That Social Security (aka Old-Age, Survivors and Disability Insurance or OASDI) faces financial trouble is hardly news. For more than two decades annual reports of the Social Security Trustees, widely reported by national media, have conveyed the message that outlays would outpace revenues and that previously accumulated Trust Fund balances would be depleted not long after 2030. The most recent projection puts the depletion date at 2035. At that point, in the absence of policy changes, the Trust Funds1 would be depleted and benefits would be cut immediately below those scheduled in current law by about 17% and more in later years.2

Despite these warnings, Congress has done nothing to close the gap, nor has any president over the last dozen years, Republican or Democratic, made closing the gap a high priority.3 Neither 2024 presidential candidate has addressed the problem directly beyond vague generalities. However, Donald Trump has put forward two non-Social-Security proposals that would deepen the funding gap and hasten Trust Fund depletion.

How did the financing problem arise? Why have elected officials failed to deal with a funding gap in America’s most popular government program, one that currently provides cash benefits to millions of beneficiaries, thereby keeping more people out of poverty than any other government program, and that provides a financial backstop for most Americans if they become disabled and when they become old and for their families when they die? What are the policy choices elected officials—and, more importantly, the American public—must eventually make? Closing the financial gap must top the agenda. But not far behind should be consideration of whether and how Social Security should be amended in recognition of the profound changes the American economy has undergone since 1983 when Congress last enacted major Social Security legislation. Meanwhile, inadequate budgets for program administration threaten to prevent the Social Security Administration (SSA) from providing adequate service to new applicants and current beneficiaries.

How did the funding gap arise?

The seeds of the current gap were sown four decades ago, when Social Security faced problems much like those the nation will face in 2035 if Congress takes no action before then. The trust funds in 1983 were close to depletion. The system was far out of “close actuarial balance,” a term used to describe the program’s long-term financial health. The system is said to be in close actuarial balance if the gap between revenues and expenditures differs from revenues by no more than 0.5% of taxable earnings projected over the next seventy-five years. In 1983 the gap was 1.82%. Trust fund balances now are heading to depletion in 2035, and the gap is 3.50% of taxable earnings projected over the next 75 years.

Legislation enacted in 1983 solved both problems—imminent trust fund depletion and long-term imbalance. It raised taxes and cut benefits enough to keep Trust Fund balances positive in the near term. Given assumptions made then, the legislation restored Social Security to close actuarial balance over the period from 1984 through 2059. During the first part of this 75-year period, Social Security was projected to run surpluses, leading to the build-up of sizeable reserves. During the latter part of the period, Social Security was expected to run deficits. The reserves accumulated early on would just offset the deficits in the later period.

Although the system was projected to be in close actuarial balance over the period from 1984 through 2059, this pattern of “surpluses early on followed by deficits” guaranteed that the program would gradually slide out of balance. As the projection window crept forward, successive projections would lose one early surplus year and pick up one later deficit year. Even if every assumption used in 1983 exactly foretold future events, Social Security would today face a projected funding gap of 2.38%, about two-thirds as large as the one we now face and considerably larger than the one Congress faced then.4

Unfortunately, some economic and demographic assumptions made in 1983 proved to be too optimistic. Earnings inequality unexpectedly increased. As a result more earnings growth accrued to people with earnings above the Social Security taxable maximum than was anticipated and, hence, was not subject to payroll tax, thus reducing revenues relative to projections. Disability awards also exceeded projections, thus increasing spending relative to projections. These are the principal explanations for why the projected long-term funding gap is 3.50% in 2024 rather than 2.38%. By 2035, when the trust funds are projected to be depleted, the long-term deficit will be even larger.

Any plan that Congress devises to close the long-run funding gap can avoid repeating the design flaw in the 1983 legislation that caused projected deficits automatically to emerge. A plan designed to equate revenues and expenditures not only on average over 75 years but also in the last year would avoid that problem. Such a plan would achieve “sustainable solvency,” which would mean that Social Security would remain in approximate balance if the economic and demographic assumptions underlying the plan are close to accurate.

The Social Security spending gap is projected to be approximately 1% of GDP in 2035. Viewed in this light, the challenge seems quite manageable. It is comparable to budget challenges that Congress has handled in the past. But it is occurring against the backdrop of general budget deficits larger than any the United States has experienced since World War II during periods of full-employment and at a time when bipartisan cooperation seems to be mostly out of reach.

Related Content

Why hasn’t Congress done anything about the funding gap?

As the consequences of trust fund depletion are dire, the repeated warnings of the need to act have long been so clear, and the funding gap, relative to the whole economy, is seemingly manageable, why has no recent administration, Republican or Democratic, seriously tried to close it? And why have the current presidential candidates said so little about it?

