This piece has been updated with clarifications on data and sourcing, and a correction to Figure 1 and Figure 4.

According to the latest data from the Federal Reserve’s Survey of Consumer Finances, the nation’s racial wealth gap increased during the COVID-19 pandemic. Between 2019 and 2022, median wealth increased by $51,800, but the racial wealth gap increased by $49,950—adding up to a total difference of $240,120 in wealth between the median white household and the median Black household.

The Survey of Consumer Finances is the most comprehensive survey on household wealth in the United States. Updated every three years, this data provides a representative outlook of our current and past economic landscapes, which is particularly helpful in capturing the economic realities of households during the onset, peak, and duration of the COVID-19 pandemic.

Even though wealth increased across the board, the data discussed here shows that not all people are reaping the benefits. While housing equity increased for Black households, other components to wealth-building such as corporate and business equity did not, exacerbating the racial wealth gap. Centuries of discrimination in public policy, financial practices, and societal norms that limited Black wealth accumulation have not been overcome, and will require broad structural changes to rectify the long-lasting impact of inequality.

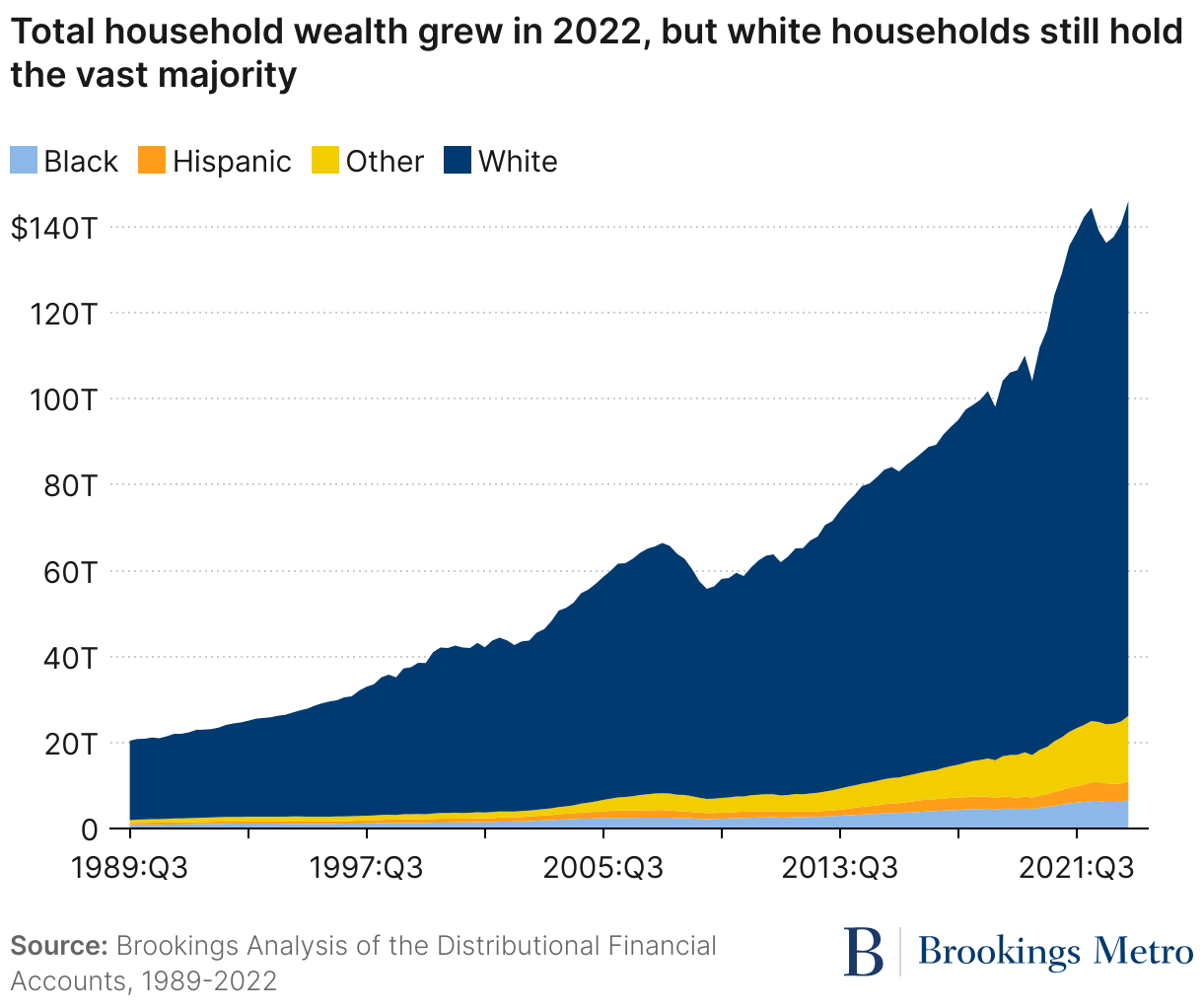

Wealth increases during the pandemic did not narrow the persistent racial wealth gap

