This June, the Biden-Harris administration acknowledged the historic role that biased home valuations have played in limiting Black Americans’ wealth-building opportunities, releasing a fact sheet detailing how the administration plans to address this systemic racial bias. The plan reflects a call for action to confront a broader set of issues within the housing market and taxation system that intersect to uniquely affect Black communities. Black homeowners face inequities in our tax code and housing industry, unfair tax burdens, and a biased appraisal system—all of which undermining the potential of homeownership as a wealth-building tool for Black homebuyers. But structural reforms are possible, and they could help to build systems that grow—rather than extract—Black wealth.

In this piece, we explore the often overlooked and compounding racially discriminatory practices in the housing market and property taxation system, and how they limit wealth-building opportunities for Black homeowners. We also explore how the current housing market allows white homebuyers’ preferences to dictate the racial makeup of residential communities and the extent to which Black homebuyers can gain equity from their home. These issues underscore that the Biden-Harris administration must remain committed to addressing the layered practices of discrimination and promote policies that empower Black homeowners to build generational wealth.

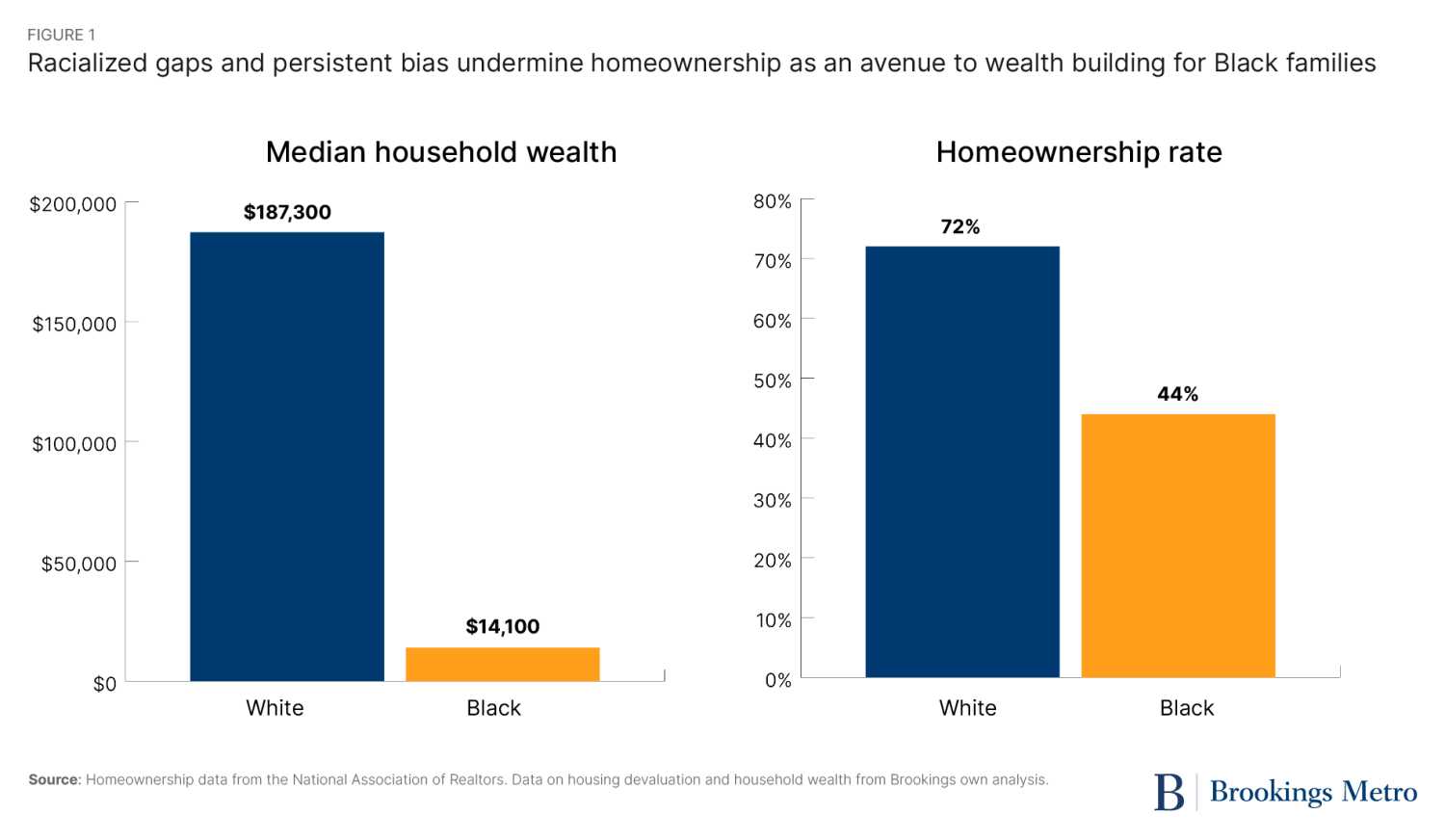

Housing and tax policy penalize Black homeowners and widen the racial wealth gap

Twentieth-century discriminatory housing policies and practices are indisputably responsible for segregating America’s residential communities and contributing to existing racial wealth disparities. Tax law and practice aggravate these effects and place a disproportionately heavy financial and oftentimes emotional burden on the average Black homeowner. So, while public conversations about how to close the racial wealth gap often focus on the importance of homeownership, they overlook the impact of the property tax system—particularly, property valuation mechanisms—on the Black homeownership experience.

Property assessments and appraisals are two different estimations of a home’s value, conducted at two different times. Their contribution to the improper valuation of Black-owned homes—through both over-assessment and under-valuation—have caused Black homeowners to lose money by way of monthly property tax payments and at the time of sale. This burden is a reflection of America’s disinvestment in, devaluation of, and disrespect for predominantly Black neighborhoods. It also reveals a penalty that housing institutions and legal frameworks place on Black homeowners—a penalty that will only grow more harmful if we continue to try to address it with ahistorical, race-neutral solutions.

