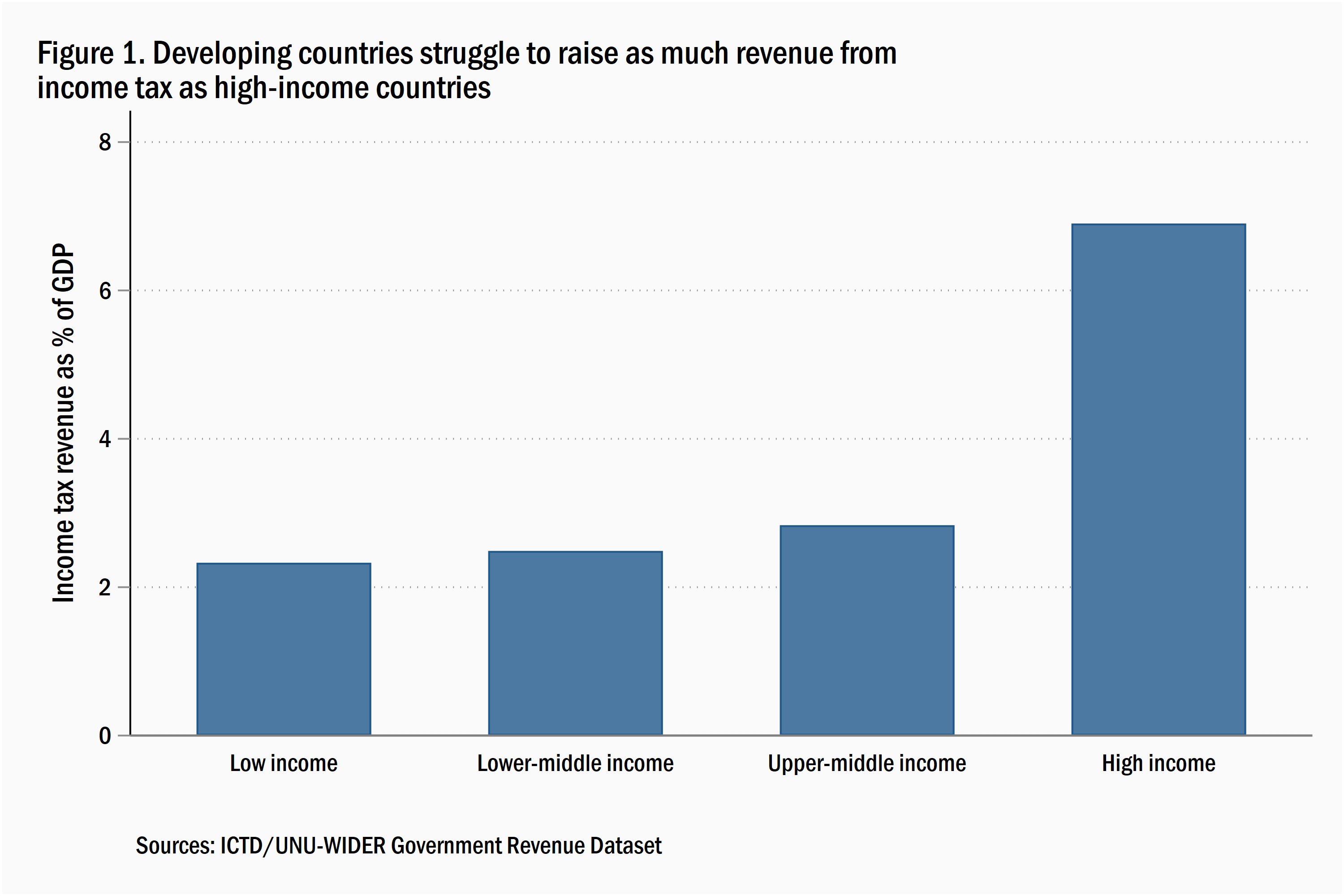

If you want to stop the government or fellow citizens from knowing the true extent of your wealth, you can do no better than move that money offshore. This time-honored strategy works well for those wishing to avoid taxation but remains a constant frustration to authorities trying to build progressive tax systems and stymie inequality and corruption: It’s difficult to eat the rich if you can’t figure out where they dine. Taxing people’s income directly remains particularly elusive for developing countries, which raise around one-third as much from income taxes relative to their GDP as high-income countries (Figure 1). Reining in offshore tax evasion would be a step in the right direction.