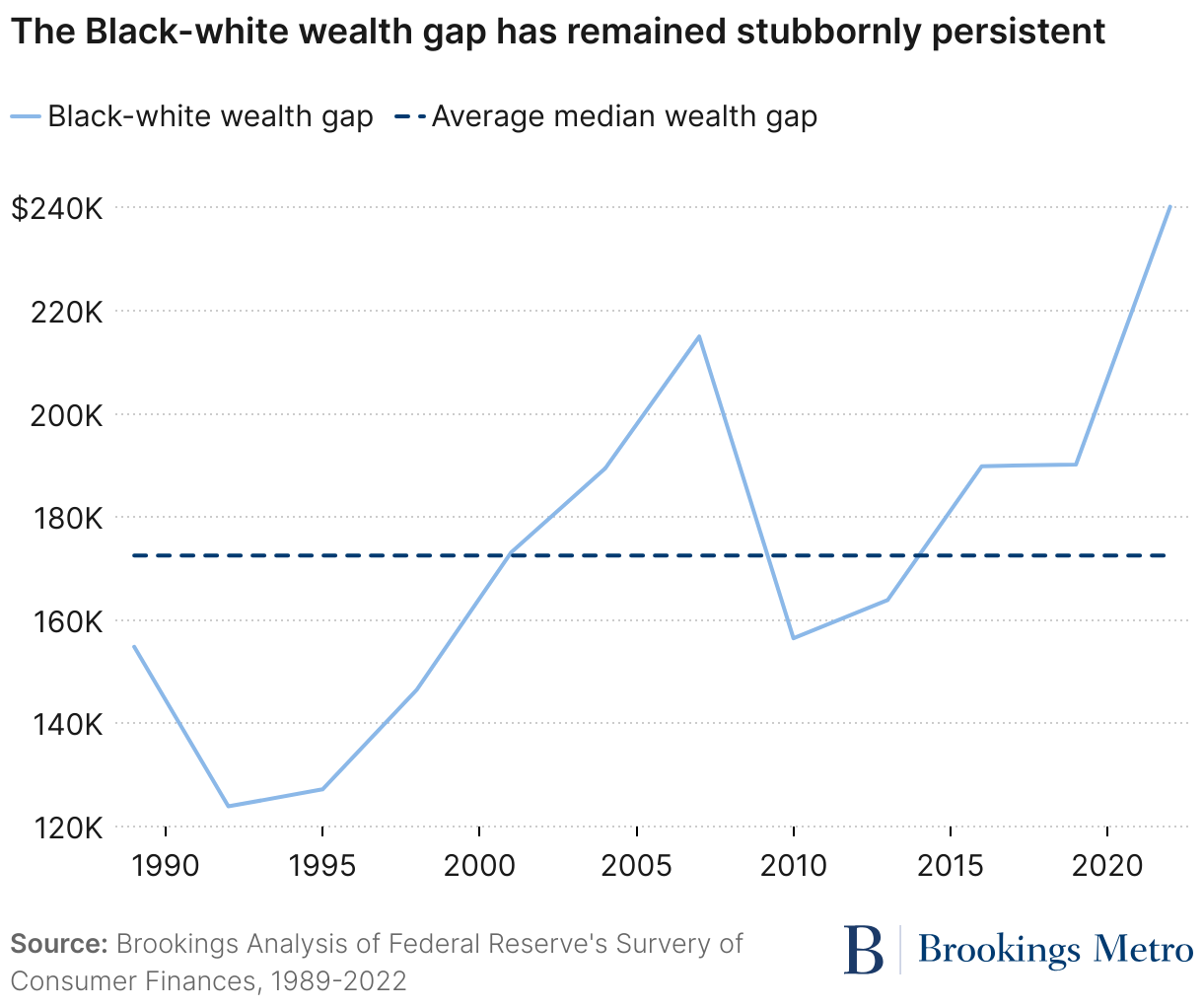

...in 2022, for every $100 in wealth held by white households, Black households held only $15.

