Studies in this week’s Hutchins Roundup find that declines in oil prices during 2014-2016 contributed to U.S. stock market volatility and hurt its energy sector, increasing industry concentration may be behind the fall in U.S. labor’s share, and more.

Want to receive the Hutchins Roundup as an email? Sign up here to get it in your inbox every Thursday.

Declines in oil prices might be bad for oil-importing economies too

Contrary to the conventional wisdom that oil price declines have positive or neutral effects on the importing country’s stock market, Ha Nguyen of the Word Bank, Huong Nguyen of Tufts, and Anh Pham of George Mason conclude that a fall in oil prices adversely affected the U.S. stock market during 2014-2016. In particular, they show that oil price declines increased uncertainty and hurt risky assets such as stocks while boosting the price of safe assets such as long-term Treasury bonds. Surprisingly, the fall in oil prices hurt equity values in oil-dependent sectors such as basic materials, transport and industrials, perhaps because the increased uncertainty lowered demand for their products.

Growing industry concentration might explain a fall in labor’s share

The share of Gross Domestic Product going to labor, as opposed to capital, has been declining for the past several decades. David Autor of MIT and his co-authors suggest that this may reflect growing market concentration within industries because labor’s share, as a fraction of total sales or value added, is likely to be lower in larger firms. In particular, they show that the concentration of sales among firms within industries has risen and industries with larger increases in concentration exhibit a larger decline in labor’s share.

Current statistical methods tend to underestimate growth from creative destruction

When a product is replaced by an improved product, statistical agencies generally average the change in prices among surviving products, adjusted for quality. This procedure is accurate only if the pace of quality change associated with this creative destruction matches that of surviving products. Philippe Aghion of College de France and his co-authors find that ignoring the possibility that the new products may be substantially better in quality than disappearing products may overstate inflation and understate growth of private non-farm U.S. business by 0.5 to 1 percentage point per year during 1983–2013.

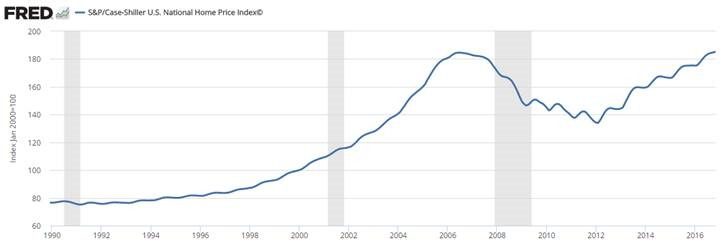

Chart of the week: Housing prices have returned to pre-crisis levels

Quote of the week: “At a minimum, the next generation of models must capture the links between the financial system and the real economy,” says Governor of the Bank of Canada Stephen Poloz.

“They should explain how the financial system can be a source of shocks and how those shocks can be propagated. They need to capture the possibility of nonlinearities that cause small shocks to have outsized economic effects. They should be able to show how debt that builds up in a specific sector can affect the entire economy. And we need models that capture risks and vulnerabilities within the financial system and can show how these interact with monetary and macro-prudential policies.”

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Hutchins Roundup: Oil prices, labor’s share, and more

Thursday, February 2, 2017