Over 20 years ago, Guillermo Calvo and Carmen Reinhart coined the term “fear of floating” to describe reluctance in emerging markets (EM) to embrace freely floating exchange rates. Their work came in the wake of the Asian financial crisis, when many exchange rate pegs collapsed in explosive fashion, with large devaluations and financial turmoil weighing on growth in the years that followed. Since then, many emerging markets have embraced fully flexible exchange rates, alongside adopting independent central banks and inflation targeting. However, significant holdouts remain, even as they continue to suffer periodic currency crises and volatility. (There are also many dirty floats, i.e., countries who intervene periodically, especially in Asia). Two things make currency pegs especially dangerous now: (i) Strong U.S. growth versus the rest of the world caused the dollar to rise sharply over the past decade, and there is no end in sight to this outperformance; and (ii) Elevated geopolitical risk is leading to big swings in commodity prices, causing the terms of trade of commodity importers and exporters to fluctuate sharply. A Trump win in the coming U.S. election—if it leads to more tariffs—could be the ultimate such terms-of-trade shock, putting severe depreciation pressure on remaining pegs.

Fear of floating in emerging markets

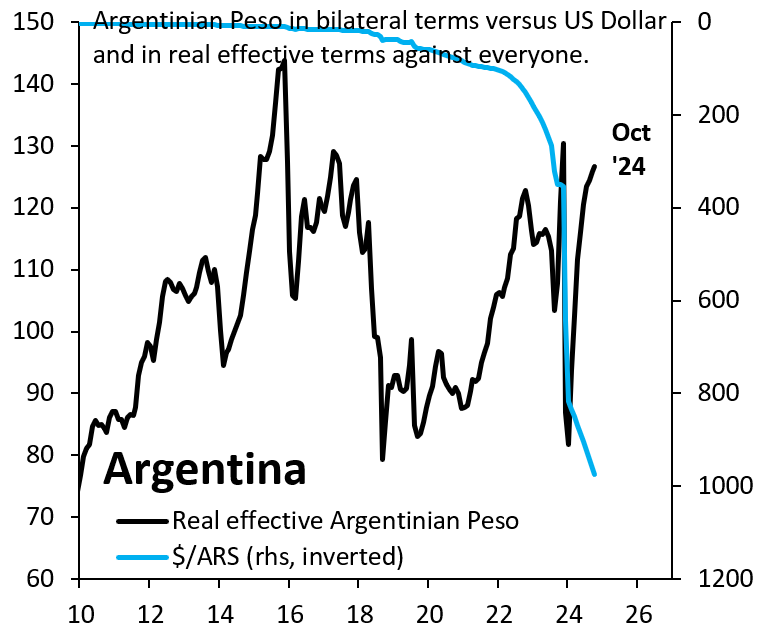

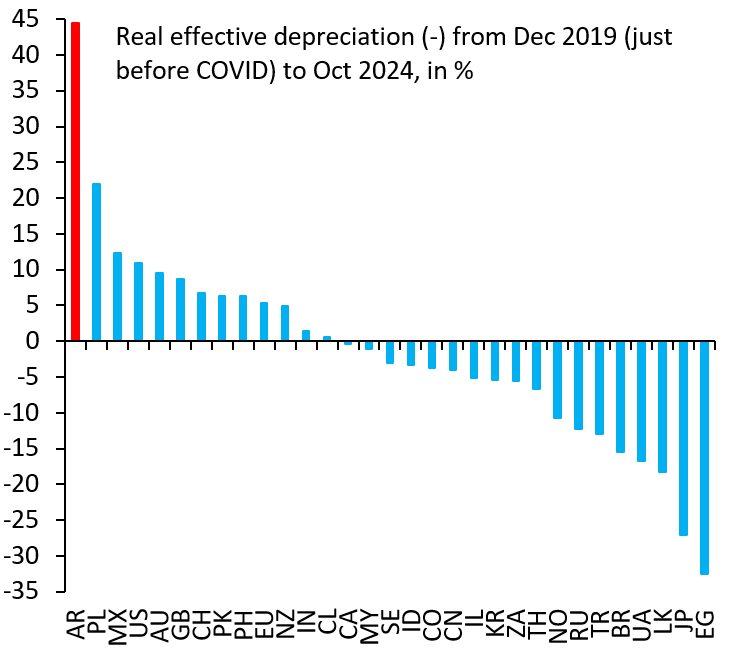

