (2015) (agriculture); The Learning Generation (2016) (education); Stenberg et al. (2017) (health); Fay and Rozenberg (2019) (energy, flood insurance, transport); Government Spending Watch (2018) and Hutton and Varughese (2016) (WASH); McCarthy et al. (2012) (biodiversity); Manuel et al. (2019) (justice)

4. Financing gaps vary by income level and by country

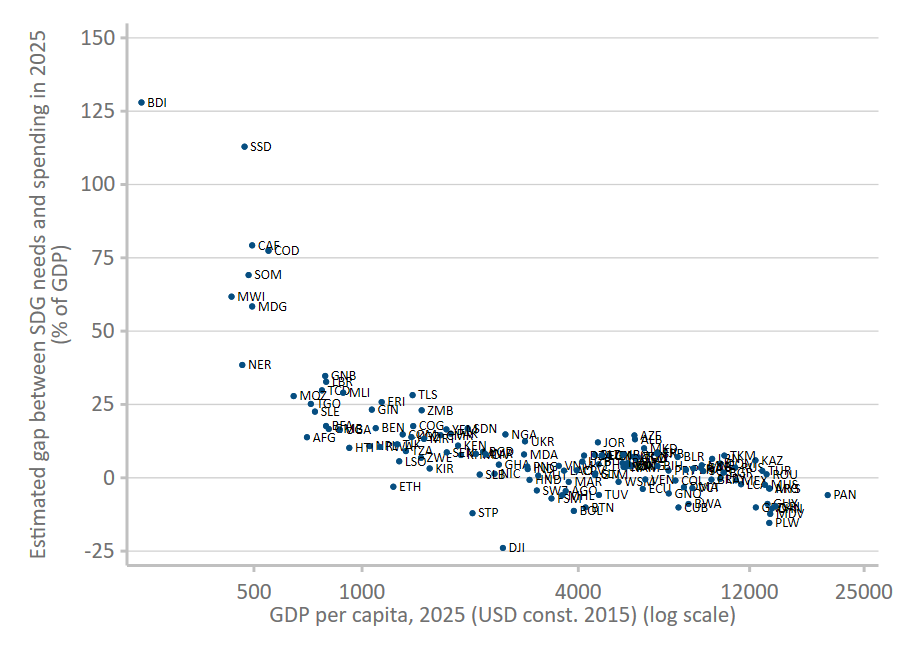

When we compare minimum spending needs with actual spending, the dimensions of the problem facing developing countries become even clearer. The lowest-income countries tend to have the most significant SDG financing gaps, defined as the difference between spending and minimum needs. Figure 4 shows the estimated gap for each country in 2025, as a share of GDP, if recent trends in economic growth continue and countries continue to spend a constant share of national income on SDG-related sectors. At the top left of the plot, Burundi and South Sudan have estimated per capita gaps of approximately $310 and $530, respectively, equivalent to more than 100 percent of GDP per capita in those countries. Notably, all countries with GDP per capita of $1000 or less in 2025 show gaps equal to 10 percent of GDP or more.

Looking downward and to the right along the scatterplot in Figure 4, many countries show a gap of less than zero. This should not be interpreted as “overspending,” but instead only as an indication that each country’s projected 2025 spending is estimated as adequate to cover at least minimum thresholds for basic SDG-related services. Importantly, countries like Ethiopia, Bolivia, and Bhutan fall into this category, as do many UMICs. It’s also very possible that countries near or below the zero line would benefit from a focus on better spending rather than more spending, although that topic is beyond the realm of the present study.

Figure 4: Estimated SDG financing gaps in 2025

Source: Authors’ calculations

When we add up all the country-level public sector gaps above the zero line in Figure 4, the sum works out to approximately $1 trillion per year—including around $150 billion in LICs, around $600 billion in LMICs, and around $250 billion in UMICs. This amount is slightly lower than what has been found by others (Gaspar et al. 2019; UNCTAD 2014; Schmidt-Traub 2015) and is again meant to be interpreted as indicative rather than a point estimate. But it is still a sobering gap, especially for LICs, when viewed against a recent backdrop of falling external assistance to the least developed countries in particular. Nonetheless, we believe there are opportunities that, taken together, would make a significant dent in the financing gap.

