Executive Summary

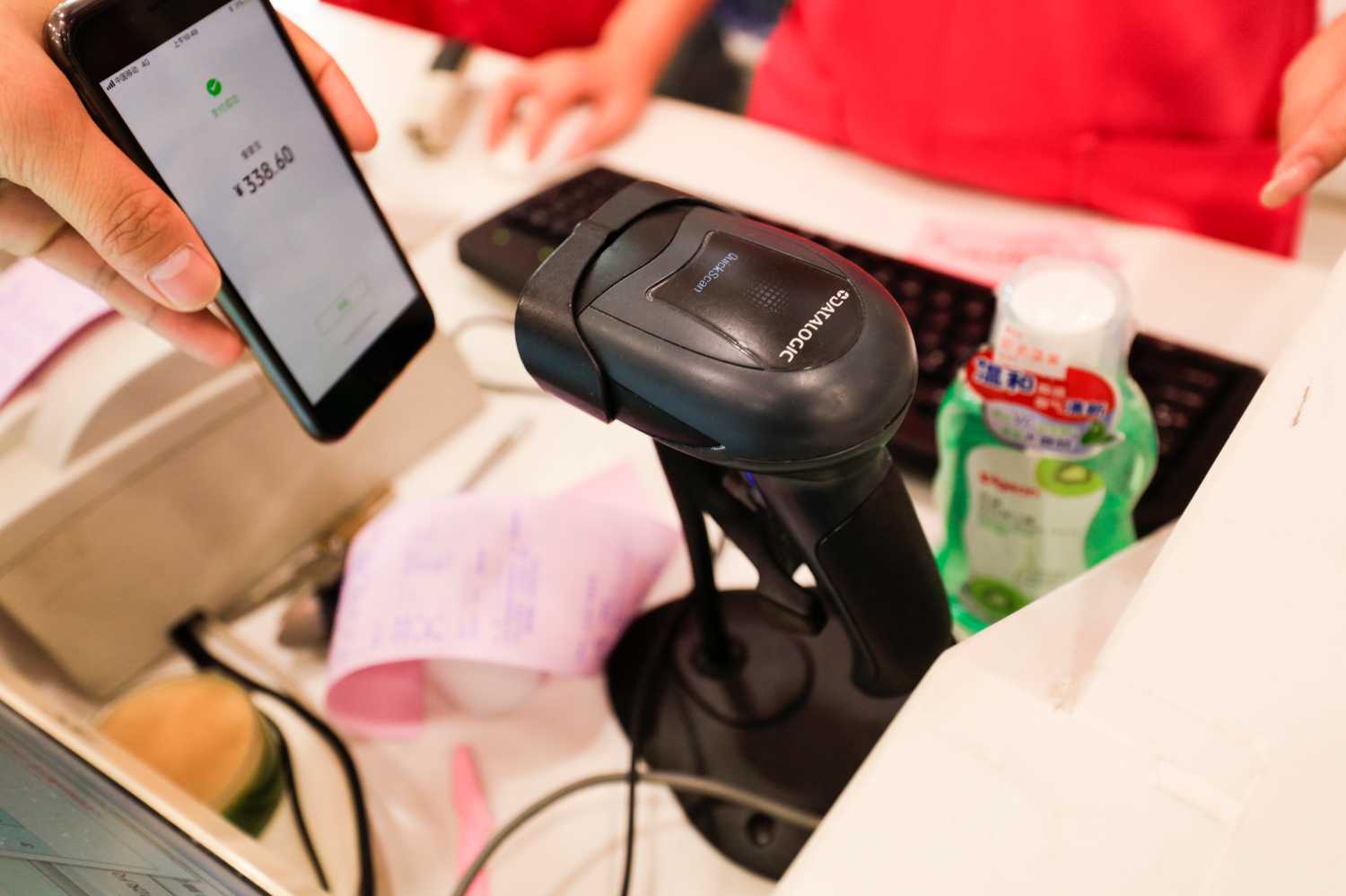

While America spent the past decade upgrading its bank-based magnetic striped cards with chips, China experienced a retail payment revolution. Leapfrogging the card-based system, two new payment systems have come to dominate person-to-person, retail, and many business transactions. China’s new system is built on digital wallets, QR codes (two-dimensional bar codes), and runs through their own big tech firms: Alipay running through Alibaba (China’s version of Amazon) and WeChat Pay running through Tencent (China’s version of Facebook). China’s system largely disintermediates banks from payment transactions, robbing banks of an important and long-standing source of revenue. It creates an alternative payment ecosystem with different incentives between merchants, consumers, and payment system providers. It challenges the long-standing placement of payments on the side of banking as opposed to commerce. In doing so, this system creates new incentives that could realign existing business models and relationships between merchants, banks, and technology providers. China’s new payment system exploded in under a decade, growing from inception to dominance. With over a billion users on each platform, the power of network incentives has been unleashed. The new payment system has replaced cards and cash at registers, how families give gifts, and even how beggars ask for money, with QR codes replacing tin cups.

While America spent the past decade upgrading its bank-based magnetic striped cards with chips, China experienced a retail payment revolution. Leapfrogging the card-based system, two new payment systems have come to dominate person-to-person, retail, and many business transactions. China’s new system is built on digital wallets, QR codes (two-dimensional bar codes), and runs through their own big tech firms: Alipay running through Alibaba (China’s version of Amazon) and WeChat Pay running through Tencent (China’s version of Facebook). China’s system largely disintermediates banks from payment transactions, robbing banks of an important and long-standing source of revenue. It creates an alternative payment ecosystem with different incentives between merchants, consumers, and payment system providers. It challenges the long-standing placement of payments on the side of banking as opposed to commerce. In doing so, this system creates new incentives that could realign existing business models and relationships between merchants, banks, and technology providers. China’s new payment system exploded in under a decade, growing from inception to dominance. With over a billion users on each platform, the power of network incentives has been unleashed. The new payment system has replaced cards and cash at registers, how families give gifts, and even how beggars ask for money, with QR codes replacing tin cups.

