The recent upgrade of Greece’s long-term foreign credit rating by Moody’s from B3 to B1 is expected to encourage investor uptake of a 10-year, 2.5-billion-euro Greek government bond launching this week. At odds with this cautiously encouraging development was the European Commission’s (EC) enhanced surveillance report issued on February 27. Layered over this are persistent political economy challenges that continue to stymie financial sector and other structural reforms.

Today, neither the current government (which has become the best partner of the country’s creditors) nor the likely pending power grab by Kyriakos Mitsotakis of the main opposition center-right party, represent a threat to Greece’s stability. It is true that, with almost 30 billion euros worth of government-backed savings that function as a guarantee to potential investors, along with debt maturity extensions from creditors, investors might view a 10-year bond buy with a yield of around 3.9 percent as a great investment opportunity.

“The ongoing reform effort is slowly starting to bear fruit in the economy,” Moody’s said in a press release describing its gated report released last week. “While progress has been halting at times, with targets delayed or missed, the reform momentum appears to be increasingly entrenched, with good prospects for further progress and low risk of reversal.” The country’s current B1 ranking still remains four levels below investment grade, Bloomberg cautioned.

According to the EC’s enhanced surveillance report, although Greece has successfully eased its budget imbalances, and a list of outstanding reform commitments made last year were met by the end of 2018, “… the Greek government will need to complete the outstanding ones in order to receive the next disbursement…” of 970 million euros with an EC decision on releasing the funds postponed until Eurogroup finance ministers meet on March 11.

Greece must still undertake 16 uncompleted reforms in critical sectors such as energy and labor markets, but the most problematic issues are in the financial sector. The follow-through by the country’s four systemic banks—Alpha Bank, National Bank of Greece, Eurobank, and Praeus Bank—on their commitment to adopt tools for resolving nonperforming loans lags far behind. One pivotally important reform relates to overhauling law 3869/2010, which relates to restructuring the debt of over-indebted individuals. Called Katseli’s law, it protects the mortgages of primary residences, which, if revised along the lines demanded by creditors, would likely lead to the release of a 970 million euro tranche later this month.

In a nutshell, not only does the EC report come down hard on the government’s incomplete reforms, it also seems to be largely at odds with Moody’s rationale for a credit upgrade, which was based largely on progress to date of ongoing reforms!

Is the glass half full or half empty?

Political risk has eased following the unprecedented U-turn of the Prime Minister Alexis Tsipras’ government regarding his stand on the bailout programs. Since May 2017, after the much-delayed completion of the second evaluation of the Greek program, the current government appeared to align on almost every issue with the creditors. On the economic front in particular, it is true, in nominal terms, that budget imbalances have eased and the current account now has a small and manageable deficit. Meanwhile, growth for 2018 is officially expected to be above 2 percent—still not enough to lift all Greek boats. Over the next four years, the EC forecasts growth slightly above 2 percent, while the International Monetary Fund predicts average growth rates closer to 1 to 1.5 percent.

Based on current forecasts, Greece may not be equipped to grow at a rate high enough to allow the repayment of debts far into the future. The country’s economic woes didn’t just disappear with the end of its most recent rescue program last August. As extreme political and economic uncertainty recedes, the country and its productive base are starting to stabilize, but a strong rebound that will undo the losses incurred from the protracted crisis remains elusive. For now, the success of the three consecutive bailout programs is largely limited to the elimination of “twin” deficits—the one in the government budget and the other in the current account—not to mention the extensive wage cuts that made parts of the economy competitive again. Those wage cuts wreaked extensive collateral damage, leaving workers with limited spending power.

As even the EC reports acknowledge, investments as a percentage of GDP are currently less than 13 percent, the lowest of all eurozone countries. The investment deficit is now estimated at around 80 billion euros. A major investment boom is needed for both a higher GDP growth rate and greater productivity.

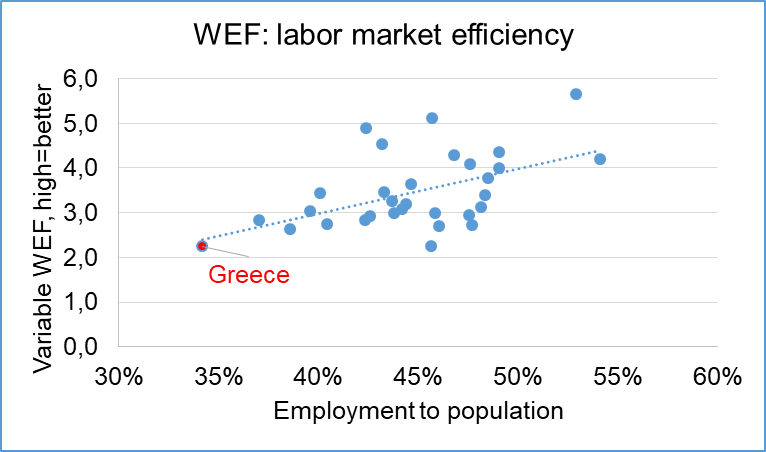

Compounding this is the country’s low labor market efficiency and a stubbornly high output gap, whereby potential (full employment) GDP and actual GDP are far apart. In this dynamic, potential GDP can decline when there is a brain drain or an aging population. GDP can also fall (or stall) when capital amortization is higher than new investments, which contributes to a big investment deficit. The country’s high tax on labor, imposed to reach the 3.5 percent primary budget surplus required as part of the bailout, only darkens the gloomy picture. In addition, that onerous tax is the main reason Greece has the lowest labor market efficiency in Europe (Figure 1).

Figure 1. Effect of taxation on employment (WEF GCI 2017-2018) and employment (15-64, Eurostat) to total employment (Eurostat) 2017

On another note, as exports have contributed the most to the country’s 2018 growth rate, another concern is that, as the global economy slows (see Figure 2, last column, 2019, first quarter), Greek exports may weaken, which would mean any GDP increase would have to come from domestic spending, foreign direct investment, or other areas.

Figure 2.

Last but not least, Greek politics are still not based on meritocracy but on favoritism and rent-seeking. To make matters worse, the economic crisis has left many people with low or medium skills jobless. Some of those unemployed citizens are now trying to enter politics to make a living irrespective of qualifications and ideology. The low quality of politics is really disappointing, and the weakness of the state apparatus makes matters even worse.

A new wave of clientelism (including within the current government) and a spirit of free-riding among certain segments of the population are not mentioned in either the Moody’s or EC reports. Yet both trends are seriously undermining Greece’s long-term prospects. This could portend a new wave of angry nationalistic populism amid the tough times that lie ahead.

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Greek economy: From bailout program exit to recovery?

March 6, 2019