This post was originally published in March 2023 and has been updated to reflect ongoing developments.

What is deposit insurance?

Deposit insurance is the government’s guarantee that an account holder’s money at an insured bank is safe up to a certain amount, currently $250,000 per account. Deposit insurance is provided by the Federal Deposit Insurance Corporation (FDIC), a government agency that collects fees—insurance premiums—from banks. The FDIC is overseen by a five-member board—three nominated by the president and confirmed by the Senate, plus the Comptroller of the Currency and the director of the Consumer Financial Protection Bureau.

Deposit insurance, created during the Great Depression in 1933, has sharply reduced the frequency of bank runs that once were common in the U.S. As former Federal Reserve Chair Ben Bernanke explained in his 2022 Nobel Prize speech, about 40% of all U.S. banks disappeared between 1929 and 1933: “They failed, closed, or were absorbed by other banks. That happened because there were massive runs, bank runs, where people lost confidence in the banks and pulled out their money … The ones that were closed couldn’t make loans, obviously, and the ones that survived became extremely cautious being very reluctant to make loans.”

“Shortly after [Franklin Delano Roosevelt] became president, he called a bank holiday and all the banks had to shut down, and he promised the American public that they wouldn’t open up until the government had inspected them and was confident that they were in viable condition. And then the Congress passed deposit insurance, so that small depositors would be guaranteed that even if their bank failed, the government would pay them off. And that led instantaneously to a stabilization of the banking system. And that, of course, as the banking system became workable, that led to, helped lead to recovery.”

How much of an individual bank account is covered by insurance?

By law, up to $250,000 is insured for each depositor’s account in each bank. Congress raised the limit from $100,000 to $250,000 temporarily in 2008 and made the increase permanent in 2010. For most Americans, deposit insurance is more than enough to insure all money in their checking and savings accounts. However, businesses and other large organizations may hold over $250,000 at a given time. As of March 31, 2025, about 39% of all bank deposits were uninsured, according to the FDIC.

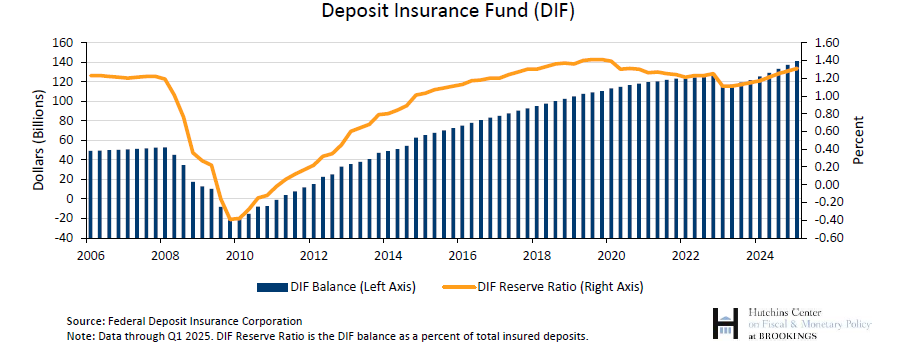

How is the FDIC funded?

The FDIC receives no appropriation from Congress, although it is backed by the full faith and credit of the U.S. government. Instead, the agency is funded by insurance premiums paid by banks and from interest earned on the FDIC’s Deposit Insurance Fund, which is invested in U.S. government obligations. The banks’ premiums depend on the size of the bank and bank regulators’ assessment of the riskiness of the bank.

As of March 31, 2025, the Deposit Insurance Fund had $140.9 billion, or about 1.31% of all insured deposits. The FDIC is gradually increasing premiums to bring the ratio up to the statutory minimum of 1.35% by September 30, 2028. Its target is to get the Fund up to 2% of insured deposits over the long run to “reach a level sufficient to withstand a future crisis.”

What does the FDIC do when a bank fails?

When a bank fails, the FDIC basically has two options. The first is to sell the bank to a willing buyer, which may take a portion or the entirety of the failed bank’s assets and liabilities. The second is to pay off the insured deposits and liquidate the failed bank’s assets, with uninsured depositors recuperating money based on the value of the assets. (To read FDIC Chair Martin Gruenberg’s description of this process, click here.)