Wealth measures the total value of assets a family owns (such as housing and business equity) minus their debts (such as student loans and credit card bills). During the COVID-19 pandemic, wealth increased unevenly. Median wealth, which provides an indication of a typical household’s financial security and capacity to invest in their future, increased at varied rates depending on race.

Figure 1, using data from the Federal Reserve’s Distributional Financial Accounts, shows that between 2019 and 2022, total wealth increased for all racial and ethnic groups. However, according to the Survey for Consumer Finances, median Black wealth increased from $27,970 to $44,890, but continued to lag other racial groups. In 2022, median wealth was approximately $62,000 for non-white Latino or Hispanic households; $285,000 for white households; and $536,000 for Asian American households. (Asian American household wealth data was only provided for 2022, and therefore time series graphs will only show wealth data for the racial categories Black, Latino or Hispanic, white, and other, which includes Asian American, Native American, and Pacific Islander wealth.)

Since 2010, the wealth disparity between Black and white families has persistently expanded. From the very first Survey of Consumer Finances in 1983, the smallest difference between Black and white family wealth was $123,910 in 1992, and has steadily climbed since, peaking in 2022.

Figure 2 shows that from 1989 to 2022, the Black-white median wealth gap has averaged $172,000, and rarely dropped below 10% of this. However, between 2019 and 2022, the gap breeched 10% of the average—signaling an increase in disparity not seen since 2007, when the gap reached $214,970. The growing disparity means that in 2022, for every $100 in wealth held by white households, Black households held only $15.