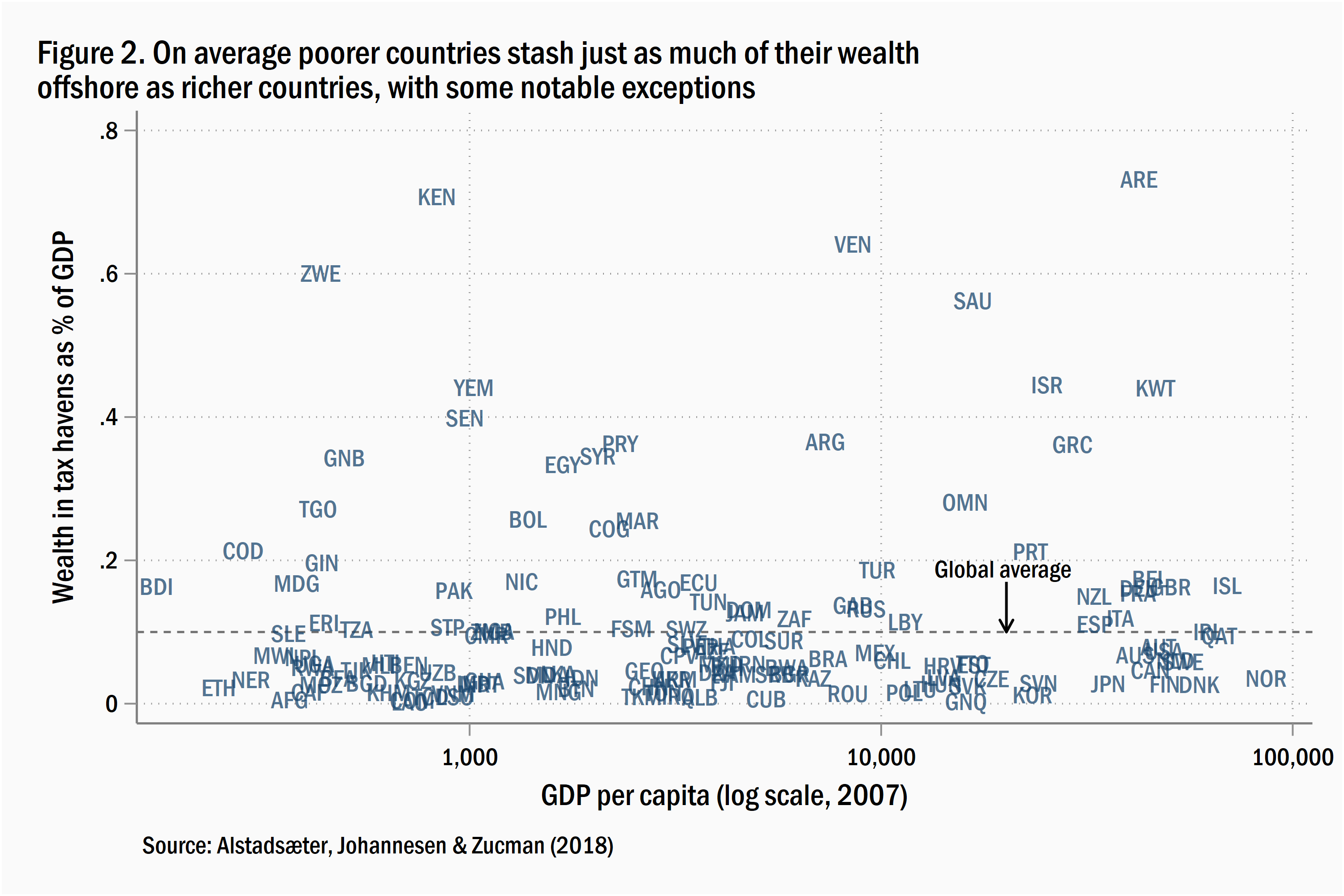

What little evidence we have suggests that offshore evasion is at least as pronounced in poorer countries as it is in richer ones. Annette Alstadsæter, Niels Johannsen, and Gabriel Zucman used a combination of international deposit and portfolio data to estimate that the equivalent of 10 percent of global GDP is held in tax havens. Their country-level estimates, which are only as recent as 2007, reveal that as a percentage of GDP, poor countries stash just about as much of their wealth offshore as rich ones do, and that there are outliers at all levels of GDP per capita (Figure 2).