Today, median white household wealth sits at $187,300, compared to just $14,100 for Black households. And while 72.7% of white Americans are homeowners, only 44% of Black Americans are. These extreme racial disparities in wealth and homeownership signify a chasm in access to homeownership and the opportunities and privileges it affords. As outlined in a 2017 report, home equity is the largest segment in most U.S. families’ wealth portfolio. However, Black and Latino or Hispanic families are less likely to own their homes and accrue less wealth through homeownership than white families. According to the Census Bureau’s 2019 Survey of Income and Program Participation, the median wealth for renters was $4,084, compared to $125,500 for homeowners (excluding home equity).

Although homeownership is thought to exemplify the American dream, our tax laws are designed such that homeowners in Black-majority communities don’t always see that dream realized as home equity. Empowering Black people and their communities requires housing and tax reforms that affirm their historically unrecognized value.

The US tax system protects accumulated wealth, creating a barrier to homeownership for lower-income, low-wealth households

For decades, researchers have shown that qualifying for homeownership is a sizeable financial challenge due to the large upfront costs. Many prospective buyers need financial assistance or must save for years to make a down payment, whereas others can rely on intergenerational wealth transfers to fund their purchase of a home.

White college-educated households are more likely to receive a financial gift of over $10,000 from family members than Black college-educated households: 32% versus 9%, respectively. Moreover, the average gift to white households is significantly larger than the average gift to Black households: $235,353 versus $65,755, respectively. In white families, wealth transfers are more likely to flow from parent to child or grandparent to grandchild; yet in Black families, wealth transfers are more likely to flow in the opposite direction.

Now, consider that the U.S. tax code provides additional relief to prospective buyers whose families have excess capital to gift them. The code enables a grantor to gift up to $17,000 without having to report the transfer on the IRS gift tax return form, and the grantee does not have to pay taxes on it or report it (unless it comes from a foreign source).

Such financial gifts are powerful in that they provide white families with a head start to wealth-building through homeownership. They also allow wealth to accumulate across generations in ways that it does not for Black families due to family structure and lack of access to excess capital.