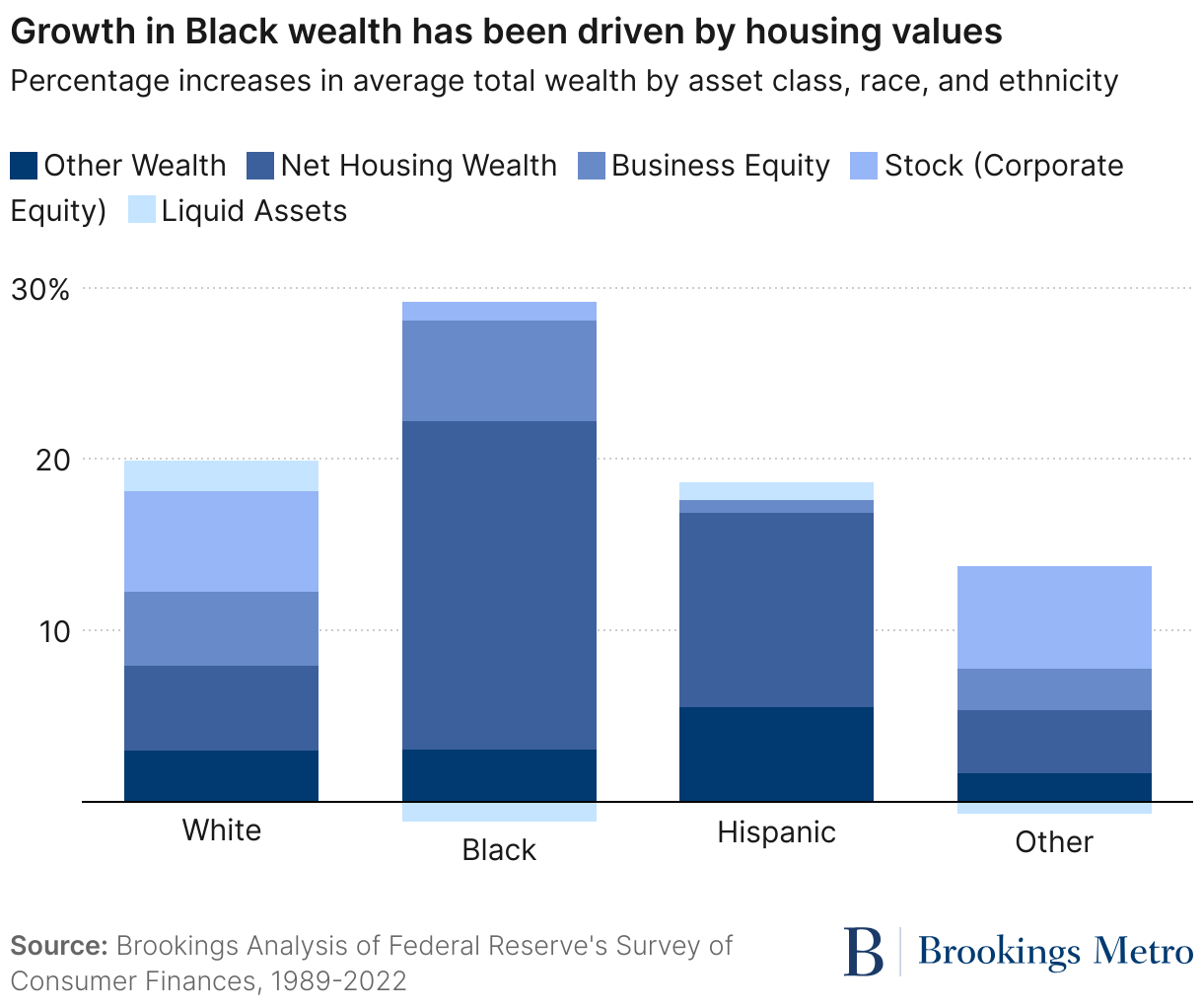

Net housing equity drove increases in Black wealth, while corporate and business equity drove increases in white wealth

Net housing equity, followed by business equity, drove the largest portion of wealth accumulation for Black Americans from 2019 to 2022, as shown in Figure 3. However, racial disparities in homeownership continue to throttle this growth, with only 44% of Black individuals owning a home, compared to nearly 73% of white individuals—a vestige of discriminatory housing practices such as redlining and blockbusting.

Business equity is another vital wealth-building component for Black families, representing 21% of wealth accumulation for Black households. The proportion of business equity in overall growth was much lower for Latino or Hispanic households (4%) but similar for white households (22%) and other non-Latino or Hispanic racial groups (21%). An increase in Black businesses can play a critical role in increasing wealth, and not just for business owners. In 2020, Black businesses employed 1.3 million people and created over 48,000 new jobs.

The largest disparity in wealth growth was in stock equity, which made up nearly 30% of white wealth but only 4% of Black wealth. This is indicative of the impact of intergenerational wealth divides resulting in the average white family possessing more investment capital than the average Black family. Since 1980, the profits made from selling off stocks—known as capital gains—has acted as a key driver of stock equity disparities, significantly concentrating wealth into white households. Stock equity appreciates more rapidly in comparison to housing equity, catalyzing wealth accumulation drastically for those who historically already hold stocks. Large racial disparities in stock equity reflect the growing concentration of wealth; in 2020, Brookings Senior Fellow Vanessa Williamson wrote that the 400 richest Americans have more total wealth than all 10 million Black American households combined.

