Any big change in Federal Reserve monetary policy creates winners and losers in the U.S. economy. But who wins most and who loses most? In “Distributional Effects of Monetary Policy,” Matthias Doepke and Veronika Selezneva of Northwestern University and Martin Schneider of Stanford University offer one answer to that question.

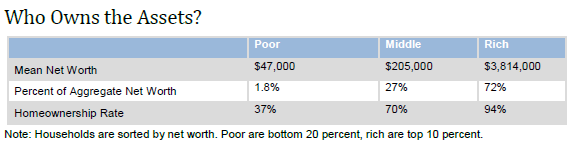

Their bottom line: When the Fed aims for higher inflation, middle-aged, middle-class households, who tend to have big mortgages, benefit at the expense of wealthy retirees, who have a lot of their savings in bank accounts and bonds. Poor and young households are less affected because they are less likely to own homes and their debt burdens are low. In this model, monetary policy not only creates winners and losers but this redistribution also has effects on the real economy: Aggregate consumption declines because winners are likely to spend a smaller fraction of their incomes than losers.

In the authors’ analysis, the redistributive effects of monetary policy operate mainly through the traditional channel: borrowers benefit from higher inflation, while lenders lose. But the authors also consider what happens if housing prices adjust to changes in demand. In their model, changes in inflation do not affect home prices in a uniform way. Prices for homes typically bought by first-time buyers rise little when inflation rises. But houses in demand by middle-aged homeowners, who are using their gains to try to upgrade, rise significantly. These changes in house prices—which hurt middle-age, middle class households and benefit elderly rich households—partially offset the direct redistributive effects of higher general inflation.

The authors evaluate the wealth changes arising from two scenarios. Both imagine an increase in inflation, one unanticipated and the other anticipated because the Fed announces an increase in its inflation target. The identity of the winners and losers is roughly the same in both of these scenarios, although losses incurred by the old rich are reduced considerably if the future course of inflation is anticipated. Thus, the authors find that, contrary to much of the recent rhetoric, looser monetary policy helps the middle-class and middle-aged at the expense of the wealthy aged. Given the magnitude of the gains for some and losses for others, big changes in monetary policy are likely to be politically contentious, the authors conclude.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).