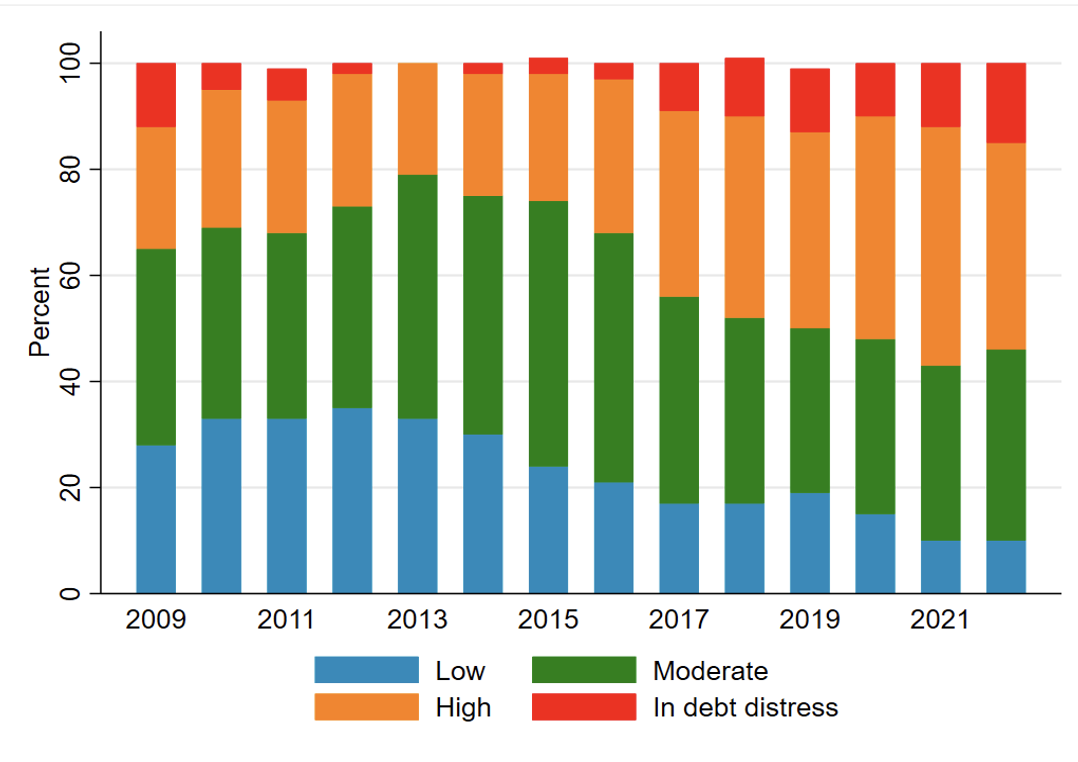

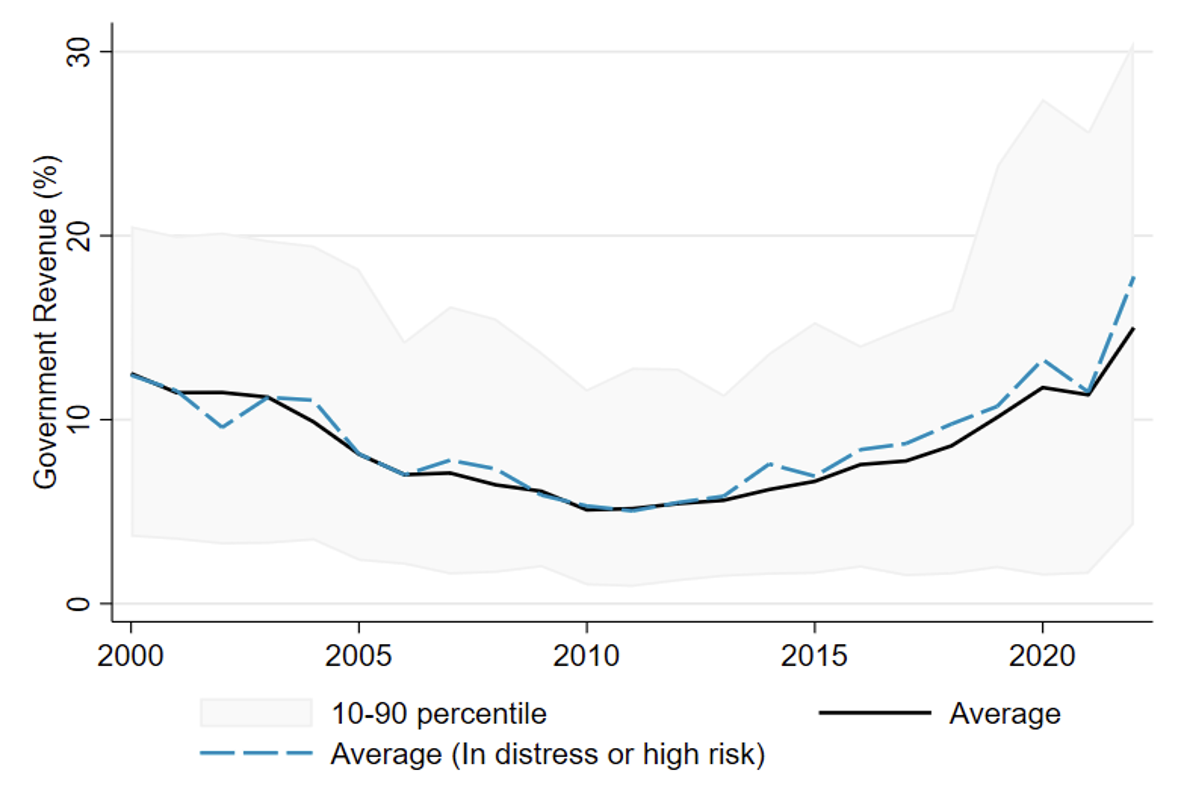

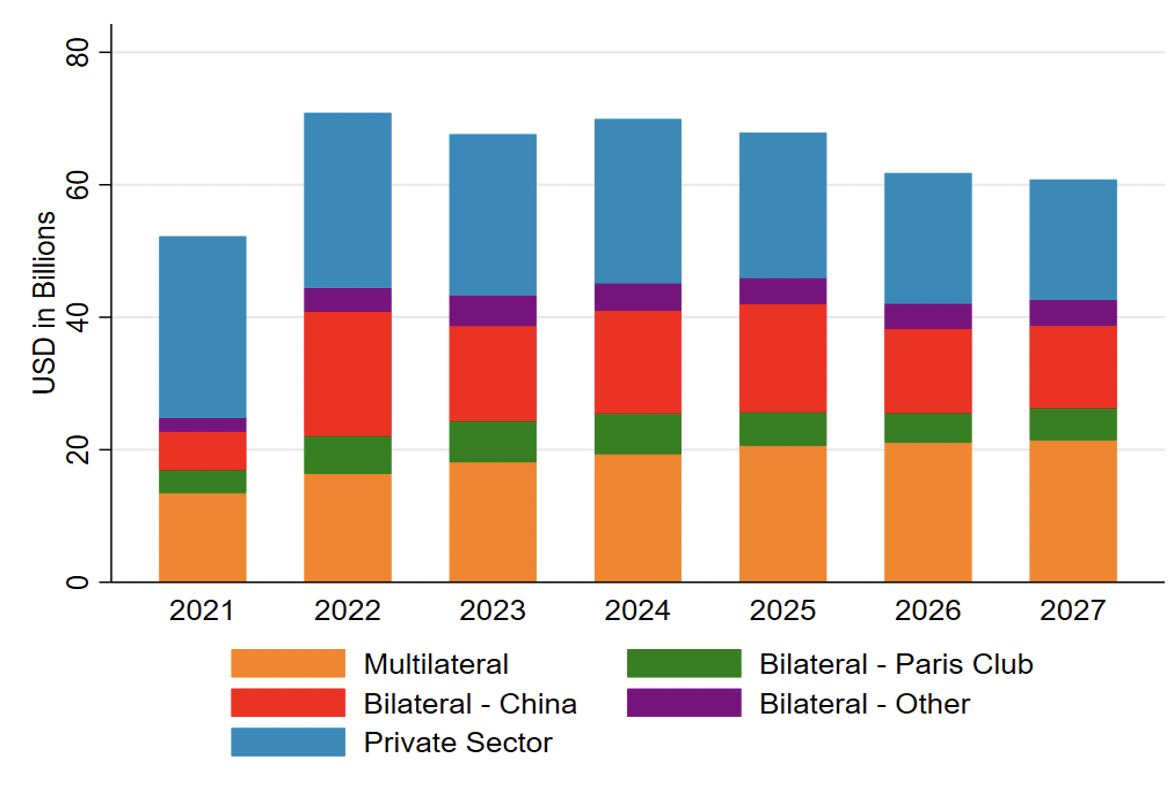

Among the challenges facing developing countries, none is arguably more crucial than the significantly deteriorated fiscal situation that threatens to erase several years of progress on development agendas. According to some estimates, almost 60 percent of the poorest countries are either in or at high risk of debt distress, nearly doubling since 2015 (Figure 1; World Bank 2022a). Total debt service payments on public and publicly guaranteed (PPG) external debt of the poorest countries rose to over $50 billions in 2021, with repayments now representing 11.3 percent of government revenue in the poorest countries, up from 5.1 percent in 2010 (Figure 2). In most developing countries, the cost of servicing external debt now exceeds expenditures on health, education, and social protection combined (UNICEF, 2021). The current global