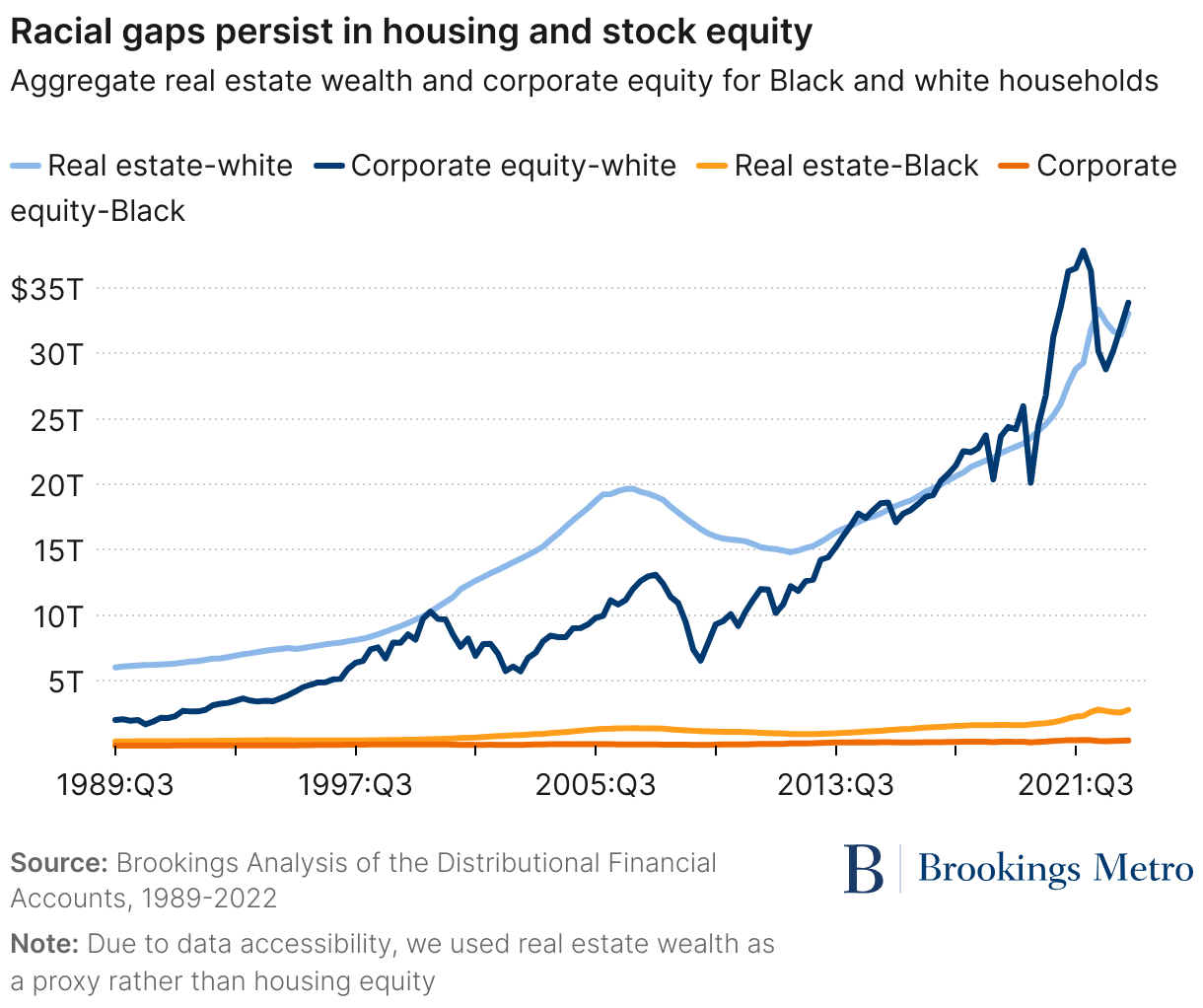

Looking at housing and stock wealth since 1989 (Figure 4), the increasing wealth gap becomes dramatically clear. Real estate wealth and stock equity show the power of intergenerational accumulation that a myriad of discriminatory policies has catalyzed, concentrating ownership in white communities. In the 1980s, a booming market made prior ownership of stocks and housing even more powerful, exacerbating the Black-white wealth gap.