The simplest way to eliminate the Social Security funding gap would be to allocate “general revenues”—taxes that fund general government activities—to fill it. But this “solution” has two serious drawbacks. First, it would boost government deficits. Second, it would violate the longstanding principle that Social Security should be financed by clearly identified, earmarked taxes. The motivation for running Social Security operations through trust funds distinct from the rest of the budget was and remains to discourage elected officials from boosting benefits, especially tempting in election years, without specifying how to pay for them. But if general revenues are not used, officials must either cut benefits or raise taxes, actions that are odious to one or both of the parties.

Furthermore, Social Security had sizeable trust fund balances at the beginning of the 21st century, topping out at a bit more than three and one-half times annual program outlays in 2008, which made procrastination possible.5 Senate procedures are also a barrier to action–any Social Security bill may be filibustered. That means that successful legislation requires at least 60 Senate votes, a threshold that no president has enjoyed since the death of Democratic Senator Edward Kennedy during President Barack Obama’s first term. More than 85% of Congressional Republicans have signed pledges not to raise taxes, and most Democrats (and many Republicans) are loath to cut benefits, especially for current beneficiaries and those soon to be eligible. With Congress closely divided between the parties, compromise on an issue as sensitive as Social Security seems almost fanciful.

Strategies for closing the gap

When elected officials get around to addressing the funding gap, they will have to choose among many possible ways to lower (or possibly raise) benefits, many possible ways to raise (or possibly lower) payroll and income taxes now earmarked for Social Security, or whether to borrow more from the public–that is, raise budget deficits–in order to prevent the benefit cuts that would occur automatically if nothing were done.6

Cutting benefits. To appreciate the many ways benefits can be cut, it helps to understand how benefits are computed. The choice among possible cuts is important, because it determines whose benefits are cut and by how much, whether everyone is affected or only high earners, and whether the cuts affect all or only some beneficiaries.

The Social Security Administration keeps track of the earnings of all covered workers. The first step in determining workers’ benefits is to calculate their average indexed monthly earnings. This number is based on the worker’s 35 highest earning years (shorter periods for some Disability Insurance claimants). Past earnings are adjusted for the change over time in average earnings per worker. Each worker’s “standard benefit”7 in 2024 equals 90% of the first $1,174 of average monthly earnings, 32% of earnings above $1,174 but below $7,078, and 15% of earnings above $7,078 but below the taxable maximum. Married couples receive the sum of each spouse’s benefits or 1.5 times the higher earner’s benefit, whichever is larger. The thresholds at which the benefit percentages change, called “bend points,” increase each year by the same percentage as average earnings. Adjusting past earnings and bend points for past growth in average earnings assures that benefits keep pace with general earnings.

Workers who claim old-age benefits at age 67 receive the standard benefit. But they may claim reduced benefits as early as age 62, in which case their actual benefit is reduced 30%. If they wait until age 70 to claim benefits, they receive 24% more than the standard benefit. The benefit adjustments are prorated so that, on average, claimants will receive approximately the same benefits over their lifetimes. Disability Insurance beneficiaries receive the standard benefit whenever they qualify. Other adjustments are made for families with children or other qualifying dependents and for survivors. All Social Security benefits are adjusted annually for increases in the Consumer Price Index (CPI-W).

Benefits could be cut in numerous ways. Congress could lower replacement rates—the ratio of each claimant’s benefits to average earnings—and they could do so abruptly or gradually over time. For example, increasing bend points with prices rather than with average earnings would mean that benefits would keep up with prices, not wages. So-called “price indexing” would hold the purchasing power of benefits constant at given price-adjusted earnings, but as wages typically grow faster than prices, benefits would fall for claimants at a given relative position in the earnings distribution. Switching to price indexing would not affect the benefits of those already on the rolls when the change takes effect. Over the long haul, price indexing would cut benefits by progressively larger percentages, eventually by more than half on average. The cuts would be larger for low earners than for high earners. Alternatively, Congress could apply price indexing only to workers with relatively high earnings. That approach would insulate low earners from the cuts. Another way to cut benefits would be to increase the number of years used to compute average earnings.8

Benefits could be increased by raising the replacement rates for everyone, or benefit increases could be focused just on low earners, for example by boosting the first replacement rate from 90% to some higher fraction or by applying the current or increased replacement rate to more earnings.