Many emerging markets have shifted to fully flexible exchange rates with independent central banks, but a few countries have not followed this trend. Argentina is perhaps the most prominent example and helps illustrate the dangers inherent in currency pegs. It most recently devalued the peso in December 2023, whereafter it adopted a crawling peg to the dollar. High inflation in the wake of the devaluation pushed the real exchange rate back up to where it was before the devaluation, so any competitiveness gain has now likely been lost (Figure 1). Indeed, on a cross-country comparison, Argentina’s peso has risen the most in real effective terms across all major currencies since the COVID-19 pandemic (Figure 2). The rebound in the real exchange rate could have been avoided had the government allowed the peso to float freely after the devaluation, since nominal depreciation would have offset high inflation. Without that safety valve, the peso has once again risen to unsustainable levels.

Figure 1. Argentine peso in bilateral terms vs. US dollar and in real effective terms against everyone

Source: Haver Analytics

Figure 2. Real effective depreciation, December 2019 to October 2024

Source: Haver Analytics

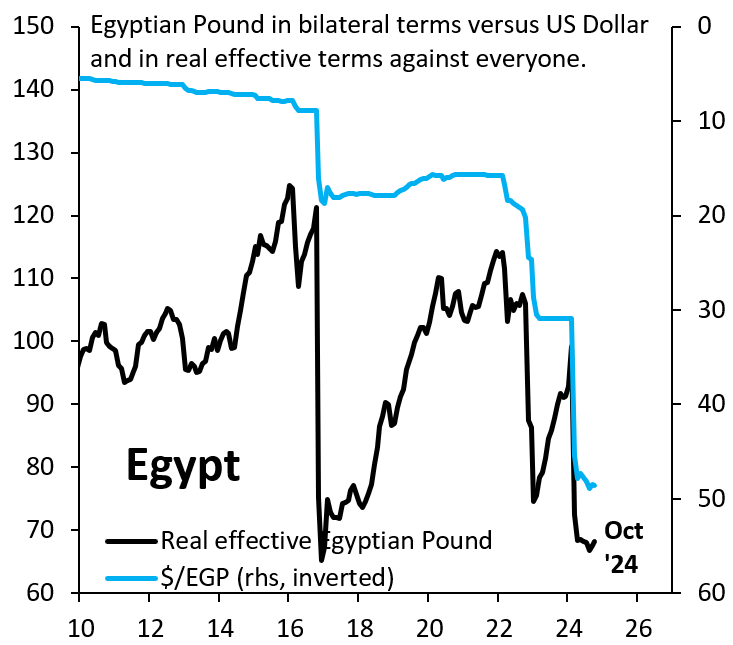

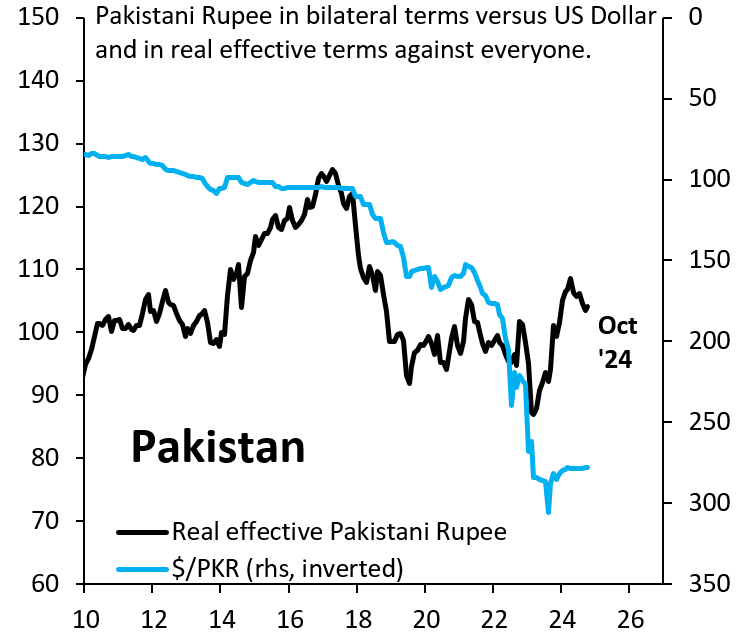

Other prominent examples in emerging markets are Egypt (Figure 3) and Pakistan (Figure 4). In both cases, reflexive repegging post-devaluation allows inflation to push up the exchange rate in real terms, locking these countries into a cycle of devaluation. Fear of floating provides the illusion of stability in the form of a nominal currency peg, but this only produces instability and harms growth over the medium term. Other prominent emerging markets locked into similar cycles include Sri Lanka, Turkey, and Ukraine.

