Amid heightened geopolitical tensions and growing challenges posed by disruptive innovation, European policymakers are seeking ways to strengthen the continent’s strategic autonomy—particularly with respect to technology. A key part of this effort is the EU Chips Act, which provides billions in financial support to set up factories for advanced chip production (so-called “fabs”) and step up semiconductor research in the EU. Just as U.S. policymakers are attempting to strengthen the American semiconductor industry via the CHIPS and Science Act signed into law on Tuesday, lawmakers in Europe are attempting to build a more independent technology industry. First put forward in April by the European Commission, the EU Chips Act aims to address semiconductor supply shortages and years of decline in semiconductor investment in the EU, boosting Europe’s share of global chip production capacity to 20% from its current level of about 10%. The act is expected to be adopted in the first half of 2023 and has already had an impact on major semiconductor companies’ investment decisions.

The EU Chips Act represents a leading example of initiatives to improve Europe’s strategic autonomy on a range of technologies. The act joins up political, industrial, technological, and financial support in a key technological area; presents a clear plan for industrial and technological capability- and capacity-building; and takes a realistic approach to partnering with like-minded countries to enhance strategic control of the semiconductor industrial ecosystem.

The Chips Act in detail

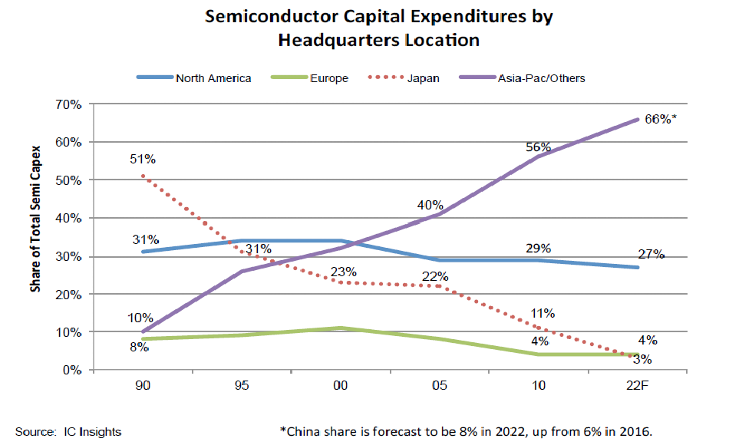

While the world’s major producers of semiconductors are stepping up their investments in current and next-generation chip design, European capital expenditure in this sector is on a decades-long decline.

The EU Chips Act aims to reverse this trajectory by launching a broad investment program along three lines of effort. The first pillar of the act supports large-scale technological capacity building and innovation in cutting-edge chips. The second pillar provides large-scale investments in production capacities. The third pillar aims to improve the ability to spot and respond to semiconductor supply crises.

The first pillar is centered around a public-private partnership billed as the “EU Chips Joint Undertaking,” which is composed of 25 EU member states, Israel, Turkey, Norway, the European Commission, and hundreds of companies and research centers. This pillar addresses semiconductor research, semiconductor pilot production lines, standards, certification for energy-efficiency and security of chips, skills, and networking of semiconductor expertise centers. It has a selective technological focus that includes chips design, advanced node technology as low as sub-2 nm, and quantum chips. By focusing on new technological paradigms (quantum), advanced chip designs (sub-2 nm), and new production methods (pilot lines that bridge “from lab to fab”), the first pillar aims to strengthen the EU’s position in the semiconductor pre-production phase. It provides both research and innovation funding and seeks to strengthen the industrial ecosystem by networking competence centers that offer semiconductor expertise and skills development across Europe. It also provides venture funding through a new Chips Fund for start-up, scale-ups, and smaller companies.

The second pillar enables setting up vertically integrated production facilities and what are called “Open EU Foundries,” which are fabs that produce chips designed by others for third parties. Both need to be “first-of-a-kind”—that is, they are not already present in the EU in terms of technology node, substrate material, or other product innovations that can offer better performance, process innovation or energy and environmental performance. Companies can access state aid and direct EU-funding and national funding amounting to about $30 billion (which should leverage further private funding) mainly for new fab construction. Companies will also benefit from fast-tracked administrative permits and priority access to pilot lines of the first pillar where they can test new production approaches. Established semiconductor producers, such as STMicroelectronics from France/Italy and Intel from the United States, are already gearing up for financial support from the second pillar.

The third pillar aims to ensure continuity of supply in case of a semiconductor crisis. This will be done by monitoring early warning indicators for shortages in chip supply relative to demand and escalation mechanisms to activate a semiconductor crisis stage. To head off a shortage, the EU Chips Act provides for coordinated procurement to be carried out and includes powers to implement a mandatory shift in production toward the production of scarce critical semiconductors by the companies under the second pillar—as a quid pro quo for the favorable investment conditions they receive. Details of early warning indicators are being developed and the list of companies concerned will grow over time as investment under pillar 2 is allocated.