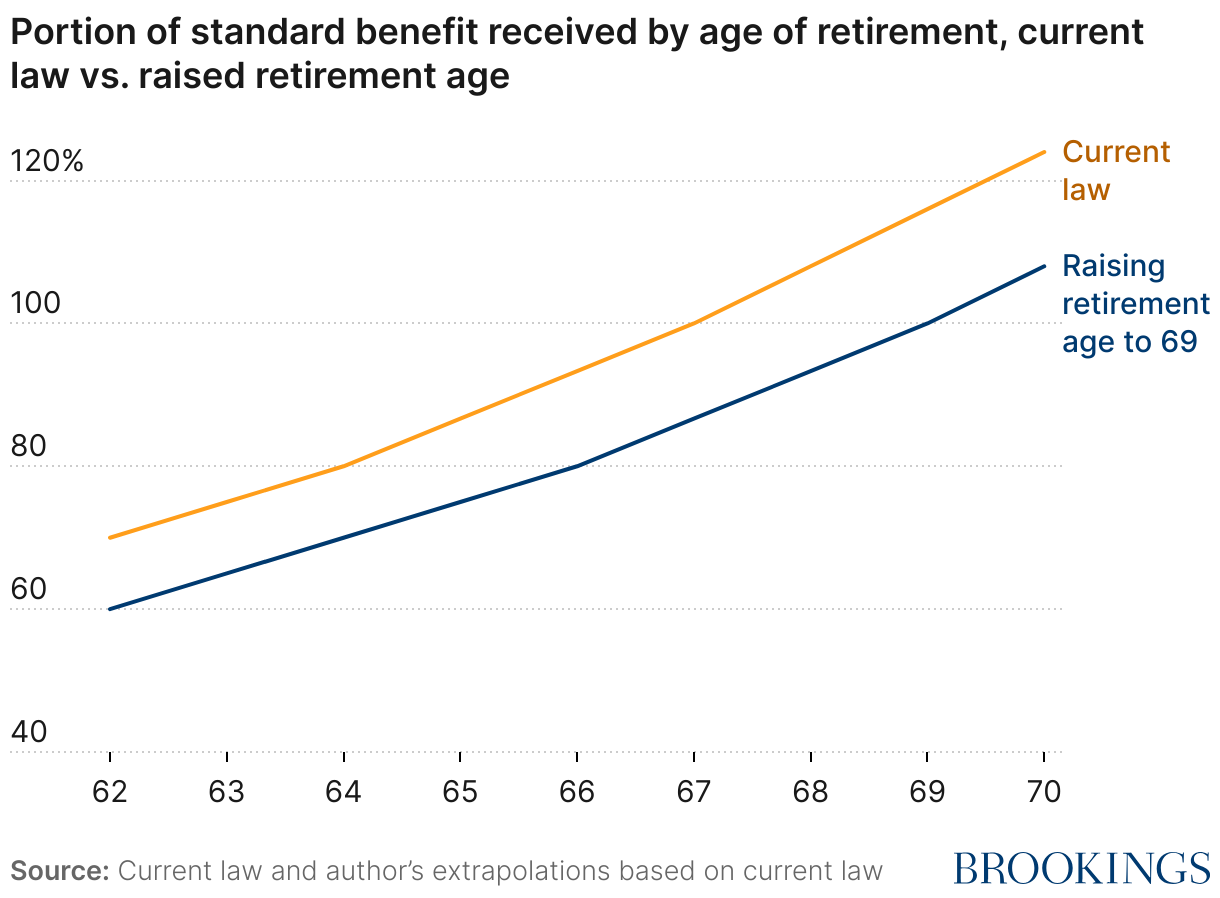

One widely discussed way to cut benefits would be to raise the age at which workers qualify for the standard benefit from 67 to some older age. This change is often called “raising the normal retirement age.” However, that term is misleading, as boosting the age at which the standard benefit is paid would not necessarily alter the age at which benefits are claimed or when workers retire. Instead, it is an across-the-board cut for all new claimants of Old-age Insurance (see Figure 1). Workers claiming benefits at, say, age 68 would receive the benefit now paid to workers who claim at age 67, instead of the somewhat larger benefit that they now receive. Deferring claiming sacrifices benefits for the duration of the deferral. Either way, raising the age at which workers receive the standard benefit amounts to a benefit cut for all old-age claimants. Those already on the rolls would be unaffected, as would Disability Insurance beneficiaries, who receive the standard benefit regardless of the age at which they qualify.

Reducing the inflation adjustment after benefits are being paid would affect all beneficiaries, those now on the rolls as well as those yet to claim. In 1983, Congress included a one-time reduction in the inflation adjustment which affected those then receiving benefits but not future claimants. Giving less than full adjustments for price inflation would cut benefits, increasingly the longer a beneficiary has been on the rolls. Switching the index used to account for inflation to an index based on the market basket purchased by the elderly—the CPI-E—is expected gradually to increase benefits, as that index weights housing and health care more heavily than the general CPI, and prices of housing and health have risen faster in most past years than the prices of other goods.9 But there is no guarantee that this differential will persist.

