Studies in this week’s Hutchins Roundup find that “too-big-to-fail” banks are not valued more highly than small banks, healthy school lunches raise student test scores, and more.

Want to receive the Hutchins Roundup as an email? Sign up here to get it in your inbox every Thursday.

Large banks’ “too-big-to-fail” status does not increase their value

Conventional wisdom suggests that the value of large banks– banks with assets above the Dodd-Frank threshold for enhanced supervision–should increase with asset size because of the implicit subsidies from the regulatory safety net. Bernadette Minton and René Stulz of Ohio State and Alvaro Taboada of Mississippi State point out, however, that large banks may also bear costs arising from increased regulatory and political scrutiny. Using the ratio of market value of assets to book value of assets as a valuation measure, the authors find no evidence that large banks are valued more highly or that their valuation increases with size. Instead, they find that bank value decreases with size.

Schools may be able to raise their students’ test scores by serving healthier meals

With data on all California public schools over 2008-2013, Michael Anderson and Elizabeth Ramirez Ritchie of the University of California, Berkeley, and Justin Gallagher of Case Western Reserve conclude that students at schools that contract with vendors serving relatively nutritional lunches score higher on state achievement tests than students at schools with in-house meal provision. The effect is larger for students who are eligible for reduced price or free school lunches. The authors find no evidence that healthier school lunches affect obesity rates.

Credit supply frictions were an important contributor to employment declines during the Great Depression

Using a novel dataset on large industrial firms during the Great Depression, Efraim Benmelech, Carola Frydman, and Dimitris Papanikolaou of Northwestern show that firms that needed to refinance maturing bonds during the crisis cut employment more than other similar businesses, especially if their local banks were in distress. In particular, constrained access to credit explains about 10 to 33 percent of the aggregate decline in employment of large firms between 1928 and 1933, they estimate.

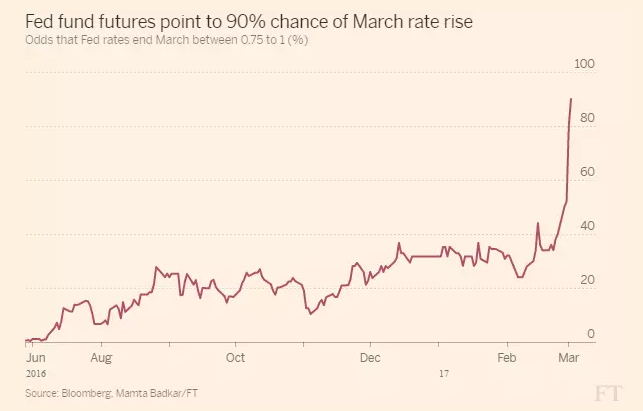

Chart of the week: Markets now almost unanimously anticipate a rate hike in March

Quote of the week: “Contrary to the popular misconception, we’re not ‘the feds’,” says San Francisco Fed President John Williams.

“We’re not politicians or fiscal policymakers. We don’t spend money or set taxes. We don’t write legislation. And unlike politicians, we’re not elected. In conducting monetary policy, we base our decisions on what’s best for the long-term health of the economy, without political influence from Congress, the Administration, or others. To my mind, this is the single most important feature of the Fed: the ability to act independently of short-term political influence… which allows us to respond to changing circumstances as needed. Across the world, independent central banks have proven to be more effective at stabilizing inflation and keeping their countries’ economies performing up to their full potential than countries where the central bank is under political control.”

Related Content

Related Books

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Hutchins Roundup: Large banks, school lunches, and more

Thursday, March 9, 2017