Earlier this month, the Bill and Melinda Gates Foundation, in partnership with the French G-7 presidency, published the report, “Women’s Digital Financial Inclusion in Africa.” The report highlights progress in financial access, the benefits of financial inclusion, and strategies to bridge the access gap between men and women.

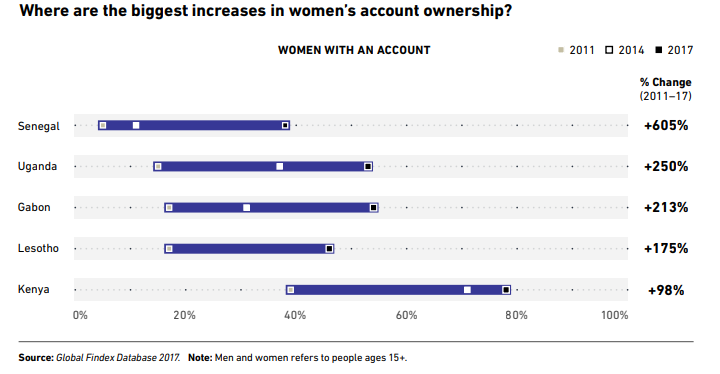

Overall, financial inclusion in Africa almost doubled from 23 percent to 43 percent between 2011 and 2017, led by growth in mobile money adoption. East Africa led in mobile money growth, followed by West and Central Africa. Women’s financial inclusion saw especially significant gains with the number of accounts rising by 600 percent in Senegal and doubling in more established markets like Kenya, bringing Kenyan women’s inclusion close to 80 percent (Figure 1). As cited in the report, recent research in Niger showed that women who received government subsidies through mobile money instead of cash had greater power in household decisionmaking. Similarly, research in Kenya has shown that women-headed households that adopted mobile money saw an increase in savings.

Figure 1: Where are the biggest increases in women’s account ownership?

Source: Women’s Digital Financial Inclusion in Africa

According to the report, despite this significant progress, two challenges persist—namely, limited interoperability across digital financial service providers and an inability to prove one’s identity. A lack of interoperability across service providers limits who customers can transact with, leading to underutilization of these services. Further, this obstacle also leads to additional problems such as high conversion fees and having to travel long distances to convert digital money to cash. The report highlights the need for more for open-loop payment systems, recommends that governments improve the policy framework around digital payments, and suggests that donors provide greater technical assistance funding to support this transition.

The second challenge, an inability to prove one’s identity, precludes individuals from accessing a range of government and private sector services, including finance. Currently, 30 percent of men and 45 percent of women in low-income countries around the world do not have a national ID. In Africa more specifically, the level of development of national ID systems varies widely. While Kenya and Rwanda have well-developed programs, systems are almost nonexistent in countries like Ethiopia and Liberia. The report recommends an increased focus on helping countries build digital ID systems to further inclusion. It recommends that countries take advantage of the World Bank’s ID4D initiative that provides technical assistance and suggests that the G-7 support the World Bank’s work in this area.

Related Content

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Figure of the week: Increasing financial inclusion for women in Africa

July 24, 2019