Studies in this week’s Hutchins Roundup find that large-scale asset purchases increased bank risk taking, credit supply shocks boost household demand, and more.

Want to receive the Hutchins Roundup as an email? Sign up here to get it in your inbox every Thursday.

Large-scale asset purchases led to relaxed lending standards and increased loan risk

Following the 2007-2008 financial crisis, the Fed made heavy use of large-scale asset purchases, including purchases of mortgage-backed securities (MBS). Using confidential survey data on banks’ lending standards and loan risk ratings, Robert Kurtzman, Stephan Luck, and Tom Zimmermann from the Federal Reserve Board find that, following the Fed’s MBS purchases, banks with a larger share of holdings in MBS were more likely to lower lending standards and increase loan risk than other banks. They estimate that Fed MBS purchases had about the same effect on bank risk- taking as a one-percentage point decrease in the federal funds rate. Thus, unconventional monetary policy works not only by increasing credit availability, but also by encouraging riskier lending, they conclude.

Increased credit availability boosts household demand, not labor productivity

Atif Mian and Emil Verner from Princeton and Amir Sufi from the University of Chicago examine the channels through which credit supply shocks affect the real economy. They explain that a credit supply shock that boosts local demand leads to a larger increase in employment in industries producing non-tradeable goods as opposed to tradable goods, whereas a credit supply shock that increases productivity increases both tradeable and non-tradeable employment. Using the variation in the degree of bank deregulation across states in the 1980s as a measure of credit supply shocks, they find that the main effect of increased credit availability is an increase in household demand: States that underwent more deregulation experienced larger relative increases in household debt and non-tradable employment, and had similar changes in tradable employment as states that deregulated less.

US corporate tax structure partially explains increased cash holdings

Cash holdings by corporations tripled between 1994 and 2014. Michael Faulkender from the University of Maryland and co-authors argue that much of this increase can be explained by the US corporate tax system, which encourages multinational companies to keep cash abroad. Using private data from the Bureau of Economic Analysis, they show that between 1998 and 2008, domestic cash increased by around 55 percent while foreign cash rose by 410 percent. They find that the variables used in existing literature to measure the need for precautionary savings predict firms’ domestic cash levels, but not their foreign holdings. Instead, differences between foreign and domestic tax rates explain foreign cash holdings. Multinationals that invest heavily in research and development are the primary drivers of the foreign cash trend, they say, because these firms can most easily transfer income from high-tax to low-tax jurisdictions.

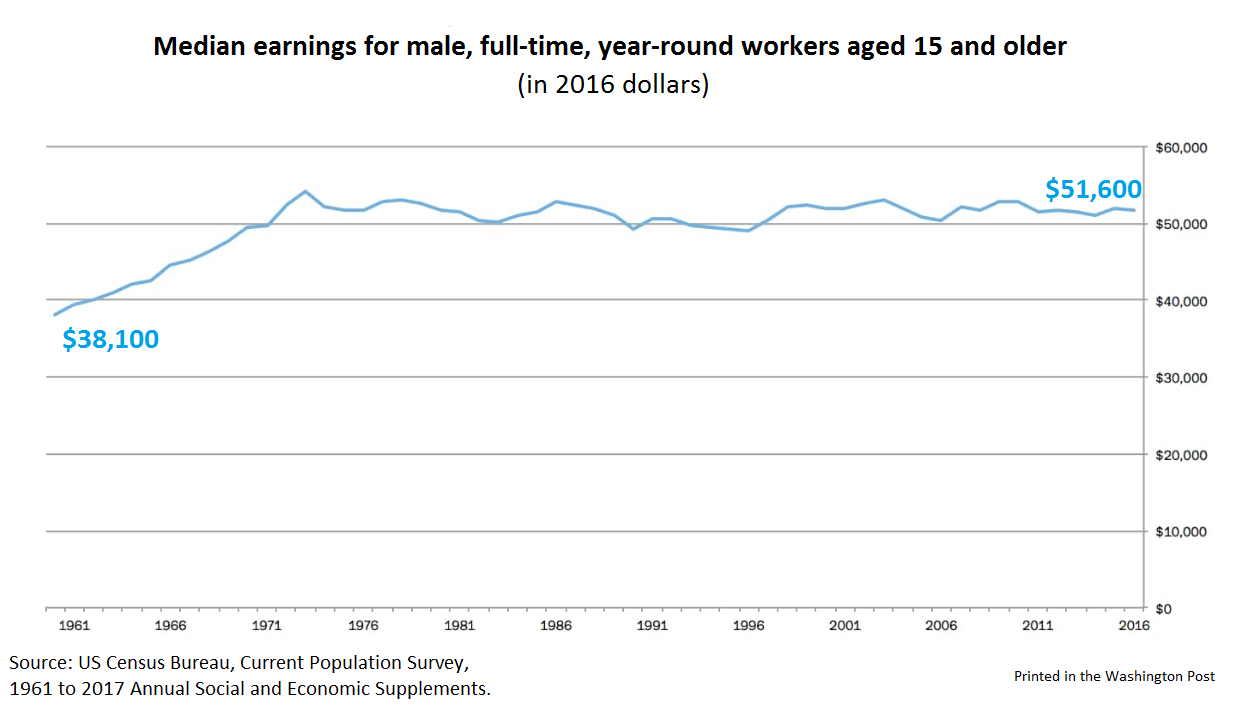

Chart of the week: Median earnings for full-time males have been stagnant since 1972

Quote of the week:

“[E]ven though inflation is currently somewhat below our longer-run objective, I judge that it is still appropriate to continue to remove monetary policy accommodation gradually. This judgment is supported by the fact that financial conditions have eased, rather than tightened, even as the Fed has raised its short-term interest rate target range by 75 basis points since last December. For example, equity prices have risen, credit spreads have narrowed modestly, longer-term interest rates have declined, and the dollar has weakened…,” says New York Fed President William Dudley.

“[Financial conditions] influence the demand for goods and services by households and businesses… All else equal, an easing of financial conditions may warrant a somewhat steeper policy rate path. Conversely, if financial conditions were to tighten unduly, then this might necessitate a shallower rate path to temper that tightening. To be clear, this does not mean that the Fed should mechanically target a particular set of financial conditions…Financial conditions are just a means to an end-the achievement of the Fed’s employment and inflation objectives.”

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Hutchins Roundup: Large-scale asset purchases and bank risk taking, effects of credit availability, and more

September 14, 2017