Figure 3. Egyptian pound in bilateral terms vs. US dollar and in real effective terms against everyone

Source: Haver Analytics

Figure 4. Pakistani rupee in bilateral terms vs. US dollar and in real effective terms against everyone

Source: Haver Analytics

A uniquely bad time for dollar pegs

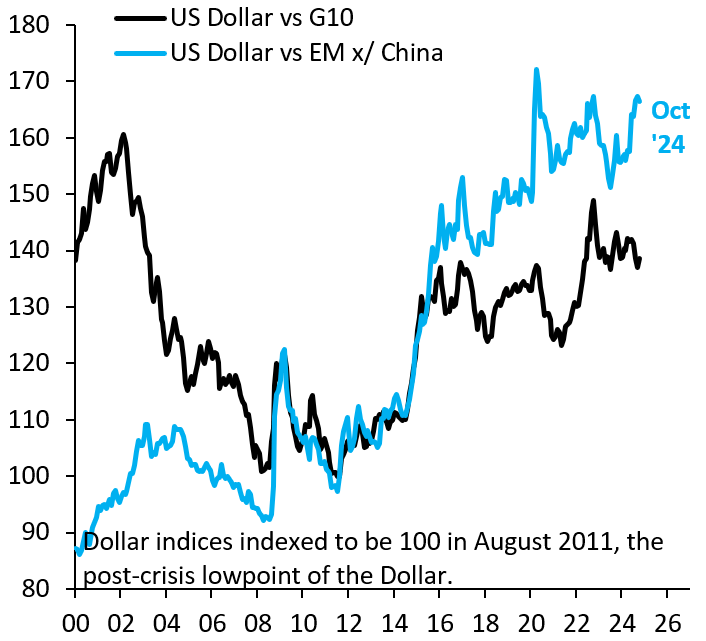

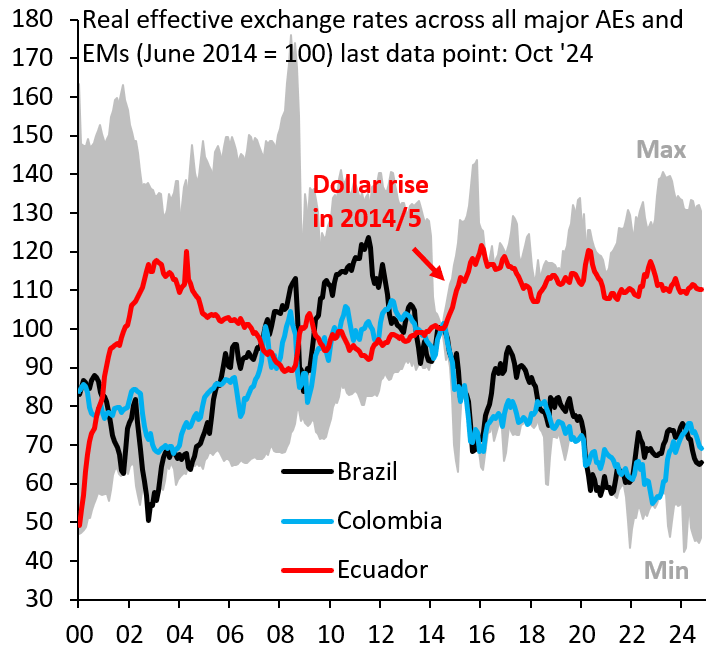

There are two things that make pegging to the dollar (the most prevalent peg) uniquely dangerous. First, the dollar has been on an uninterrupted rise over the past decade, as greater fiscal capacity and stronger growth in the United States than anywhere else have caused the greenback to appreciate (Figure 5). Any kind of dollar peg will inevitably shackle a country to this rise, damaging its competitiveness. Ecuador is the best example of this. It dollarized in 2000 and imported dollar strength in 2014-155, when falling commodity prices caused currencies in the rest of Latin America to weaken (Figure 6). Ecuador—a commodity exporter like many others in the region—suffered an adverse terms-of-trade shock, but—unlike others in the region—saw its real exchange rate rise. The result is weak growth and political instability.

