Ten Senate Republicans recently proposed a $618 billion COVID relief package. In this piece, we provide an analysis of that package and update our analysis of the Biden Administration’s $1.9 trillion fiscal package, using the current-law gross domestic product (GDP) projections that the Congressional Budget Office (CBO) released on Monday.

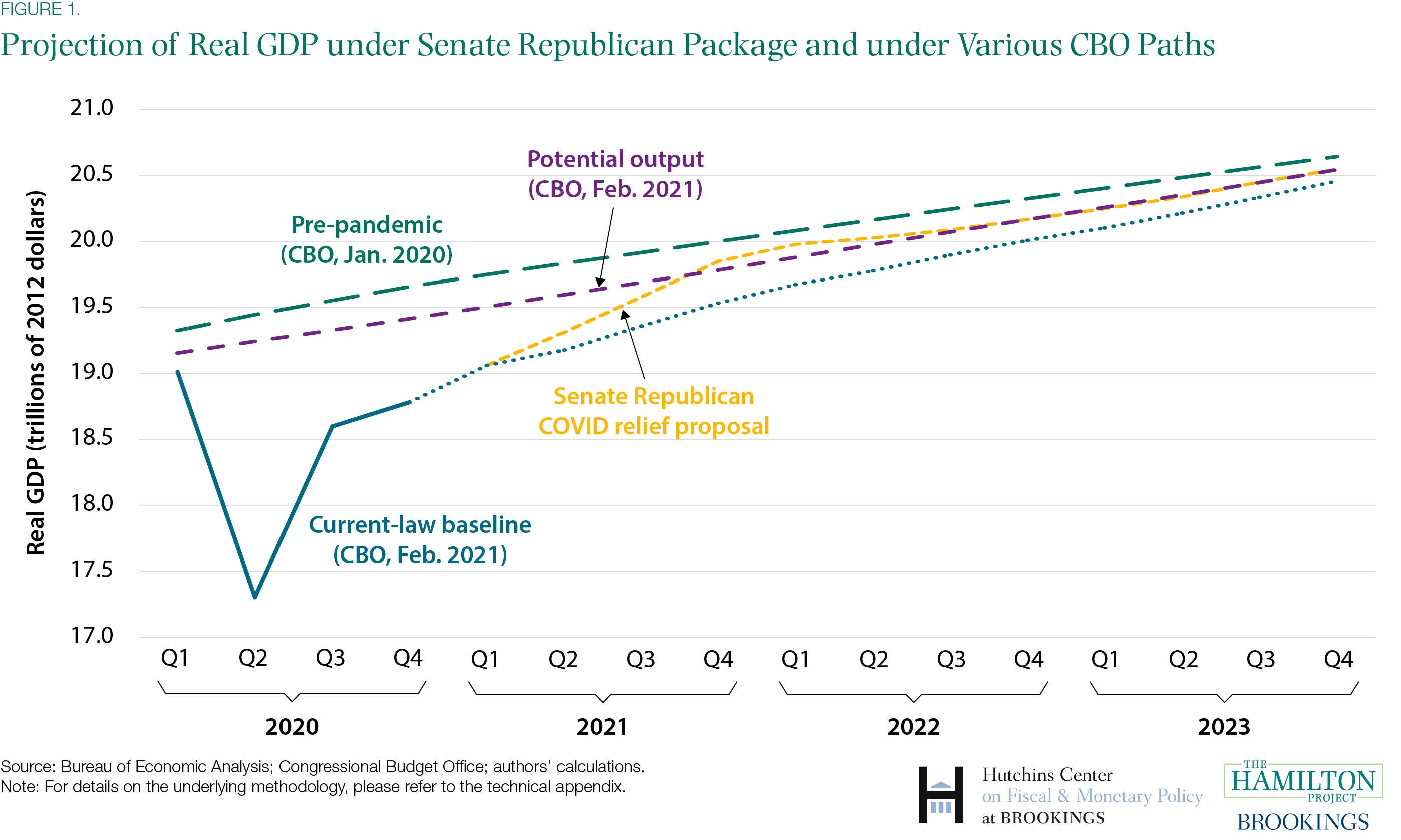

We estimate that the Republican plan would raise the level of real (inflation adjusted) GDP by 1.6 percent in the fourth quarter of 2021 and 0.8 percent in the fourth quarter of 2022, above the baseline level that CBO projects under current law (which assumes no additional fiscal support). This would leave GDP about 0.8 percent below its pre-pandemic trajectory at the end of both and 2021 and 2022, but a touch above CBO’s estimate of potential GDP—the maximum sustainable level of output (see figure 1).