Raising revenues. The simplest way to raise revenues is to increase the payroll tax rate. For example, boosting the payroll tax rate from 12.4% to 16.2% would bring Social Security into approximate close actuarial balance for the next 75 years. Another way to raise revenues is to increase the taxable maximum. Some proposals would raise the taxable maximum so that 90% of earnings would be subject to tax, the same share as in 1983 after the last major legislation. Or the taxable maximum could be removed altogether so that all wages and salaries are taxed. Yet another way to increase revenues would be to broaden the base of the 12.4% tax to include some forms of capital income as well as employer-financed health insurance and other fringe benefits. The current income tax on part of Social Security benefits that is now returned to the Trust Funds could be broadened. General revenues or revenues from other taxes, such as the estate and gift tax, could be earmarked for Social Security.

Each of these ways to boost Social Security revenues would fall differently across the income distribution. Those with earnings greater than the current taxable maximum would bear the full burden of raising or removing the ceiling on taxable earnings. Taxing fringe benefits would not burden those with earnings already above the taxable maximum and, by definition, would not affect those without such fringe benefits. Taxing capital income would burden those who receive capital income, predominantly those with comparatively high incomes. The ultimate burdens of each change would depend on the degree to which the tax change causes employers to change compensation packages.

Should newly taxed income be used in computing benefits? Boosting the taxable maximum or broadening the tax base raises the knotty question of whether the newly taxed income should be used in computing benefits. With minor exceptions, benefits have always been based on previously taxed earnings.10 This practice has created a general sense that workers have earned their Social Security benefits. That sense is politically significant as it stiffens resistance to benefit cuts.11 This belief that workers have earned their benefits helps explain why virtually all workers claim Social Security when they are eligible to do so. In contrast, one-sixth of those eligible for food subsidies and, in some states, more than 80% of those eligible for “welfare” (aka Temporary Assistance to Needy Families) fail to apply for benefits to which they are legally entitled.12

Not including newly taxable income in computing benefits would, at least to some degree, undermine the politically important sense that Social Security benefits have been earned. Furthermore, Congress has always intended that Social Security should ensure only a core income to workers when they become elderly or disabled or to close relatives if the worker dies at a young age. For that reason, it is hard to see why government should use its limited ability to levy taxes to finance increased pensions for people with high earnings or income. At the same time, failing to include newly taxed earnings in the computation of benefits for those with high incomes or wealth would threaten the earned-right principle and possibly saddle Social Security with the stigma similar to that associated with income- and means-tested payments that many potentially eligible beneficiaries do not claim. And, in the case of raising the taxable maximum, it is doubly hard to see why an additional 12.4% tax should be imposed only on high earnings but not on other forms of income.

Demographic and economic developments since passage of the last major Social Security legislation four decades ago have raised other questions. The now dominant norm of two parents working outside the home presents a dilemma to many couples with young children—pay for financially burdensome daycare or sacrifice the earnings of one parent. If one parent stays home, those parents will have years when they earned nothing, which will later depress the Social Security benefits to which they are entitled. Much the same problem confronts workers who spend many years out of the paid labor force caring for elderly or disabled relatives—an increasingly serious matter as life-expectancies have increased. Rising life expectancies also mean that long-term beneficiaries may have spent down any assets that they once had.

Numerous draft bills have been introduced to ameliorate these problems. For example, various bills have proposed to help parents of young children by reducing the number of years of earnings used in computing their standard benefits. Such a step would allow one parent to leave the labor force to care for a young child or a sick or disabled dependent without having years of zero earnings.

Such proposals raise difficult problems of policy and administration. Should such “drop-out” years be provided for just one child or for more? Should the drop-out years be given if the parent has part-time earnings? If drop-out years are allowed to parents of young children, should they also be allowed to people who care for aging or incapacitated parents or other relatives?

A variety of proposals would use Social Security to counter poverty among the elderly and long-term beneficiaries. Some would update a provision enacted years ago to provide higher benefits than the current general formula does to people with a lifetime of low earnings.13 Others would provide a one-time increase to old-age beneficiaries over some age, such as 80 or 85, or to all beneficiaries who have been on the rolls for more than a specified period.

These proposals are intended to deal with real problems. But recent analysis has shown that increasing Social Security benefits is not the best way to help financially distressed beneficiaries.14 Supplemental Security Income (SSI), another program administered by the Social Security Administration, more accurately targets monthly cash payments to people who have low incomes and negligible assets.

Unfortunately, inflation has tightened SSI asset thresholds, which were set at $2,000 for single persons and $3,000 for couples in 1989 and have not been updated since. Had these asset thresholds been adjusted for price inflation since then they would now be more than twice as high—over $5,000 for individuals and over $7,500 for couples. Furthermore, every dollar of Social Security benefits beyond $20 per month now reduces SSI payments dollar-for dollar. Thus, increases in Social Security benefits now would would do nothing for anyone who is eligible for both programs. Complex rules discourage eligible individuals and couples from applying for payments and absorb scarce SSA administrative resources from more urgent matters.