Achieving strategic autonomy

Above all, the EU Chips Act aims at improving Europe’s strategic autonomy, which consists of the capabilities, capacities, and controls necessary to decide and act on one’s long-term economic, societal, and democratic future. Importantly, strategic autonomy is not only about industry, defense, and technology, but also concerns public policymaking, public service delivery, and “our” culture and democracy— what we value and what belongs to us, from the riches of our soil and the territory within our borders to digital assets such as health and industrial data. Rising geopolitical tensions, digital disruption, dominant platform companies, supply-chain crises related to the COVID pandemic, and rampant cyber-crime have fueled concerns among European policymakers that EU sovereignty and strategic autonomy are at risk—particularly with respect to technology. As a linchpin of the digital economy, a stable supply of semiconductors therefore represents a key step in the path toward European’s strategic autonomy.

Given its upstream position in the value chain, pillar one of the EU Chips Act, is at first sight the least political. By setting up a public-private partnership supporting design and piloting activities, pillar one feeds into pillar two, which is attracting the most attention given it is where the big money is being spent to build semiconductor capacity fully under European control. Together, pillars one and two build the long-term knowledge capabilities and production capacities necessary for semiconductor strategic autonomy. The third pillar of the act provides measures to monitor semiconductor supply chains, which will inform the EU’s long-term push to secure chip supplies. By understanding how these supply chains work, European policymakers will be better positioned to identify structural weaknesses beyond incidental disruptions—and guide further action to ensure the EU’s long-term economic security with respect to semiconductors.

Four months after it was introduced, there is some evidence that the EU Chips Act is already spurring investment. Early and promising signs include Intel’s commitment to build a $19 billion semiconductor fabrication plant in Germany as part of a stated investment in Europe of $90 billion. STMicroelectronics and GlobalFoundries signed up with the French government for a $6 billion fab in France. Other semiconductor manufacturers from the USA, Taiwan, and Europe are drawing up investment plans for Europe.

European policymakers recognize that cooperation with likeminded partners is a necessary element of strengthening strategic autonomy and are attempting to improve cooperation with their American counterparts on technology governance issues. Discussions at the Trans-Atlantic Trade and Technology Council (TTC) in recent months have included consideration about how to cooperate on warning mechanisms for semiconductor shortages. With both the United States and Europe developing measures to support the semiconductor industry, cooperation between these two blocs is crucial to void a subsidy race—a sure sign of tension between industrial and competition policy. The Paris-Saclay TTC statement from May declares that the two sides will aim to avoid subsidy races by respecting WTO rules and by establishing “common goals for incentives granted in respective territories and an exchange of information regarding such incentives on a reciprocal basis.” But this is a soft commitment, as it will be implemented by the two sides keeping one another informed on subsidies and establishing a direct consultation mechanism between key policy staff.

It is not yet clear what scale of investment will result from European and American policy proposals. The total EU investment from the EU Chips Act consists of an identified $43 billion, which is anticipated to spur additional private-sector investments of an equal amount, bringing the total to some $86 billion. Expectations regarding commensurate private-sector investments make it difficult to compare the dollar amounts in EU and US proposals contained in the recently adopted CHIPS and Science Act, which allocates $53 billion in funding to the semiconductor industry. Other countries are spending on a far greater scale, as is the case in South Korea, where the government is spending a staggering $450 billion on its chips industry. The difficulty in assessing the exact size of investment packages creates hurdles for policymakers trying to avoid subsidy wars.

So is the scale of EU investments sufficient to achieve strategic autonomy? First, absolute strategic autonomy is unlikely to be achieved, as dependencies on third countries will likely remain, including for rare-earth elements and other production materials necessary for advanced semiconductor manufacturing. However, the countries that produce those materials—most notably China—will likely remain dependent on the United States and the EU for designs or fabrication equipment. The resulting mutual strategic interdependence will need to be managed carefully, ideally in a way that improves rather than undermines strategic stability.

Second, the semiconductor market will require huge investments, with capital expenditure between now and 2030 estimated at $825 billion. A single fab may require up to $20 billion. To achieve the EU’s target of 20% production share, total semiconductor capital expenditure in Europe would have to be roughly $164 billion. For the United States to get back to the 37% share that it had in the 1990s from the current 12% would require over $300 billion. It is not clear how the gap between investment needs and funding from policy plans will be filled. Further strategic financial planning must be done to shore up the credibility of efforts to achieve strategic autonomy.

The EU Chips Act also does not mobilize all possible policy instruments. It does not have a plan for public procurement even if several of the promising markets involve strong public interests (security, defense, health). Neither does it discuss export controls nor specific guidance for foreign direct investment (FDI) scrutiny or partnering. Policy measures on skills and talent are underdeveloped and do not address underlying causes of brain-drain, such as the European innovation environment and salaries.