environment characterized by higher global interest rates and exchange rate depreciations against major currencies is adding to the fiscal challenge by raising the cost of external financing and debt service. Debt service payments for the poorest countries rose 36 percent to over $70 billion last year and are projected to remain elevated through at least 2027 (Figure 3). It is increasingly evident that the Common Framework for Debt Treatments, adopted by the G-20 to help developing countries restructure their debts and address solvency issues and protracted liquidity problems, is facing serious operational challenges. Echoing widely shared concerns about the limitations of the CF, the International Monetary Fund’s Managing Director called for changes to it while the World Bank President urged for the acceleration of its implementation. Likely due to the challenges with the CF, out of the 37 countries at high risk of or in debt distress, only four countries have requested assistance under the framework so far. We need a pre-emptive and wholesale approach to restore fiscal sustainability across the developing world and avert a systemic debt crisis.

Figure 1: Low-income countries Debt Sustainability Analysis

Source: IMF Annual Report (2022a) and author’s calculations using the IMF Debt Sustainability Analysis for Low-income Countries (2022).

Figure 2: External PPG debt servicing cost (2000-2022)

Source: Author’s calculations using World Bank International Debt Statistics (2021) and IMF World Economic Outlook database (2022b).

Figure 3: Total external PPG debt service coming due

Source: Author’s calculations using World Bank International Debt Statistics (2021).

In this policy brief, we propose that the G-20 adopt a Brady-like scheme to accelerate the restructuring of external private sector debt to restore debt sustainability in the affected countries with the following design features.