What does this mean for the future of China’s payment system and America’s response? First, China’s new payment system is here to stay. It will continue to grow domestically and globally, following Chinese travelers and consumers abroad. Second, new technology makes possible the movement of the payment system away from banking and into technology and social networking. This means that technology and social network firms with sources of data on which to base financial decisions such as providing credit will be able to provide alternative underwriting that is likely to follow. Third, the incentives created by moving the payment system from banking to technology firms are substantial and potentially concerning. The potential for anti-competitive behavior and privacy concerns by tech platforms by using the payment system and data generated from it are real. However, it is not clear whether these concerns can and would be remedied by effective regulation. Finally, the same economics that make China’s system beneficial for merchants but bad for Chinese banks are why the Chinese system is unlikely to catch on in America, but may be more viable in other countries with less-developed banking systems.

While America led the global revolution in payments half a century ago with magnetic striped credit and debit cards, China is leading the new revolution in digital payments. In the past decade, China has leapfrogged magnetic cards, moving to a system based on smartphones and QR codes. But the changes from this system go far beyond just a new technological form. The Chinese payment system has done something far more revolutionary: It has largely disintermediated the banking system.

In America, and most developed economies globally, the payment and banking systems have been intertwined for centuries. The connection between the two is clear: Who is better equipped to intermediate payments between parties than the financial institutions that hold those parties’ funds? Yet new financial technology and its application in China have created a viable alternative payments model where banks play a far less central role, and in the extreme, possibly none.

This new payment form requires greater analysis to appreciate the benefits, costs, and implications from a new model. Understanding this model will help answer key questions and inform policy decisions. Will the American-led invention of magnetic stripes and card readers be globally replaced by digital wallets using QR codes to transfer funds external to the banking system? Will banks continue to play the central role in operating payment systems or will new tech disintermediate banks? If disintermediation occurs, what are the ramifications of combining payments with commerce instead of banking?

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).