There is also the risk that political interest may start to wane. The European Commission wants to capture the moment and is attempting to speed passage of the Chips Act. Against the backdrop of geopolitical competition, both the United States and Europe should be concerned that they are not moving quickly enough. EU policymakers seem to be aware of this risk. Contrary to established practice in EU policymaking and because of the urgency of the chips crisis, the EU Chips Act was launched without an ex-ante impact assessment. The later published staff working document, therefore, makes for even more interesting reading as an ex-post justification. The document acknowledges with surprising candor that past semiconductor initiatives were largely unsuccessful due to a lack of political commitment and the industry’s short-term orientation. For now, the EU Chips Act has managed to raise the EU’s political commitment to the issue, which is likely to remain in years to come, not least due to unabating geopolitical and geoeconomic pressures. European firms in key industries like the automotive, telecom, and health sectors all want access to the advanced semiconductors described in the EU Chips Act, but it remains to be seen whether they will indeed create long-term demand for these goods.

Outlook for EU strategic autonomy

If European policymakers are to achieve strategic autonomy, they will have to address a whole range of strategic technologies. The EU Chips Act offers an indication of how they might do so. EU decision-making has recently become firmer, faster, and more freed-up from past taboos about industrial policy or addressing national security. The EU Chips Act has helped improve political interest in semiconductor initiatives—an issue that has undermined previous such efforts—and is strongly linked to the European industrial ecosystem. The act contains clear technological choices, even if the importance of quantum chips is hard to predict, and foresees that technological priorities can be adjusted.

Despite its strengths, the EU Chips Act should not to be used as a template for other technology areas. Rather, it provides lessons on how to tune future strategic autonomy initiatives to specific technologies. Let’s briefly consider a few areas: trusted cloud, quantum tech, and AI.

The EU’s trusted cloud initiatives—GAIA-X and EU-level secure cloud certification—have strong technological and industrial anchors in their technology roadmaps and links to the cloud ecosystem. But these initiatives lack political support. Is trusted cloud best pursued in a strategic partnership of the likeminded or rather as a global interest? Is it the role of governments to stay at the wayside as the market sorts out cloud security and trusted AI-based services or should public procurement be used to give direction? Stories of past, failed efforts to boost EU chip manufacturing—as laid out in the ex-ante staff working document—should be re-told to policymakers in order to spell out the risks of unclear political anchoring.

Quantum strategic autonomy needs to address quantum computing, quantum communications, quantum sensors, as well as post-quantum encryption. This involves a whole stack of basic hardware technologies, components, algorithms, software and services, and applications. The current EU quantum flagship initiative addresses much of this. This can be reinforced by the focus on quantum in the EU Chips Act. However, weaknesses must be addressed, notably the lack of political attention to the issue. Moreover, there is a dearth of European venture capital for quantum scale-ups.

AI and strategic autonomy should be of great concern for the EU. Artificial intelligence is another technology key to establishing tech sovereignty, but there is little technological focus and a rather weak European industrial ecosystem in AI. Politically, AI receives a lot of attention in Europe, mostly related to the proposed EU AI Act which aims to write rules around how to ethically deploy AI in the European market. On its own, however, this will not result in Europe attaining strategic autonomy for AI, just as GDPR did not bring the EU strategic autonomy in personal data protection.

The EU Chips Act shows that policy actions need to be strongly joined up in a credible strategic autonomy initiative. The EU Chips Act could provide an important contribution to a separate initiative on EU strategic autonomy in AI, given the advanced semiconductors that the EU Chips Act would deliver for AI applications and the great potential of AI in sectors in which the EU is strong, such as industrial automation, health and pharma, 5G/6G, and automotive.

There are many more strategic technologies and dependencies to consider (IoT, cybersecurity, digital ID, etc) and for each of these we can learn from the strengths and weaknesses of the EU Chips Act. The EU may be spurred into further action by China’s approach, which systematically tackles some 35 technology chokepoints with actions such as improving domestic industry and R&D, government purchasing, acquisition of foreign suppliers, leapfrogging, and copying or imitating. The EU also knows its strategic dependencies but does not have comprehensive plan to tackle them.

The EU Chips Act will likely be a trendsetter for how to advance the EU’s strategic autonomy. Even if it’s incomplete and weak in some regards, it paves the way for further comprehensive and realistic approaches to strategic autonomy in other areas—comprehensive in the sense that all critical dependencies that undermine sovereignty are to be addressed, realistic in the sense that strategic autonomy will have to be pursued in partnership and with a strategic approach to remaining dependencies. Ultimately, strategic autonomy policy must also be policy for living in an interdependent world.

Dr. Paul Timmers is a research associate at the University of Oxford, Oxford Internet Institute, a professor at the European University Cyprus, and a visiting professor at KU Leuven and the University of Rijeka.

Intel provides financial support to the Brookings Institution, a nonprofit organization devoted to rigorous, independent, in-depth public policy research.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

How Europe aims to achieve strategic autonomy for semiconductors

August 9, 2022