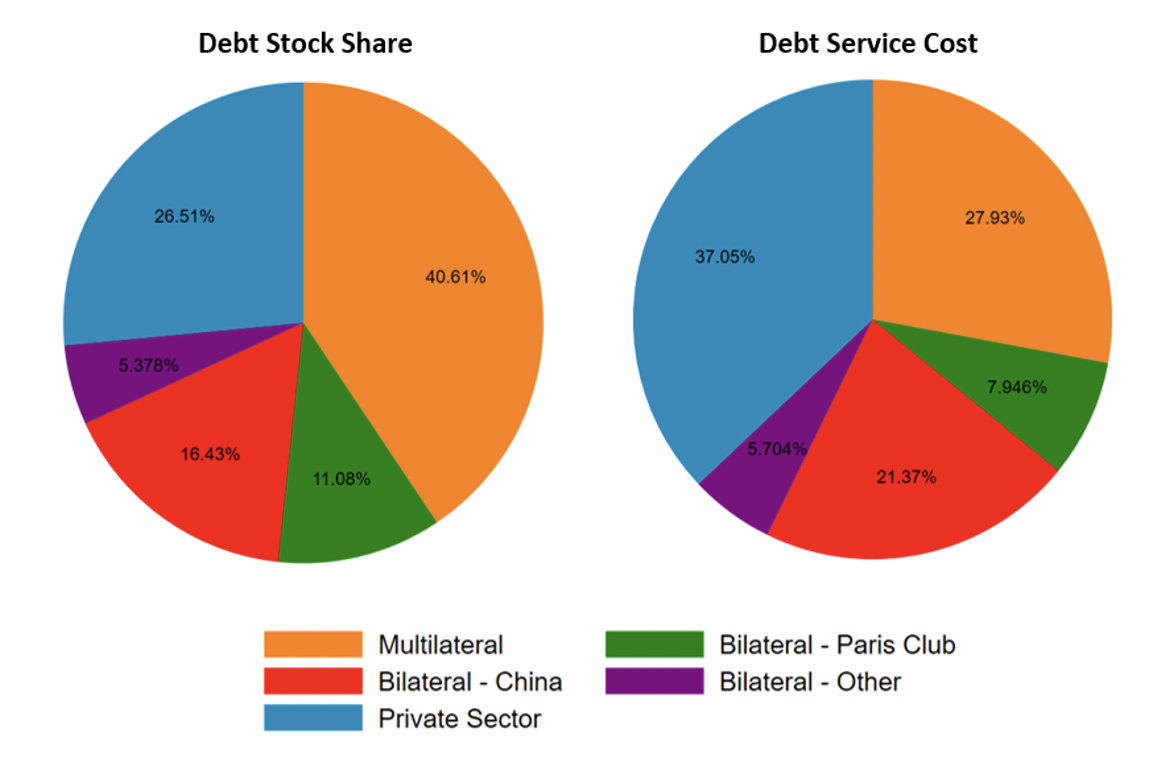

First, we recommend the creation of a new special purpose fund—the recovery and sustainability fund (RSF)—to be capitalized by International Financial Institutions (IFIs) and bilateral donors. Second, the funds will be used to secure collateral against new tradable bonds—Recovery and Sustainability bonds (RSBs)— issued by participating indebted countries. The guarantees attached to the RSBs will provide credit enhancement and allow countries to issue the new bonds on terms that are more favorable than those of the current stock of private external debt. As shown in Figure 4, despite holding about 27 percent of the debt, the private sector accounts for 37 percent of the debt service due to the higher cost; the median coupon rate is 7.5 percent. The new bonds would also have longer maturities, ideally 30 years. The beneficiary countries could use the proceeds from the RSBs to retire the outstanding balance on the current private external debt.

Figure 4: Share of debt versus share of debt service cost in 2021

Source: Author’s calculations using World Bank International Debt Statistics (2021).

The lower coupon rates on the RSB along with the longer maturity will lead to sizeable reductions in the debt burden to more sustainable levels. We conduct a simple illustrative simulation, which indicates that this scheme could reduce the debt service payments as a share of government revenues by up to 4 percentage points per year for the average developing country, cutting near half the debt service burden in many cases. We further estimate a total reduction in external debt repayment of up to $100 billion over the next five years. In the remainder of the brief, we document the deterioration in sovereign debt situation, review the challenges with the CF, and outline the case for a Brady-like plan.

Related Content

Authors

-

Acknowledgements and disclosures

We thank without implicating Homi Kharas, Vera Songwe, Giancarlo Perasso, and Steven Kamin for valuable comments on an earlier draft. All remaining errors and omissions are our own.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).