Figure 5. US dollar vs. G10 and emerging markets excluding China

Source: Haver Analytics

Figure 6. Real effective exchange rates across all major advanced economies and emerging markets

Source: Haver Analytics

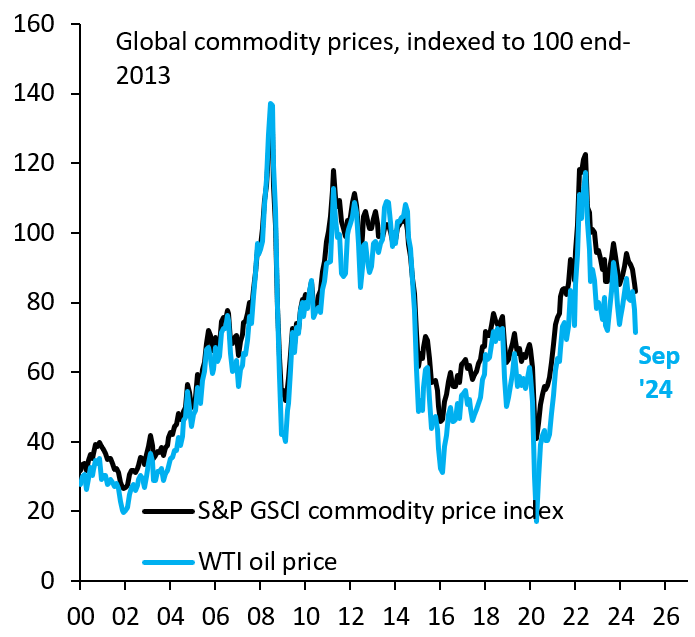

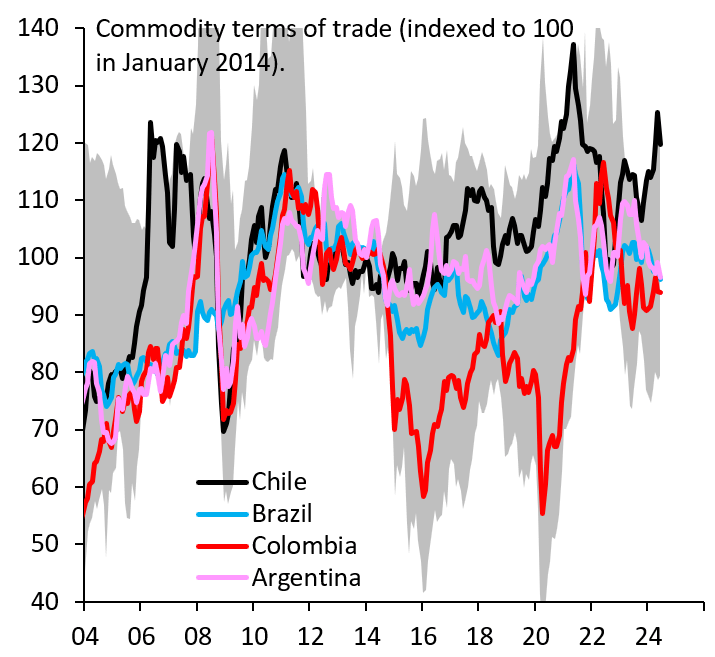

The second reason why exchange rate pegs are dangerous is elevated geopolitical risk. The war in Ukraine and instability in the Middle East mean commodity prices may now be more volatile (Figure 7), which is driving large swings in the terms of trade of commodity importers and exporters (Figure 8). This volatility in the terms of trade makes it even more important that exchange rates be allowed to move freely. A Trump win in the upcoming U.S. elections could be the ultimate manifestation of elevated geopolitical risk if more U.S. tariffs spark a broad rise in the dollar, putting depreciation pressure on remaining emerging market pegs. The current juncture is a uniquely dangerous time for dollar pegs.

Figure 7. Global commodity prices

Source: Haver Analytics

Figure 8. Commodity terms of trade

Source: Haver Analytics

Author

Related Content

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Fear of floating exchange rates in emerging markets

October 24, 2024