“Don’t tell me what you value. Show me your budget, and I’ll tell you what you value.”

– Joe Biden

Even modest student loan forgiveness proposals are staggeringly expensive and use federal spending that could advance other goals. The sums involved in loan-forgiveness proposals under discussion would exceed cumulative spending on many of the nation’s major antipoverty programs over the last several decades.

There are better ways to spend that money that would better achieve progressive goals. Increasing spending on more targeted policies would benefit families that are poorer, more disadvantaged, and more likely to be Black and Hispanic, compared to those who stand to benefit from broad student loan forgiveness. Indeed, shoring up spending on other safety net programs would be a far more effective way to help low-income people and people of color.

Student loan relief could be designed to aid those in greater need, advance economic opportunity, and reduce social inequities, but only if it is targeted to borrowers based on family income and post-college earnings. Those who borrowed to get college degrees that are paying off in good jobs with high incomes do not need and should not benefit from loan-forgiveness initiatives that are sold as a way to help truly struggling borrowers.

Putting loan forgiveness in fiscal perspective

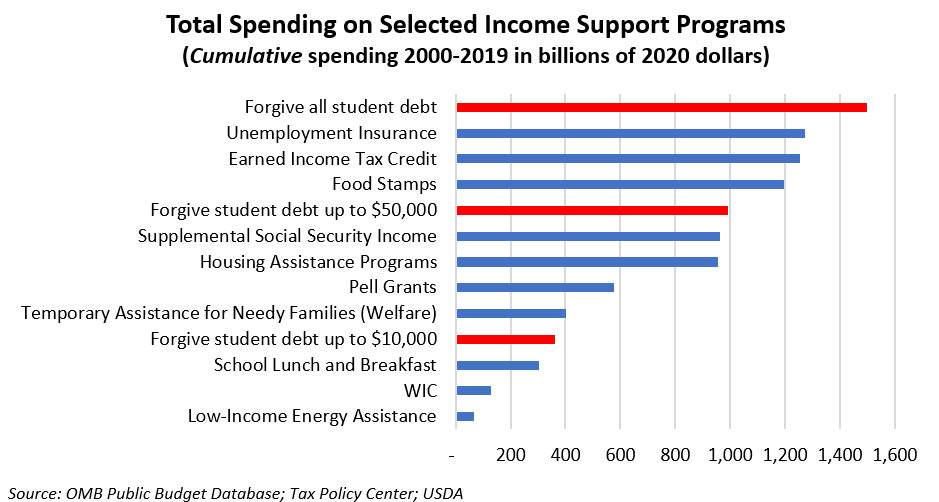

In terms of its scale in budget and cost to taxpayers, widespread student loan forgiveness would rank among the largest transfer programs in American history. Based on data from the Department of Education, forgiving all federal loans (as Senator Bernie Sanders proposed) would cost on the order of $1.6 trillion.[1] Forgiving student debt up to $50,000 per borrower (as Senators Elizabeth Warren and Chuck Schumer have proposed) would cost about $1 trillion. Limiting loan forgiveness to $10,000, as President Biden has proposed, would cost about $373 billion. Under each of these proposals, all 43 million borrowers would stand to benefit to differing degrees.

To put those numbers in perspective, the chart below compares the cost of these three one-time student loan forgiveness proposals against cumulative spending on several of the country’s largest transfer programs over the last twenty years (from 2000 to 2019, adjusted for inflation).

Click on chart to enlarge.

Forgiving all student debt would be a transfer larger than the amounts the nation has spent over the past 20 years on unemployment insurance, larger than the amount it has spent on the Earned Income Tax Credit, and larger than the amount it has spent on food stamps. In 2020, about 43 million Americans relied on food stamps to feed their families. To be eligible, a household of three typically must earn less than $28,200 a year. The EITC, the nation’s largest antipoverty program, benefitted about 26 million working families in 2018. That year, the credit lifted almost 11 million Americans out of poverty, including about 6 million children, and reduced poverty for another 18 million individuals.