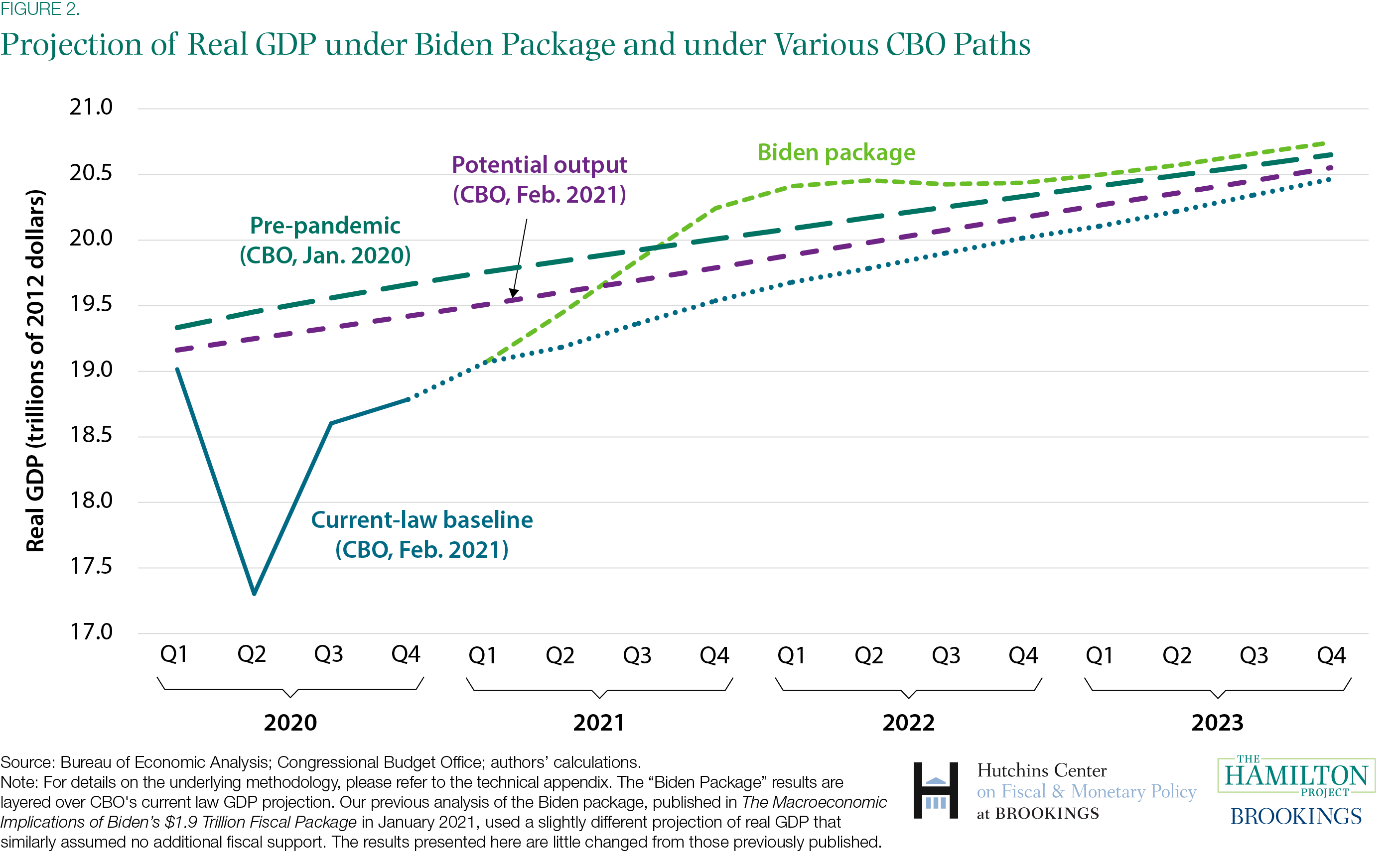

We estimate the Biden package would result in real GDP exceeding its current-law baseline by 3.6 percent at the end of 2021 and 2.1 percent at the end of percent in 2022 (see figure 2). (As described below, our analysis of this package is updated only insofar as we now use CBO’s current-law projection as our baseline in place of our own projection that also assumed no additional fiscal support). [1] In addition, real GDP would rise above its pre-pandemic path, meaning that some of the economic activity lost during the pandemic would be made up. We estimate that the positive output gap between GDP and CBO’s estimate of the maximum sustainable level would peak at 2.6 percent in the first quarter of 2022. That positive output gap would likely put upward pressure on inflation, which the Federal Reserve has said would be welcome. However, the temporary surge in economic activity would also create a risk that the return of GDP back down to potential could create a difficult economic period after 2021.