Micro-level work also suggests that offshore ownership is dominated by elites, and that secrecy is their best defense against the prying eye of tax authorities. Work by UCLA’s Juliana Londoño-Vélez with Javier Avila-Mahecha found that rich Colombians were much more likely to hide wealth offshore, with over 40 percent of the top 0.01 percent engaging in the practice. But that same work found that bridging the information gap made a difference: Colombian elites that were named in the Panama Papers leak were substantially more likely to declare their wealth through a disclosure scheme run by the tax authority.

Most developing countries lack the tools to go after offshore money

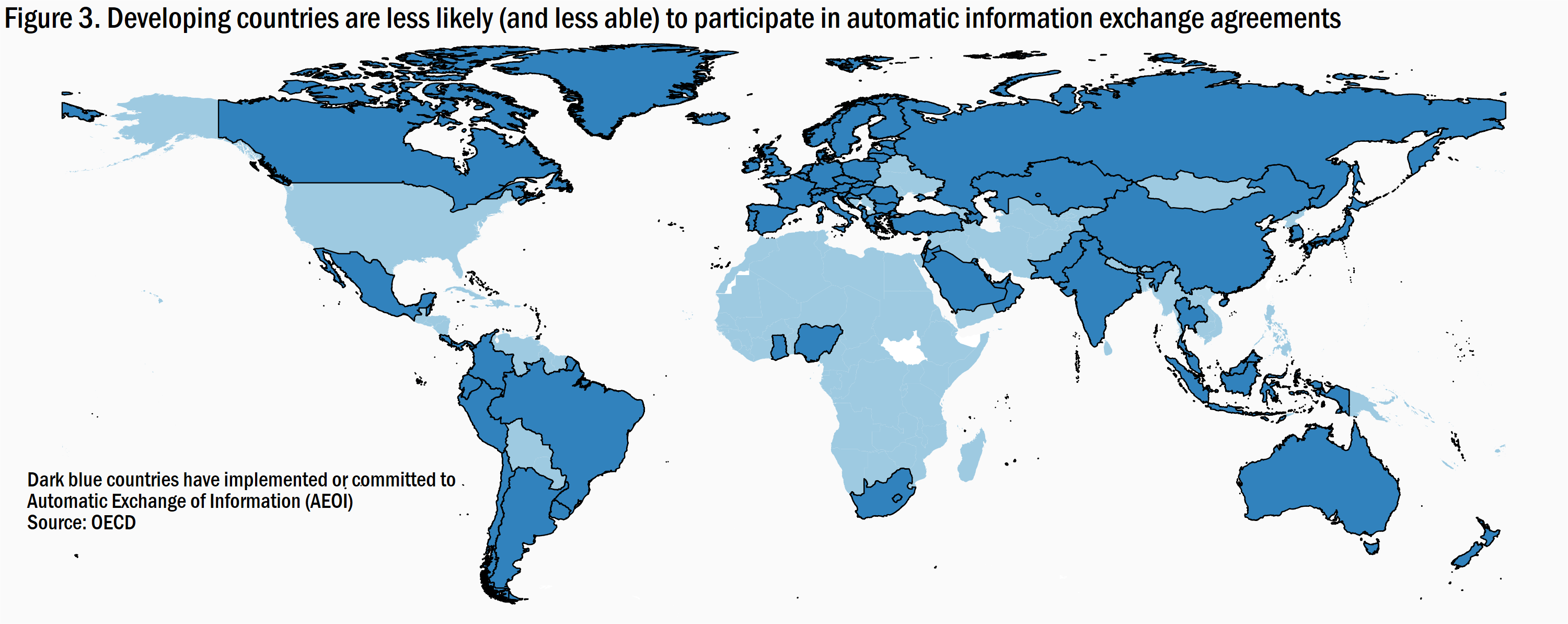

Leaks of financial data like the Panama Papers offer a useful snapshot for tax authorities, but how can they have more systematic, timely data on the offshore world? The solution put forward by the OECD suggests that tax authorities routinely gather and exchange relevant data on bank deposit ownership with each other. As of this year, 115 countries, including most tax havens, have signed up to the OECD’s framework for the Automatic Exchange of Information (AEOI). The few studies that have been conducted show that when these exchange agreements are implemented, offshore wealth shrinks—and does so rapidly.

But if you look at a map of who has signed up to AEOI, it’s hard not to spot the obvious: Poorer countries haven’t been able to take advantage of this information exchange. Only 7 percent of low-income and lower-middle income countries have adopted AEOI or committed to implementing it by 2023 (Figure 3).

This gulf in participation is driven by the fact that many developing countries currently lack the capacity to gather comprehensive data on what little wealth foreigners are stashing in their banks. To compound matters further, AEOI is based on a principle of reciprocity: To join the club, you have to be ready to share information with all of its members. Because of this, many developing countries remain shut out of a trove of information that would be useful for tracking down hidden wealth or corrupt assets.