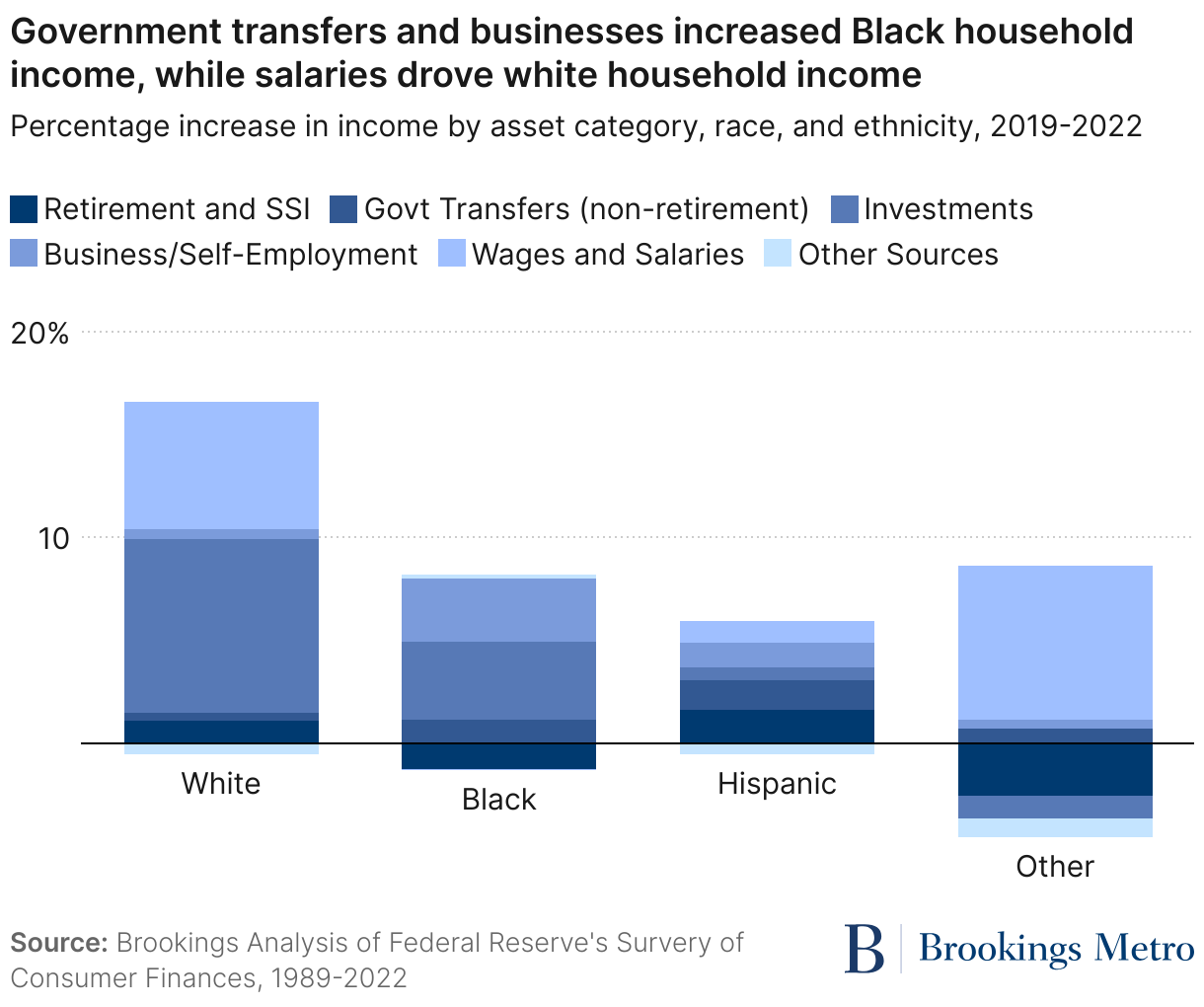

More granularly, Figure 5 shows that between 2019 and 2022, decreases in salaries among Black families drove income declines, yet business revenue (including from self-employment) and government transfers drove income increases. During the COVID-19 pandemic and corresponding economic downturn, unemployment spiked most severely for Black Americans, reaching 11.4%. Since then, unemployment has reached record lows, hovering at 3.5% —indicating that pandemic-related income loss was an important driver of the net decline in Black household wealth. Additionally, liquid assets drove a decline in wealth for Black Americans from 2019 to 2022, while for white households, they drove an increase of about 2%.

During the COVID-19 pandemic, government transfers played a larger role in average income growth for Black and Latino or Hispanic households compared to white households, who profited most from investments and wages. Government transfers comprised 17% of overall income growth for Black households, rising 1.1% from 2019 to 2022, and 26% for Latino or Hispanic households, as historic economic relief legislation such as the Coronavirus Aid, Relief, and Economic Security (CARES) Act sent direct cash payments to millions of Americans. However, income growth for white Americans—whose incomes grew the most of any racial group during this period—looked significantly different, with 53% of overall growth coming for investment returns and 38% coming from wages and salaries, rising 6.2% from 2019 to 2022. The various sources of income during the pandemic highlight the severe disparities between economic safety nets and avenues for wealth accumulation across racial groups.

We need structural solutions to close the racial wealth gap

These findings illustrate the systemic compounding of wealth, which exacerbates racial gaps. In other words, wealth begets wealth. Past and present discrimination in critical markets—including housing, banking, taxation, higher education, and more—result in lower average wealth for Black families. Policies that privilege whiteness are reflected in higher levels of wealth for the average white family, which can be leveraged across generations to generate greater wealth and advantages. This became very clear during the pandemic: Black households made major gains through housing and business equity, yet that growth paled in comparison to white households’ gains from investment returns.

While growth in Black ownership of businesses and homes is a positive step forward, it is not enough to combat the compounding effect of wealth. In lieu of significant policy changes that impact wealth accumulation and distribution, racial inequality will likely continue to grow. Efforts to close this racial wealth gap include progressive tax policies in which the average tax burden increases with wealth and income, or reparations from the private and public sector. In tandem, both will act to ease immediate disparities and put us on a path of reconvergence so that racial wealth equity might be seen in our lifetime.

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).