Property tax assessments and valuations are biased against Black homeowners

The local property tax applied to the over-assessed value of Black-owned homes is 10% to 13% higher than for white-owned homes.

The average Black homeowner faces a disproportionally higher property tax burden than the average white homeowner. In the U.S., property taxes are supposed to be based on the value of the home; however, researchers at Indiana University concluded that nationwide, tax assessors often over-assess Black-owned homes relative to their market value. Consequently, the local property tax applied to the over-assessed value of Black-owned homes is 10% to 13% higher than for white-owned homes.

Conversely, property assessments for white-owned homes are often closer to the home’s market value. Ultimately, Black homeowners end up paying a higher property tax bill than they should because the value of their home has been over-estimated compared to what it will sell for. White homeowners, on the other hand, pay a more accurate property tax bill because their home value estimations are often closer to the actual sales price.

Similarly, Brookings research has shown that real estate appraisers often undervalue Black-owned homes by 21% to 23%, which lowers the price a home is likely to be sold for. The over-assessment of Black-owned homes is the fault of tax assessors (81.3% of whom are white), whereas the undervaluation of Black-owned homes is the fault of licensed professional appraisers (99% of whom are white). These discrepancies demonstrate deep flaws in the two mechanisms the housing industry uses to determine “value” and present a real barrier to wealth-building for Black homeowners.

Brookings research has shown that real estate appraisers often undervalue Black-owned homes by 21% to 23%, which lowers the price a home is likely to be sold for.

Data suggests that Black homeowners’ ability to gain wealth through homeownership is also largely dependent upon the housing preferences of white Americans. Whereas Black people prefer to live in neighborhoods where the majority of the population is made up of racial and ethnic minorities, white people prefer to live in communities with very low Black populations. Further, homes in white neighborhoods are appraised at three times the value of homes in communities of color, and, over the last decade, homes in white neighborhoods appreciated $200,000 more on average than similar homes in communities of color. Data also shows that homes lose approximately 16% of their value once the neighborhood’s population of Black residents reaches 10%.

Therefore, Black people have the highest likelihood of building wealth through homeownership when they purchase in predominantly white neighborhoods, where homes are more likely to appreciate, but where they are also severely outnumbered by white residents. The experience of Black homeowners in choosing where to live is heavily influenced by white preferences, which limits potential opportunities for Black Americans to build wealth.

Identifying equitable solutions for Black wealth-building through homeownership

The many racial biases within the housing market are often addressed as individual challenges rather than compounding factors that work together to undermine Black wealth. Despite numerous legislative efforts to combat racial discrimination in housing, racially biased practices are still prevalent and utilized by private actors, lenders, property tax assessors, and property appraisers.

The disproportionately heavy tax burden alongside racialized home appreciation and wealth transfer disparities reveal that our federal, state, and local tax policies and housing industry penalize Black neighborhoods and their residents. At its core, this penalty is rooted in systemic racism and negative perceptions of Blackness enforced by our legal system. In fact, the American Institute of Real Estate Appraisers, in their historic official texts, advocated for appraisal practices that viewed an influx of racial and ethnic diversity as lessening the desirability of a neighborhood and contributing to the lowering of home values.

Access to wealth-building homeownership should exist in every neighborhood, and a Black homeowner’s ability to build wealth should not be based on the subjective perceptions of white professionals or the preferences of white homebuyers. Furthermore, using homeownership to close the racial wealth gap—which was estimated to sit at $10.14 trillion—requires that the burden to eliminate wealth inequality in America no longer be placed on Black homeowners as individuals, but the factors that created it in the first place. After all, Black people created America’s wealth, not its wealth gap.

Homeownership data from the National Association of Realtors, available at: More Americans Own Their Homes, but Black-White Homeownership Rate Gap is Biggest in a Decade, NAR Report Finds.