5. Three substantial opportunities to fill the financing gaps

There are three major prospects to help countries fill their SDG financing gaps, although each comes with its own issues to be resolved. The first is to increase domestic resource mobilization (DRM). The IMF has suggested that developing countries could raise 3-5 percentage points of GDP in DRM. We estimate that if countries with SDG financing gaps increase DRM by up to this amount (i.e., by applying DRM increases up to the level of a likely gap), the added financing sums to a notable $500 billion per year. However, aggregates are again potentially misleading, since the gap sums across a diverse cross-section of country circumstances. A simple breakdown by income groups shows that an incremental gap-filling percentage point of GDP in additional DRM will raise approximately $5 billion for LICs, $95 billion for LMICs, and $60 billion for UMICs in 2025. In other words, most of the aggregate DRM potential lies in populous LMICs with sizeble financing gaps, not in LICs.

A few initiatives such as the Base Erosion and Profit Shifting agenda being pursued by the OECD, the efforts to address taxation of mining companies, clampdowns on tax evasion, and strengthening of domestic tax systems through the Addis Tax Initiative, are all promising. Many of these measures would help address the problem of illicit financial flows that are a contributing factor to a number of countries’ financing gaps. But we would also sound a word of caution. Fiscal systems in many developing countries are often regressive, in the sense of poor people paying more in taxes than they receive in subsidy equivalents. Relying more heavily on fiscal mechanisms to achieve the SDGs therefore requires both an improved effort to raise taxes as well as a major structural overhaul of taxes and subsidies. Absent this, it can simply lead to “fiscal impoverishment,” to use a term coined by Nora Lustig and colleagues at the Commitment to Equity Institute.

Related Books

A second opportunity is to make good on aid commitments, starting with full replenishments of the eight international agencies that are seeking donor support in the next 18 months or so. Pledges to these agencies in the previous round totaled $70 billion. This time, a concerted effort must be made to build the level of ambition towards what is needed to achieve the SDGs, rather than simply to replicate past pledges. Given ongoing improvements in aid effectiveness and newfound determination to end the scourge of failed states, now is the time for new global leadership on aid. In 2018, only five OECD countries met the commitment to deliver 0.7 percent of gross national income in aid: Denmark, Luxembourg, Norway, Sweden, and the United Kingdom. If all high-income countries make good on the same pledge, it would add about $200 billion to development finance. If directed toward financing gaps in countries with the greatest need, this could make a major dent in generating progress for the SDGs.

A third opportunity is to make better use of the multilateral development bank (MDB) system, and, more broadly, of non-concessional official flows. MDBs have long been constrained by credit rating assessments that fail to understand their unique situation of preferred lender status provided by borrowers, combined with callable capital guarantees from rich countries. If shareholders permit, and indeed encourage, MDBs to take on more risk, then, using new rating models now being developed by S&P and others, a significant volume of lending could be unlocked—$1.4 trillion according to one study by the Banca d’Italia. With their ability to mitigate risk through policy reform, project identification, and an ability to scale by mobilizing private capital, the MDBs have the potential to make contributions to the financing gap for sustainable infrastructure in particular. But this will require heightened transparency for assessment of large projects and a new approach to considering projects in countries with high debt levels, especially if those projects contribute to improved creditworthiness.

These are of course only three of the big opportunities at hand. In 2019, four years after the launch of the SDG and Addis Ababa agreements, there is a time-sensitive need to revive ambitions around targeted public spending on specific SDG-related priorities. We hope to help raise sights by encouraging the unpacking of big headline global figures into more practical operational gaps—country-by-country and sector-by-sector. Resources need to be targeted and specific, often accompanied by substantive reforms. Authorities in developed countries, developing countries, and multilateral institutions all have a responsibility to make breakthroughs in the SDG financing agenda.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

How much does the world spend on the Sustainable Development Goals?

July 29, 2019