Simple legal and administrative changes to SSI could convert that program into one better designed to aid Social Security beneficiaries in financial distress. These changes include raising asset limits—a step that currently enjoys bipartisan support—and allowing SSI recipients to keep more than $20 per month in Social Security benefits. To encourage those who might be eligible to apply for SSI, SSA could inform Social Security beneficiaries that they might also be eligible for SSI and help in completing an application. There are good prospects for raising asset limits as that change enjoys bipartisan support.

What reform efforts lack: A focus on administration

To make public programs work well, effective administration is as necessary as well-designed legislation. This maxim of good government is particularly relevant for Social Security. Thousands of rules and regulations must be applied as fairly, uniformly, and expeditiously as possible across the United States and its territories. To do its job, SSA must keep track of earnings for nearly 200 million covered workers, compute and deliver monthly checks accurately and on time to nearly 75 million beneficiaries, answer millions of enquiries each year, and determine whether millions of applicants for disability benefits under Social Security and SSI have impairments serious enough and (for SSI) have income and assets low enough for them to receive monthly income support.

The 2023 cost of administering Old-Age Insurance and Survivors Insurance (OASI) (0.34% of benefits paid) and Disability Insurance (1.78% of benefits paid) is remarkably low compared to the costs of similar private insurance, even if one allows for the added costs private insurers must incur to collect premiums. The higher cost of administering SSI—7.7% of payments—reflects not only the cost of determining initial eligibility but also the statutory requirement to monitor recipients’ incomes and net worth on a continuing basis. In recent years, SSA’s administrative budgets have not kept pace with increasing workloads. If administrative budgets continue to grow less than rising workloads, the quality of administration will suffer.

A single example may illustrate why it is essential to spend enough to fund adequate administration. Applicants for disability benefits through Social Security Disability Insurance or Supplementary Security Income apply initially to state-managed centers. Denied applications are routinely reconsidered. On average these two steps take six to eight months, although there is large variation from state to state.15 Applicants denied at reconsideration may apply for a review by an administrative law judge (ALJ), in the course of which they may submit new medical information. The time for an ALJ decision is highly variable, ranging recently from 128 to 707 days across 163 hearing sites.

What these numbers mean is that while applicants are awaiting a decision, some in a few months, others in two years or more, none can engage in what is called “substantial gainful activity,” which means earning more than $1,550 per month. The reason is that doing so while an application is under consideration would result in immediate disqualification. For that reason alone, delay in deciding a case threatens economic hardship. As recently as 2023, more than 1.7 million SSI and DI applicants were waiting for final disability decisions.16

Unfortunately, the problem threatens to get much worse if administrative budgets are not increased. The problem is that as workloads have grown, turnover among SSA disability examiners has risen nearly five-fold. Getting each newly hired replacement up to speed takes about one year, as they must learn how to apply hundreds of regulations and rules to medically complex cases. During that period, the productivity of experienced staff suffers as they divert time from processing claims to training the newly hired.

A recent study reveals the appalling consequences if current staffing levels are not increased.17 If turnover rates among Social Security staff return to past levels, and even if staffing at the initial disability determination stage is increased by 20%, the backlog will still increase to roughly 2.7 million and remain above current levels for at least a decade. If, in addition, staff to help administrative law judges make their findings more quickly is also boosted by a fifth, the backlog is projected to increase, but it would fall back to current levels by 2033. But if nothing is done, the number of Disability Insurance applications awaiting decision is projected to grow to more than 4.5 million.

Behind these dry statistics is potentially lethal hardship. Even now, millions of people, many of whom will eventually be found eligible, are effectively barred from substantial gainful activity while their cases are pending. In addition, SSI disability applicants must show that they lack income or significant assets. All are in limbo until decisions are made. During this waiting time, any skills they may have retained will atrophy. Even now, the number of people who are placed in such a financial bind is appalling. That this number should be allowed to double or more is revulsive.

This single example of the consequences of spending too little to retain staff and to establish pay and other working conditions that will retain them is deeply troubling. But it is only one of many tasks that SSA must perform if the provisions of the Social Security Act are to be put into effect as Congress intends.

The 2024 Republican platform pledges that a Republican administration “will not cut one penny from Medicare or Social Security,” that Social Security is a promise “to our seniors, ensuring they can live their golden years with dignity,” and that “Republicans will restore economic stability to ensure the long-term sustainability of Social Security.”