Official statistics may understate how much offshore wealth elites from developing countries control

We know from estimates produced by Alstadsæter et al. that developing countries hold about the same amount of wealth offshore as a proportion of their GDP. Those estimates are in part based on data produced by the Bank of International Settlements (BIS), which gathers and publishes data from mostly high-income countries on foreigner’s claims on bank deposits.

But there is some evidence that the international statistics may understate the true level of offshore wealth held by some countries. When the BIS assigns the ownership of offshore accounts, it relies on each bank’s own assessment of the residence of the owner—whether it is a person or a company. There are two limitations to this approach. First, banks have little incentive to get this information right, so they will be more inclined to take an account owner’s claim of residence at face value. Second, and more importantly, if a person’s wealth comes from their ownership of a company, the residence is assigned based only on where that person is located. This means that the accuracy of the BIS doesn’t extend to shell corporations.

Data from AEOI reports should in theory make it easier to correctly identify the jurisdiction where the owners of offshore wealth reside. For certain types of corporations, banks are required to gather and share information on the ultimate owner or beneficiary of that account. This means that even if a corporation in a tax haven that will passively hold wealth is set up, once the tax haven and the home country sign up to AEOI, information on the account beneficiary will be disclosed. AEOI data isn’t perfect: Most customers had warning before banks began gathering and sharing this information and may have moved their assets elsewhere before the light flooded in. But AEOI is still likely a big improvement on past frameworks.