Of course, as we have written, these plans should be judged not only on their macroeconomic impact, but also on the extent to which they adequately invest in COVID-19 containment and vaccination and provide needed relief to help households and businesses weather the pandemic. Still, an analysis of the likely effects on GDP should be an important part of the debate.

How We Analyzed the $618 Billion Senate Republican COVID Relief Package

The methodology we use to analyze the $618 billion Senate Republican COVID Relief Package is similar to that detailed in our analysis of the Biden $1.9 trillion fiscal package. Briefly, we use information publicly available from the office of Senator Susan Collins (R-Maine) to divide the package into four categories, based loosely on our assessment of the extent and speed of the resulting increase in spending by households, firms, and government agencies. Those effects are referred to as marginal propensities to consume, or MPCs. We then apply a “fiscal multiplier”—an estimate of the increase in real (inflation-adjusted) GDP for each initial dollar of spending—to calculate the total GDP effect.

The four categories—and the dollar amounts by category–are as follows:

- COVID-19 containment and vaccination, aid to state and local governments, and increased federal spending ($204 billion): this category includes money for vaccination, testing and tracing, child care, and reopening schools;

- Direct aid to families ($220 billion): this category includes rebate checks of up to $1000 per person.

- Aid to financially vulnerable households ($144 billion): this category includes an additional $300 per week in unemployment benefits through the end of June and nutrition assistance programs; and

- Aid to businesses ($50 billion): this category includes loans and grants to small businesses.

Although we used the same categories to organize federal outlays under the Biden package, the MPCs and fiscal multipliers we used for the Senate Republican COVID Relief Package are slightly different. In particular, we use somewhat more front-loaded MPCs for outlays on COVID-19 containment and vaccination, aid to state and local governments, and increased federal spending, because the Senate package includes much less aid to states. With the smaller amount of aid going to government agencies being more targeted, we expect the money to be spent more quickly. In addition, we have nudged up our estimates of the MPCs from the rebate checks relative to those used to analyze the Biden package. We did that because the checks in the Senate Republican COVID Relief Package phase out at lower income levels and are less likely to be received by families who will save them. Finally, as shown in figure 1 above, under the Senate Republican Package, GDP only exceeds potential GDP by a touch and so is less likely to create supply constraints and boost inflation. As a result, we have used a slightly higher fiscal multiplier used to estimate the effects on real GDP. [2]

For our baseline projection—the path of GDP without any additional fiscal support—we use CBO’s projection from February 1, 2021. In our previous analysis of the Biden package, we used a slightly different projection of real GDP based on our own analysis that similarly assumed no additional fiscal support. For the figures presented here, we have re-estimated the effects of the Biden $1.9-trillion package using CBO’s latest estimates.[3]