This stance is inconsistent with Donald Trump’s repeated comments that he will not touch Social Security or Medicare. Both programs face financial shortfalls that, if left untouched, will force major benefit cuts. The promise to do nothing, if honored, would allow trust fund depletion and the associated automatic benefit cuts to take place.

But Mr. Trump has also proposed two measures that would both hasten trust fund depletion and deepen the long-run funding gap. First, he has proposed to end income taxation of part of Social Security benefits. Currently, revenues from this source amount to about 4% of total revenues, a share that is projected to increase under current law. Eliminating this revenue source would accelerate trust fund depletion by about two years and deepen the long-run funding gap by more than 7%.18

He has also promised to deport up to 11 million current U.S. residents who are undocumented immigrants. If implemented, this policy would immediately reduce the U.S. labor force, earnings, and payroll tax revenue, hastening trust fund depletion. It would eventually reduce benefit payments but by a smaller proportion than trust fund income, as immigrant adults are younger, on average, than the native-born adult population. In addition, the disruption that would result from the abrupt departure of immigrant workers would likely cause additional losses, particularly in such industries as construction and agriculture where undocumented immigrants comprise a particularly large share of the workforce.

In addition, the platform contains two false statements. It says that “corrupt politicians have robbed Social Security to fund their pet projects,” which is untrue as all Social Security revenues are used to pay for benefits and program administration or are invested in government bonds guaranteed as to principal and interest. The platform also declares that a Republican administration will “secure our Borders to preserve Social Security.” On the contrary, reducing net immigration would increase Social Security’s funding gap, as explained in the annual reports of the Social Security Board of Trustees.19

“Project 2025,” the lengthy compilation of proposals intended to guide a future Republican administration prepared under the aegis of the Heritage Foundation by a group of authors that includes past Trump advisors, is silent on Social Security. The authors say that the 887-page document lacked space to address several issues, including Social Security.

Senior Republican members of Congress have been less reticent in the past. In 2010, Paul Ryan, who later became Speaker of the House of Representatives, presented a plan to allow the diversion of payroll tax revenues into newly authorized private accounts and otherwise to cut Social Security benefits by more than one-third. In some respects, this plan resembled an initiative put forward by a commission appointed by President George W. Bush which drew little support from Republicans and virtually none from Democrats. In 2016 former Republican chairman of the House Committee on Ways and Means, Sam Johnson, proposed legislation to cut Social Security benefits eventually by more than one-third. Those benefit cuts were large enough not only to close the funding gap but also to permit payroll tax cuts. Ryan and Johnson both proposed using then-existing trust fund reserves to enable a gradual phase-in of benefit cuts.

These proposals came to grips with a political dilemma—if payroll taxes or other revenues are not increased, then the only way to avoid benefit cuts is to borrow more from the public, which means boosting the budget deficit. Paradoxically, their candor in confronting this problem goes a long way toward explaining why those proposals drew little support. When Ryan and Johnson released their plans, sizeable trust fund reserves made it possible to phase in the benefit cuts gradually. Since then, trust fund reserves have fallen and are rapidly vanishing. That means that benefits will have to be cut abruptly unless Social Security revenues are increased or the nation is prepared to increase budget deficits.

In March 2024, the Republican Study Committee, comprised of some members of the House of Representatives, proposed to raise the age at which the standard benefit would be payable from 67 to 69. This action is equivalent to an across-the-board benefit cut of about 13% for all new old-age claimants. But they also promised, as did the Ryan plan earlier, not to cut benefits for those now on the rolls and those nearing retirement age. Keeping this hold-harmless provision will be impossible unless Social Security revenues are increased in some way—by boosting taxes, which an overwhelming majority of Republican members of Congress have pledged not to do, or by increasing the federal budget deficit. It is possible that, in the future, Republican Senators and Representatives might violate their “no tax increase” pledge. But without either boosting payroll taxes or transferring general revenues to Social Security, it is now mathematically impossible to sustain benefits for everyone now on the rolls or soon to be eligible. Thus, the stated Republican position is internally inconsistent.

The Biden administration has not pushed any major Social Security legislation since he took office. Some Democratic members of Congress have put forward much bolder proposals than Biden did during his presidential campaign.

Representative John Larson, ranking Democratic member of the subcommittee on Social Security of the Committee Ways and Means, introduced two bills to expand benefits and to close most of the funding gap. When the House Ways and Means Committee failed to report out the first bill, he introduced the second plan which would have gradually extended the full payroll tax to cover all earnings and net investment income. The bill would have used some of the added revenue to increase benefits but only for a time, after which they would revert to current law. Most of the revenue would be used to delay depletion of the trust funds by an estimated 32 years. Most House Democrats cosponsored the bill. The bill was the subject of subcommittee hearings, but the full Ways and Means Committee, which then had a Democratic majority, did not hold hearings, and the bill never reached the House floor.