Forgiving up to $50,000 of student debt is similar in cost to the cumulative amount spent on Supplemental Security Income (SSI) and all housing assistance programs since 2000. Supplemental Security Income provides cash assistance to 8 million people who are disabled or elderly and have little income and few assets. Recipients must have less than $2,000 in assets. About half have zero other income.

The cost of forgiving $50,000 of student debt per borrower is almost twice as large as the federal government has spent on all Pell Grant recipients over the last two decades. In contrast to federal loans, which have no income eligibility limits and are available to undergraduates, graduate students, and parents, Pell Grants are awarded only to low- and middle-income undergraduate students with demonstrated financial need. About seven million students each year benefit, many of whom are poor and the majority of whom are non-white.

Even $10,000 in debt forgiveness would involve a transfer that is about as large as the country has spent on welfare (TANF) since 2000 and exceeds the amount spent since then on feeding hungry school children in high-poverty schools through the school breakfast and lunch program. Likewise, it dwarfs spending on programs that help feed low-income pregnant women and infants or provide energy assistance to those who otherwise struggle to heat their homes in winter.

Who benefits from comparable transfer programs?

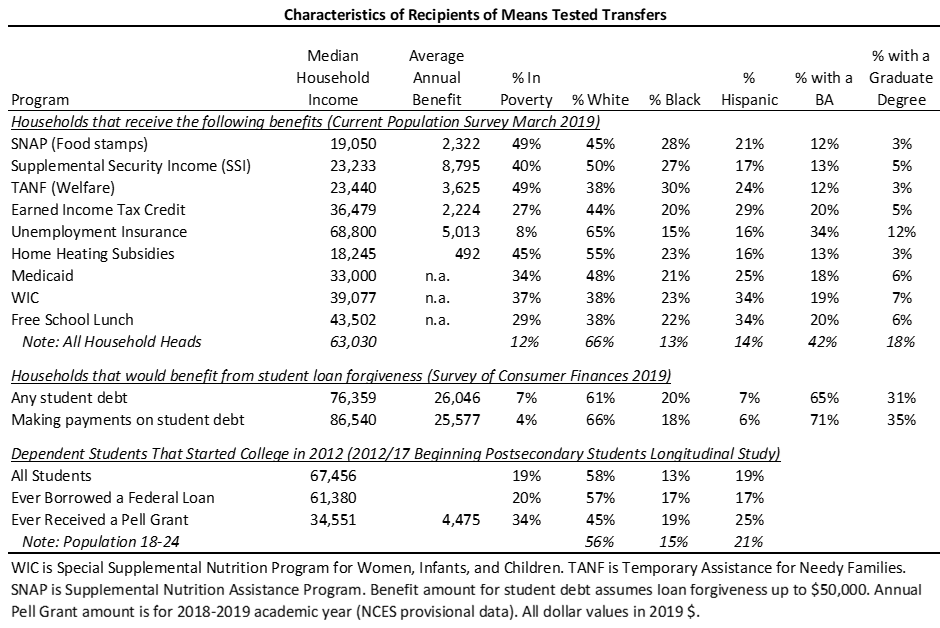

Beyond the sums that debt forgiveness would represent, the beneficiaries of student loan forgiveness would be higher income, better educated, and whiter than beneficiaries of other transfer programs. The following table describes the economic and demographic characteristics of beneficiaries of selected income support programs as well as would-be beneficiaries of student debt forgiveness.

Food stamps, for instance, serve households whose median income is about $19,000 a year (half are in poverty), and provide $2,300 annually for the average household. Medicaid households earn about $33,000; about 34 percent are below the poverty line. Families that claim the Earned Income Tax Credit—the largest cash income support for working families—earn about $36,500; their average annual benefit is about $2,200.

Click on table to enlarge.

In contrast, the median income of households with student loans is $76,400, and 7 percent are below the poverty line. Among those making payment on their loans (and who would have an immediate cash flow benefit from forgiveness), the median income is $86,500, and 4 percent are in poverty. If debt forgiveness were capped at $50,000, the average benefit to these households would be roughly $26,000—about the same as we provide a family living on food stamps over the course of 11 years.