When Washington Mutual failed in 2008 and was sold to JPMorgan Chase, uninsured depositors (who accounted for 24% of total deposits) got all their money. But when IndyMac failed, also in 2008, uninsured account holders recovered 50% of uninsured deposits. Even so, IndyMac was the costliest failure in the FDIC’s history—a $12.4 billion hit to the Deposit Insurance Fund. Since 1991, the FDIC has been required to choose the resolution method least costly to its Deposit Insurance Fund—unless the FDIC and other regulators declare that the least-cost option poses a systemic risk (see below).

On March 19, 2023, the FDIC said it sold substantially all the deposits, the branches, and some of the loans of failed Signature Bank to Flagstar Bank of Hicksville, New York. The FDIC estimated that the cost of the failure to the Deposit Insurance Fund was approximately $2.4 billion. And on March 23, the agency said it sold all the deposits and loans of Silicon Valley Bank –but not the bank’s portfolio of bonds and other securities—to First Citizens Bank & Trust of Raleigh, North Carolina. The FDIC estimated the deal cost the Deposit Insurance Fund about $16.1 billion. Why did depositors in Silicon Valley Bank and Signature Bank with more than $250,000 in their accounts get covered?

What about depositors at other banks with more than $250,000?

At times of acute financial stress, the law allows the government to lift the $250,000 ceiling. This is known as a “systemic risk exception.” If federal officials believe that normal procedures would have “serious adverse effects on economic conditions or financial stability,” a systemic risk exception can be declared by the Treasury Secretary, in consultation with the president, provided at least two-thirds of the members of the FDIC’s Board of Directors and two-thirds of the members of the Federal Reserve’s Board of Governors approve. The systemic risk exception was written into law in 1991 but wasn’t used until the Global Financial Crisis of 2008. In March 2023, Treasury Secretary Janet Yellen invoked the systemic risk exception to cover all deposits of Silicon Valley Bank and Signature Bank.

In May 2023, the FDIC proposed to cover its losses on SVB and Signature with an assessment of 0.125% a year for two years levied on large banks’ uninsured deposits, arguing that these banks benefited indirectly from the decision to cover all uninsured deposits at the two failed banks. It would exempt the first $5 billion of uninsured deposits at any bank from the assessment. Only 113 of the more than 4,000 banks insured by the FDIC would be subject to the levy, including the nation’s largest banks. The FDIC estimated the special assessment would raise $15.8 billion.

What changes to deposit insurance are under consideration?

In October 2025, Senators Bill Hagerty (R-Tenn.) and Angela Alsobrooks (D-Md.) introduced legislation that would raise the deposit insurance ceiling to $10 million for non-interest bearing transaction accounts at midsize banks. Deposits in these accounts, which are commonly used by small businesses for payroll and other operational expenses, often exceed the FDIC’s $250,000 limit. Consequently, panics at midsize banks—such as the failure of Silicon Valley Bank and Signature Bank in 2023—can lead to runs and potential financial crises.

Supporters of this bipartisan bill, including Treasury Secretary Scott Bessent and Senator Elizabeth Warren (D-Mass.), argue that raising the insurance limit for small business accounts would reduce the risk of future runs at midsize banks. Many supporters also share the belief that the current insurance limit handicaps community and regional banks while benefiting large banks like JP Morgan and Bank of America, who are implicitly insured for free due to their “too big to fail” status. “All small businesses that bank with smaller banks deserve the security larger businesses that bank at big banks receive,” Sen. Alsobrooks argued.

Critics of the proposal suggest that raising the insurance cap will increase moral hazard—that is, lead to riskier lending behavior due to the increased protection against bank runs—while failing to improve the management of poorly-run banks. If the FDIC insures accounts up to $10 million, and if the higher insurance cap leads to riskier lending and greater financial losses, the FDIC will have to foot a much larger bill, critics point out. At the same time, while midsize banks benefit most directly from this reform, larger banks will ultimately bear the cost. Over the next ten years, the additional cost of insuring these accounts would be borne exclusively by banks with assets exceeding $10 billion.

Some of the participants in an April 2023 Hutchins Center debate on the merits of raising the ceiling on deposit insurance favored a higher ceiling on the bank accounts that small businesses use for payroll and other purposes. You can read highlights of that debate here.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

How does deposit insurance work?

November 19, 2025