Democratic Senator Sheldon Whitehouse, together with Representative Brendan Boyle, proposed tax increases much like those in the Larson bill but without any benefit increases. It would have converted the funding gap into a sizeable surplus. Senator Bernie Sanders also introduced draft legislation which, like Larson’s bill, proposed to apply the payroll tax to all earnings (but with a shorter phase-in than Larson suggested) and to apply the 12.4% tax to net investment income and to income from S corporations, which flow through each year from the business to its owners. Although Democrats controlled the Senate when these bills were introduced, no hearings were held.

Other Democrats, alone or jointly with a Republican in some cases, introduced bills with narrower scope that had little or no impact on the date at which the trust funds would be depleted or on long-term balance. The Larson bills were genuine, if unsuccessful, efforts to enact new law. The other proposals were “message bills”—draft legislation that publicly staked out a position but had no real prospect of passage. None had White House backing.

The 2024 Democratic platform repeatedly attacks Republican proposals for cutting benefits but says nothing, except in general terms, about what a Democratic administration would do to deal with Social Security’s financial shortfall. The platform advocates “strengthen(ing) the program and expand(ing) benefits by asking the wealthiest Americans to pay their fair share,” which means raising the taxable maximum, but it doesn’t specify by how much.

Neither presidential candidate and neither party has given voters much indication of how it will deal with Social Security or even whether it would push major Social Security legislation during the next four years. Each could follow the playbook of recent administrations and pass the issue to future elected officials. If they do so, full scheduled benefits would continue to be paid until either the trust funds are depleted or Congress decides to act. This course is likely, as whichever party wins will inherit a fractious Congress seemingly not given to compromise and troublesome budget deficits that many economists warn will carry serious long-term threats to economic wellbeing.

But there are reasons why each party might decide to deal with the issue now if it wins the White House and control of both Houses of Congress, even with narrow majorities. Should Democrats win the White House and both Houses of Congress, they will have an opportunity, possibly evanescent, to shore up the most important domestic social legislation of the last century, a prized program their party authored and has perennially defended. Some Democrats are averse to cutting a compromise deal with Republicans because they believe that when the trust funds are depleted Republicans will have no viable political option other than to use tax increases or budget deficits to sustain benefits. This rationale for delay is entirely unpersuasive, however. Past Republican proposals would have cut benefits gradually over time and used increased government borrowing (aka deficits) as well as Trust Fund reserves to smooth the transition. As Republicans have demonstrated a clear willingness to enact deficit-increasing tax cuts, there is little reason to doubt that they might pursue deficit-increasing plans to cut Social Security.

If Republicans win the presidency and control of Congress, they too will have an incentive to act. With large deficits hanging over budgetary debates, they would be in the best position in years to argue, once again, that those deficits should be lowered over time and that curtailing growth of spending on Social Security, Medicare, and other cash and in-kind assistance is a better way to lower deficits than raising taxes. They could argue that it is worth incurring temporarily increased deficits to rein in what they regard as excessive social spending.

It is far from certain that either party, if victorious in November, will decide to spend its energy and limited political capital on Social Security legislation. But one thing is clear: If they do, who wins the 2024 election will have a profound effect on Social Security, which means a profound effect on everyone who now receives benefits or hopes to do so in the future.

Author

-

Acknowledgements and disclosures

The Brookings Institution is financed through the support of a diverse array of foundations, corporations, governments, individuals, as well as an endowment. A list of donors can be found in our annual reports published online here. The findings, interpretations, and conclusions in this report are solely those of its author(s) and are not influenced by any donation.

-

Footnotes

- Social Security consists of three programs: Old-Age Insurance, Survivors Insurance, and Disability Insurance (DI). The first two operate through one trust fund (the OASI fund), the third by another (the DI fund). The two are legally separate. Revenue from the 12.4% payroll tax is divided between the two funds—10.6% to OASI and 1.8% to DI. The trust funds also receive revenues from the income taxation of a part of Social Security benefits, which accounts for about 4% of total income. Given this division, current projections indicate that DI will be adequately funded for the next 75 years and the OASI fund will be depleted in 2033. If the operations of OASI and DI are considered together, depletion of the combined funds would occur in 2035, based on the most recent projections. As Congress has varied the distribution of the payroll tax between the two funds for various reasons, including when one of the two funds faced depletion much sooner than the other, and may be expected to do so in the future, I shall refer to “the Trust Funds” as if they were a single entity.

- Just how benefits would be cut is not specified in law. The Social Security Administration would have considerable discretion. It could lower benefits and send them out on time. It could maintain benefit amounts but delay payment. It might delay the onset of payments for new claimants and pay benefits for old claimant more promptly.