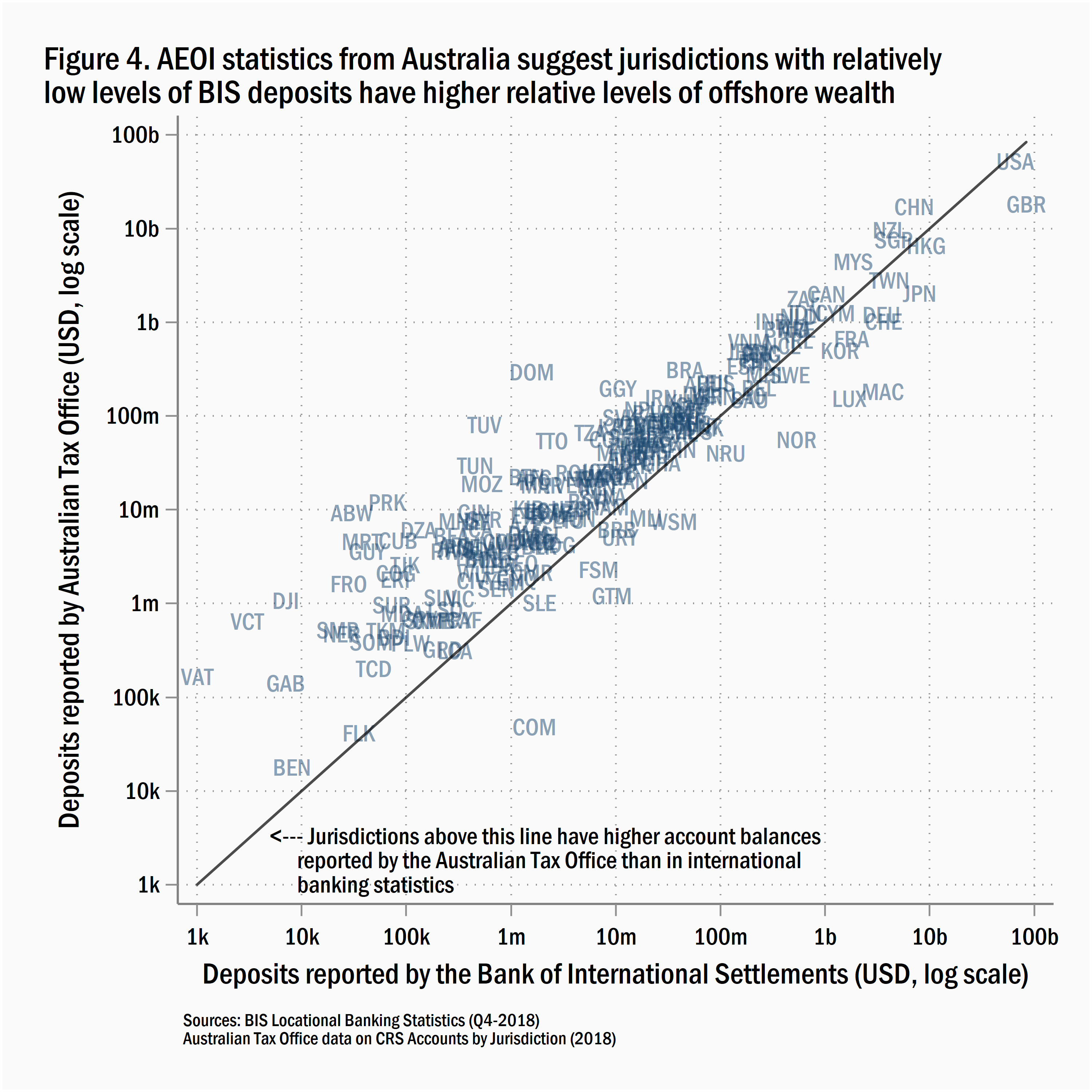

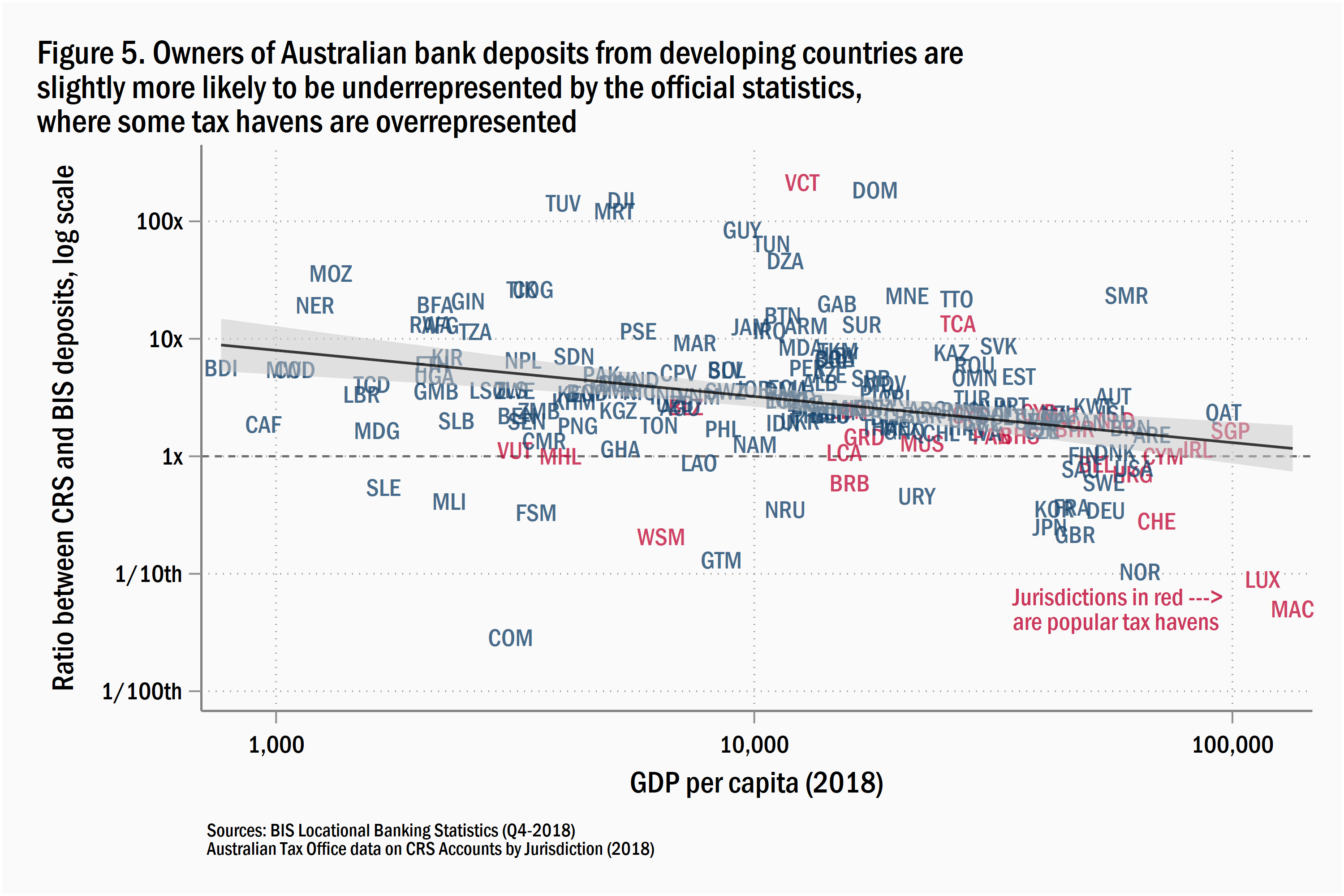

Most countries keep data from their AEOI exchanges a secret, but the Australian Tax Office recently—after some nudging from civil society groups—released information on offshore ownership in 2018. These published figures will deviate from the BIS statistics for many legitimate reasons: Australia assigns the entire account balance to the jurisdiction of each owner of an account, so there is some double counting. BIS data also includes loans and doesn’t cover the same range of financial institutions as the OECD’s framework for AEOI statistics. Even so, the data released by the Australian Tax Office offers a rare opportunity to observe where and why the BIS may understate true levels of offshore wealth (Figure 4).

When one compares the two data sources, smaller economies with lower levels of deposits in Australia tend to have better coverage in AEOI statistics than they do in BIS data. As we move down in GDP per capita, the ratio of AEOI-to-BIS deposits increases from around 1-1 to 10-1, suggesting that official statistics may be obscuring the true levels of wealth held by developing countries, even in a non-tax haven country like Australia (Figure 5). By contrast, many jurisdictions commonly thought of as tax havens have lower levels of deposits in the AEOI statistics relative to those in the BIS statistics, reflecting the fact that many companies in tax havens are shell companies used to obscure the ultimate owner of assets.

Tax authorities in developing countries have much to gain from going after offshore wealth but are constrained in their ability to participate in the automatic exchange of information as constructed. Entities like the OECD, the World Bank, and Tax Inspectors without Borders have started to provide some technical assistance to developing countries to get them up to speed.

But these efforts will take time to move the needle. If we want to get data on offshore wealth into the hands of countries that need it the most, the OECD should consider relaxing the reciprocity restriction for automatic exchange of information for countries that meet predetermined criteria, either those below a certain GDP per capita or based on a recent metric of tax capacity. Until then, tax officials in developing countries can chase the rich as far as their national borders, but no further.

Related Content

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Can developing countries rein in offshore wealth?

October 9, 2020