Today, Black Americans are trying to play “catch up” to others that have been afforded the necessary conditions to build wealth for generations. While many Black homeowners have achieved upward social mobility, the tax code and housing industry do not empower them like it does for white homeowners. Attempting to close the racial wealth gap by encouraging Black Americans to pursue homeownership—assuming that it will benefit them in the same way it has white Americans—is a hollow hope because of the inequities within the broader housing market. Moreover, it places an undue burden on prospective Black homebuyers to do alone what white people have done with significant government assistance that explicitly excluded Black Americans. Accordingly, reforms must be made to finally acknowledge and cement the value that has always existed in Black communities.

To combat the racial wealth gap, Dorothy Brown, Georgetown Law Professor and author of “The Whiteness of Wealth,” proposed a wealth-based refundable tax credit for taxpayers whose wealth falls below the median of approximately $100,000. Brown has acknowledged that although the tax credit is not targeted directly at Black taxpayers, a disproportionate share of taxpayers that fall below median wealth are Black (83%). Thus, an initiative of this sort is likely to withstand legal challenges because it is directed toward a socioeconomic class rather than a racial group.

The U.S. tax code is somewhat “progressive,” although Brookings research has shown that it has become less so over the last five decades. Irrespective of income level, the tax code is structured to reward existing wealth, predominantly held by white households. Creating a wealth tax credit might be a sizable legislative challenge, but one worth fighting for given its potential impact on Black communities and its ability to economically empower those with the lowest levels of wealth.

In addition to proposing a wealth-based refundable tax credit, Brown has also advocated for introducing a “living allowance” deduction. In this, taxpayers would receive a deduction or fixed amount of money that could be subtracted from their taxable income (reducing the amount of taxes owed) based on their cost of living. If they earned more money than the living allowance, they would pay taxes on the excess amount at a progressive rate; if they earned less, they would receive a check from the government. This is different from the current system in that it would tax all income and remove all deductions and exclusions in the tax code, which primarily benefit wealthy white taxpayers.

Lastly, greater transparency would also help address the root causes of the wealth gap. Brown has called for the public release of IRS tax data by race to more easily identify discriminatory tax policies. All of these proposed reforms seek to level the playing field for Black taxpayers and mitigate the advantage the tax code currently provides to wealthy white taxpayers.

These changes to the tax code should be supported by complementary policy. One suggestion is the baby bonds program proposed by economist Darrick Hamilton and William Darity, Jr. Through this program, the government would create and manage investment accounts for infants, providing them with grants based on their family’s wealth. The account would grow at a guaranteed annual rate, and upon reaching adulthood, the child could use the money for higher education, a startup, or a down payment on a home. This program has the potential to support low-wealth families in the same way financial gifts empower high-wealth families, again with a high likelihood of disproportionately benefiting Back families.

We need structural changes in taxation and housing to make wealth-building through homeownership a reality for more Black homebuyers

Ultimately, removing the influence of white subjectivity on the mechanisms that determine the value of Black communities, people, and assets is imperative to building Black wealth. It is unreasonable and unjust to expect Black Americans alone to close the racial wealth gap through homeownership, especially if solutions to closing the gap continue to rely on the subjective beliefs of white Americans and a housing industry that is still rife with racial bias.

The current systems we use to measure the value of Black homes invite racial biases that influence home value estimations and, ultimately, the market value of Black-owned property. Changing property tax assessment procedures by regulating government-appointed assessors and standardizing assessment procedures so that they are based on the characteristics and quality of a home as opposed to its proximity to Black people would be an effective way to remove biases that lead to the over-assessment of Black homes and the subsequent higher taxation of Black homeowners.

We must confront the inequities in our tax code and housing industry, remove the disparate tax burden from Black homeowners, and make wealth-building through homeownership a reality for more prospective Black homebuyers. The racial wealth gap is not an accident—it is a policy failure rooted in white supremacy and enshrined in biased policy mechanisms that punish low-income and Black communities. Until we acknowledge this truth, the dream of opportunity, economic success, and well-being for many Black Americans will remain deferred.

Authors

-

Acknowledgements and disclosures

The authors would like to thank our reviewer, Dorothy Brown, author of “The Whiteness of Wealth,” for her generous contributions to this article.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).