- During the 2020 presidential campaign, Joe Biden issued a plan that would have slightly increased benefits and raised revenues a bit more but that would have done little to close the long-term funding gap. After election, however, he did not push the plan. See Karen E. Smith, Richard W. Johnson, and Melissa M. Favreault, “How Would Joe Biden Reform Social Security and Supplemental Security Income,” Urban Institute, October 2020.

- The 1983 legislation was crafted initially by a commission appointed by President Ronald Reagan. Some members of that commission recognized that Social Security would drift into projected imbalance are recommended enacting tax increases for future years to forestall that effect. But the Commission did not include this recommendation in its final report, and Congress did not include it in the bill that it finally enacted.

- The absolute size of the trust fund continued to grow slowly until 2020, but outlays grew faster after 2010, causing the ratio of the fund to outlays to fall steadily.

- The Office of the Chief Social Security Actuary periodically releases a compendium briefly describing changes to Social Security proposed by members of Congress or by major private organizations. This compendium includes estimates of the impact of the proposals on long-term actuarial balance and on the balance of the system in the last year of the projection period. See Office of the Chief Actuary, “Summary of Provisions That Would Change the Social Security System,” September 27, 2023.

- The Social Security Administration uses the term “primary insurance amount” for the standard benefit.

- Average earnings are now based on the 35 years of highest earnings. If average earnings were based on more years of earnings, the additional years of earnings would necessarily be lower than the 35 years of earnings now used. The resulting average would necessarily be lower than the current one.

- The CPI-E has risen faster than the regular CPI in the past, but whether it will do so for the next 75 years is not obvious, as health costs depend on technological changes that will affect health costs in unpredictable ways and housing costs also depend on factors that may differ from the past.

- The principal exceptions are the revenues from income taxation of part of Social Security benefits and general revenue transfers to cover the cost of credits given retroactively to former members of the armed forces for compensation they received while in the armed forces at a time when members of the military were not covered by Social Security.

- Although there is a belief among workers that rights to Social Security have been earned and that they are, in some sense, entitled to them, the Supreme Court ruled in 1960 that Congress could cut or even eliminate benefits if it wished to do so.

- Participation in Temporary Assistance to Needy Families, a joint federal-state program administered by states under different procedures and with varying benefits and eligibility rules, ranged widely across states in 2016-18, from over 50% in New York, California, Oregon, and the District of Columbia to less than 10% in seven states, mainly in the Deep South. See Government Accounting Office, Temporary Assistance for Needy Families: The Decline in Assistance Receipt Among Eligible Individuals, April 10, 2023.

- This provision, enacted many years ago, used an earnings threshold to limit eligibility only to low earners. But the threshold was indexed only for prices. As earnings have risen, fewer and fewer people have been eligible.

- Jack A. Smalligan, “Increasing SSI benefits is a more effective approach to reducing poverty than an enhanced Social Security minimum benefit,” The Brookings Institution, May 14, 2024. See also, Kathleen Romig and Sam Washington, “Policymakers Should Expand and Simplify Supplemental Security Income,” Center on Budget and Policy Priorities, May 4, 2022.

- These steps require on average fewer than 100 days in Iowa, Idaho, Pennsylvania, and New Jersey, but more than 300 days in Georgia and Mississippi. See https://www.ssa.gov/securitystat/disability-processing-time/.

- ALJ decisions are not quite final, as denied applicants may appeal their cases to higher administrative review or to the courts. In fact, few do so, and fewer still are approved after ALJ denial.

- Stephen J. Goss and Michael L. Stephens, “Social Security Disability Claims Pending Determination: Past and Projected,” Actuarial Note 163, May 2024, Social Security Administration.

- THE BOARD OF TRUSTEES, FEDERAL OLD-AGE AND SURVIVORS INSURANCE AND FEDERAL DISABILITY INSURANCE TRUST FUNDS , THE 2024 ANNUAL REPORT OF THE BOARD OF TRUSTEES OF THE FEDERAL OLD-AGE AND SURVIVORS INSURANCE AND FEDERAL DISABILITY INSURANCE TRUST FUNDS, p. 51

- Trustees reports show the estimated positive effects of net immigration on trust fund balance. For example, “The cost rate decreases with an increase in total net immigration because immigration occurs at relatively young ages, thereby increasing the numbers of covered workers earlier than the numbers of beneficiaries.” THE 2024 ANNUAL REPORT OF THE BOARD OF TRUSTEES OF THE FEDERAL OLD-AGE AND SURVIVORS INSURANCE AND FEDERAL DISABILITY INSURANCE TRUST FUNDS, p. 191, May 6, 2024.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

A voter’s guide to Social Security

October 2, 2024