In terms of demographics and educational attainment, households with student debt largely mirror the characteristics of households in the population at large, except they are better educated. Student loan borrowers are more likely to be white and highly educated. Indeed, among those making payments on student loans the fraction of households that are white is the same as in the population at large, but they are about 70 percent more likely to have a BA and twice as likely to have a graduate degree.

In contrast, households that benefit from federal programs, like SNAP, the EITC, SSI, or Medicaid, are more likely to be Black or Hispanic, and have much lower levels of educational attainment; few have gone to college, and almost none have a graduate degree.

For reference, among all households, the Census reports that 66 percent identify as white, 13 percent Black or African American, and 14 percent as Hispanic. About 42 percent have a BA and 18 percent a graduate degree.

In short, beneficiaries of across-the-board student loan forgiveness would be higher income, better educated, and more likely to be white than beneficiaries of just about all other programs designed to reduce hardship and promote opportunity and targeted to those who need help.

Prioritizing spending on targeted programs would therefore be a more effective way to achieve progressive goals. Biden’s proposal to make the child tax credit fully refundable, for example, would exclusively benefit children living in poverty. Twenty six percent of beneficiaries of that policy would be Black and 29 percent Hispanic. That is a progressive change that would lift the incomes of millions of very poor children. It would also benefit many student loan borrowers—as well as many who don’t have student loans.

Targeting student loan relief

Student loan relief could be targeted to those who need help most.

Use borrower’s financial aid application: Every student with a federal student loan has already filled out an application for financial aid (and that application remains on record at the Department of Education). That information could be used to target aid based on students’ economic circumstances at the time of application. For example, the Pell Grant is available only to undergraduate students from low- and middle-income families. As a result, relative to other postsecondary students, Pell Grant recipients are from poorer families and are more likely to be Black and Hispanic students.

Biden has proposed to double the Pell Grant prospectively. If future students got additional grant money, you could argue that prior students should have had that opportunity too—and we could reduce borrowers’ undergraduate loan balances by the amount they should have gotten in Pell (plus interest). That would be more progressive and concentrate the benefit of debt forgiveness on students from disadvantaged backgrounds.

Income-driven repayment: Income-driven repayment plans (like Pay As You Earn, or PAYE) remain an excellent way to target debt relief and forgiveness to students whose post-enrollment incomes are too low to be able to make student debt payments. The Biden Administration has new tools enacted in the FUTURE Act that, if implemented, would make it easier for students to sign up and remain in income-driven plans.

Getting income-driven plans to work effectively is necessary because student lending isn’t going away. Even the most ambitious “free college” proposals would only modestly reduce the volume of new student debt because they only cover tuition and fees at public institutions. Graduate students, students at private colleges, and students who borrow to cover living expenses would still be reliant on loans to finance their education. Those costs represent the majority of loan dollars students borrow each year. Income-driven repayment will be necessary to help these future borrowers manage their loans.

Between targeted debt relief to students from low-income families, improvements in income-driven plans, and implementing forgiveness plans (like public service loan forgiveness) already on the books, Congress and the Biden Administration can reduce hardships imposed by federal lending and advance economic opportunity—without across-the-board loan forgiveness. Congress and the Administration can’t do it all. We need to weigh student-loan forgiveness against other spending priorities and be clear about what we value most.

[1] Administrative data from the Department of Education shows that borrowers owe a total of $1.57 trillion—the sum of balances under $50,000 is $1.05 trillion, and the sum of balances under $10,000 is $377 billion. CBO estimates the subsidy rate on student loans (the amount that would not be repaid in present value) is 3% on newly-originated loans in 2021. As a result, I assume the cost is 97% of the value reported by the Department of Education. For purposes of understanding the magnitude of the transfer, the face value is also relevant because it reflects the total amount of aid provided to students. These estimates are larger than estimates based on data from the Survey of Consumer Finances (SCF), because about a third of student debt is not reported in that survey.

Related Content

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Putting student loan forgiveness in perspective: How costly is it and who benefits?

February 12, 2021