How Each Category is Estimated to Affect Real GDP

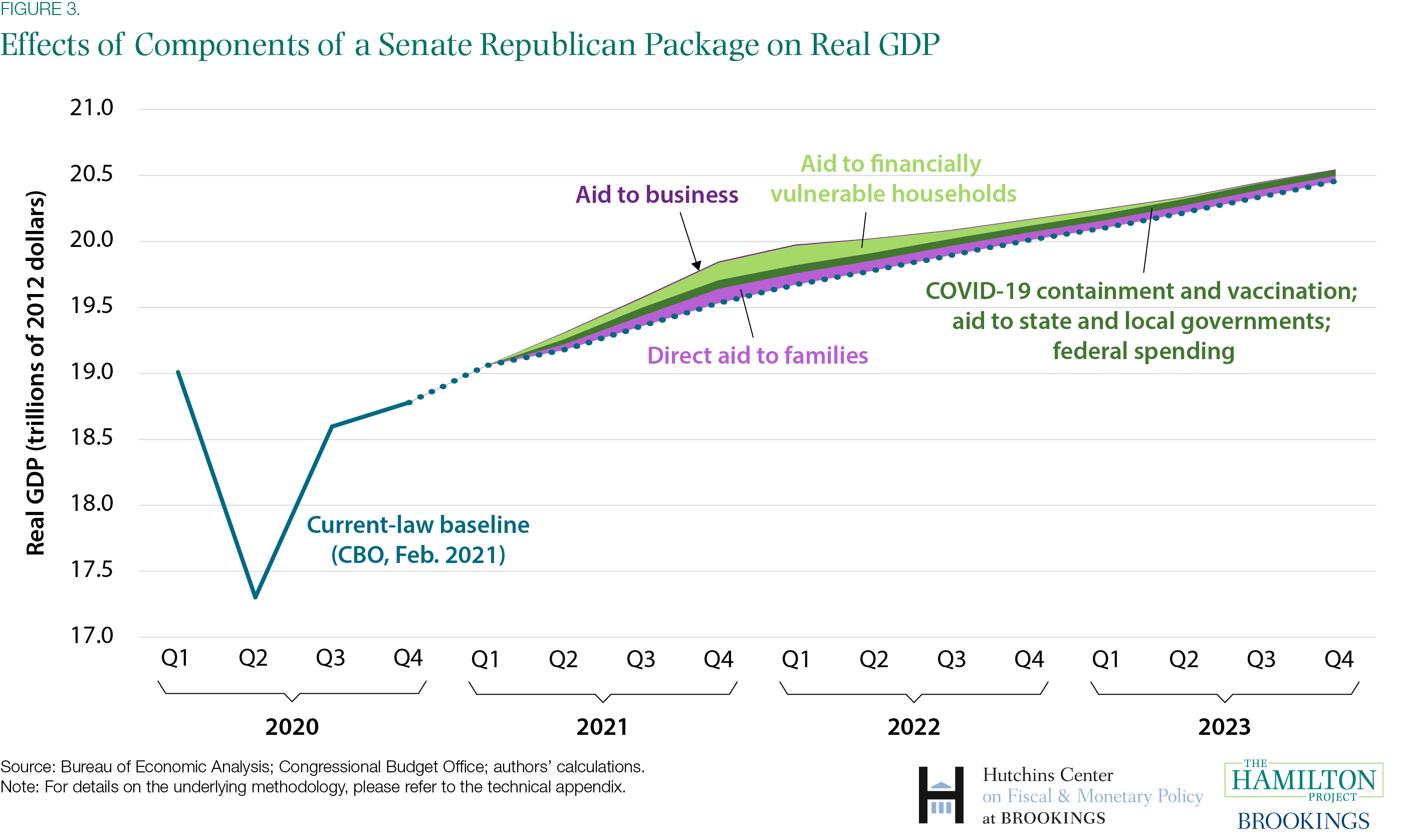

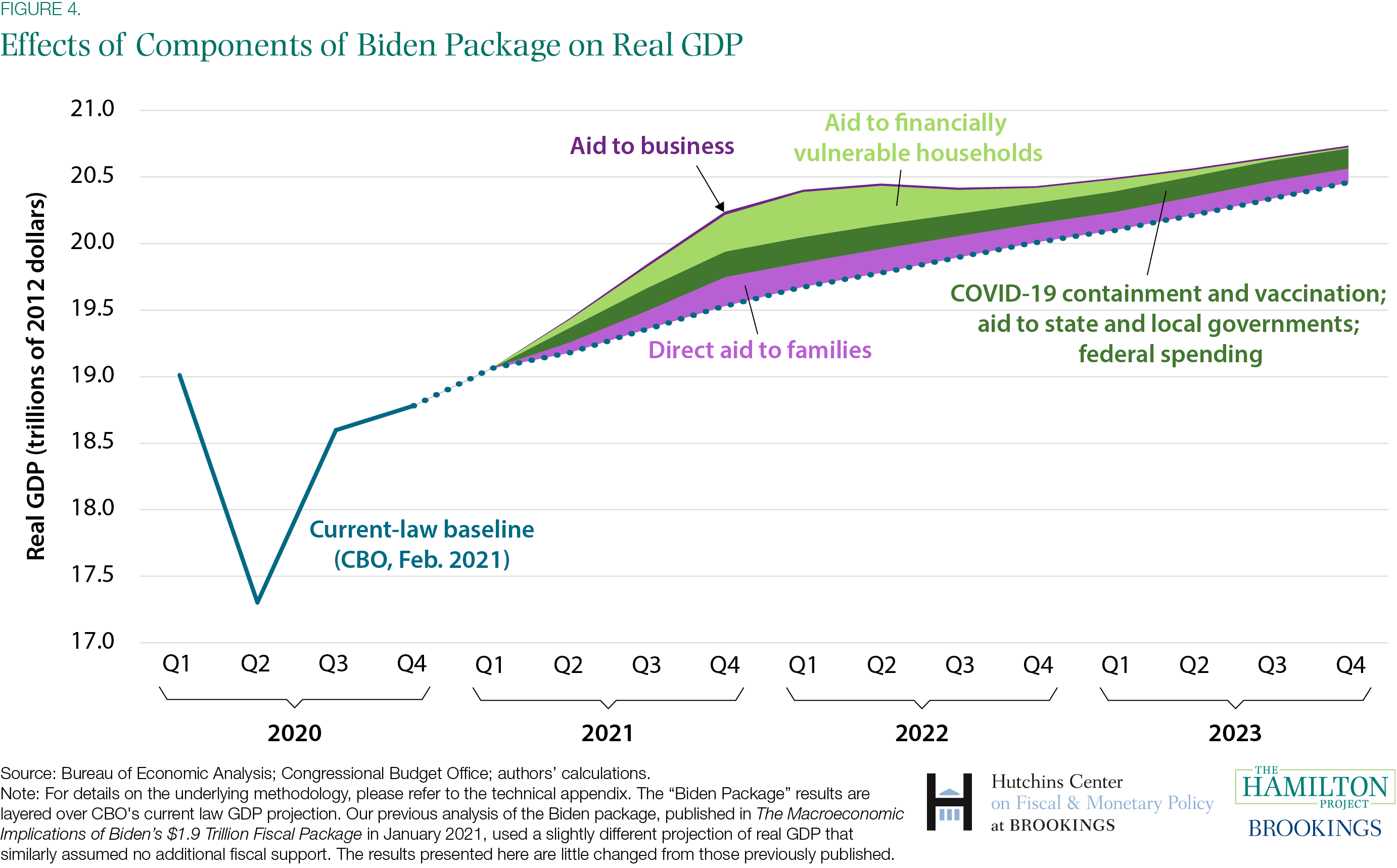

To show the estimated economic effects of the major components of the Senate Republican COVID Relief Package, figure 3 shows the breakdown of the effects on GDP by our four categories of aid layered over CBO’s current-law projection of real GDP. Figure 4 shows the same analysis for the Biden package.

Uncertainty

Our analyses of both the Biden $1.9 trillion plan and the $618 billion Senate Republican package are subject to great uncertainty. The path of GDP with no additional fiscal support is hard to predict, as it depends critically on the pace of the vaccine rollout and the response to the new more contagious COVID-19 variation. The increase in demand in response to additional fiscal support is also particularly uncertain, because there is no historical precedent to look to when trying to predict how quickly demand will return after a prolonged period of social distancing. Finally, the fiscal multipliers are hard to predict. That is particularly true given the Federal Reserve’s stated goal of getting inflation moderately above its 2 percent target for some time; it is, therefore, unlikely to tighten monetary policy even if, as we project, GDP modestly exceeds the maximum sustainable level for a time.

Footnotes

[1] These estimated effects of the increases in real GDP relative the baseline are unchanged from the analysis published in January 2021. The estimates are provided with more precision here.

[2] More precisely, we use a simple average of outcomes with the high fiscal multiplier and the low fiscal multiplier CBO estimates when the economy is weak and monetary policy is very accommodative. In analyzing the Biden package, we put 60 percent weight on the low multiplier and 40 percent weight on the high multiplier.

[3] The results presented here are very close to those we previously published. In particular, we continue to project that if the Biden package were enacted, GDP would reach the CBO’s pre-pandemic GDP projection after the third quarter of 2021, exceeding it by about 1 percent in the fourth quarter. And, we continue to estimate that with the $1.9 trillion package, the average amount of GDP through 2023 remains about 1 percent below its pre-pandemic projected path.

Authors

-

Acknowledgements and disclosuresThe authors thank Lauren Bauer and David Wessel for valuable feedback. Mitchell Barnes and Stephanie Lu provided exceptional research assistance. Jeanine Rees provided graphic design and Sara Estep provided superb research support.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

A macroeconomic analysis of a Senate Republican COVID relief package

February 3, 2021