The election of Donald Trump demands a reevaluation of the future of globalization and our earlier optimism that the open global economic order will endure. It is time to consider the possibility that a single politician could reverse decades of global trends.

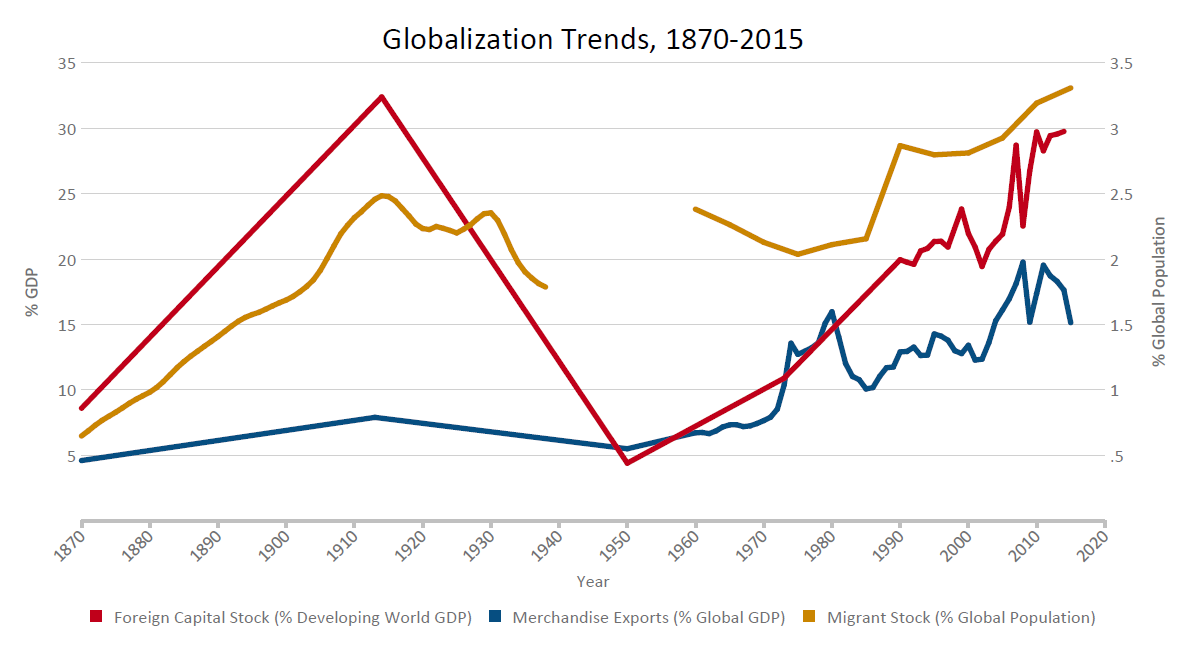

We published a short paper a month ago assessing the claim that globalization was on the verge of a retreat. Our conclusion was relatively sanguine. Based on an assessment of the movement of goods, money, and people across international borders, we found little evidence that globalization is already receding—see Figure 1. We also showed that the global economy is more integrated today than during the peak of the early 20th century, which we interpreted as a repudiation of the claim that globalization had reached unsustainable levels; we are skeptical that such levels exist in a literal sense. Looking to the future, we speculated that the years immediately ahead will be characterized either by stabilization in the level of globalization, or further integration but occurring at a more modest pace than in the past.

Figure 1: Globalization trends, 1870-2015

Authors’ calculations based on IMF 2015, Lane and Milesi-Ferretti 2013, Maddison 2001, the Maddison Project 2015, McKeown 2004, McKeown 2010, Riley 2009, U.N. 1999, U.N. 2015a, U.N. 2015b, UNCTAD 2015, U.S. Census Bureau 1975, World Bank 2015, World Bank 2016, and WTO 2016. Merchandise exports and foreign capital stock are expressed in market dollars as a share of global income expressed in international dollars, and will therefore differ with those cited elsewhere. Full description of sources and methodology are available in this report.

How, if at all, does the election of Donald Trump alter our views?

It is worth emphasizing that a resistance to globalization was arguably the foremost policy theme in Trump’s election campaign. In the speech announcing his presidential bid, Trump railed against the United States’ existing trade agreements, threatened to slap taxes on U.S. companies investing overseas, and pledged to build a wall to keep out migrants, whom he accused of being rapists. Trump’s plan for his first 100 days in office reaffirms the centrality of this theme, with a commitment to renegotiate or withdraw from NAFTA, abandon support for the Trans-Pacific Partnership (TPP), label China a currency manipulator, establish tariffs to discourage companies from off-shoring production and jobs, expel more than two million migrants, suspend immigration from terror-prone regions, and build the wall.

Let’s assume President-elect Trump succeeds in implementing this agenda. We see its effects on globalization playing out at three levels.

The first is the direct effect of the U.S. turning inward. The U.S. is the world’s largest economy, measured in market dollars, and its third most populated. A partial withdrawal from the global economy by the U.S. is therefore likely to register in measures of globalized stocks and flows, simply by virtue of the country’s size.

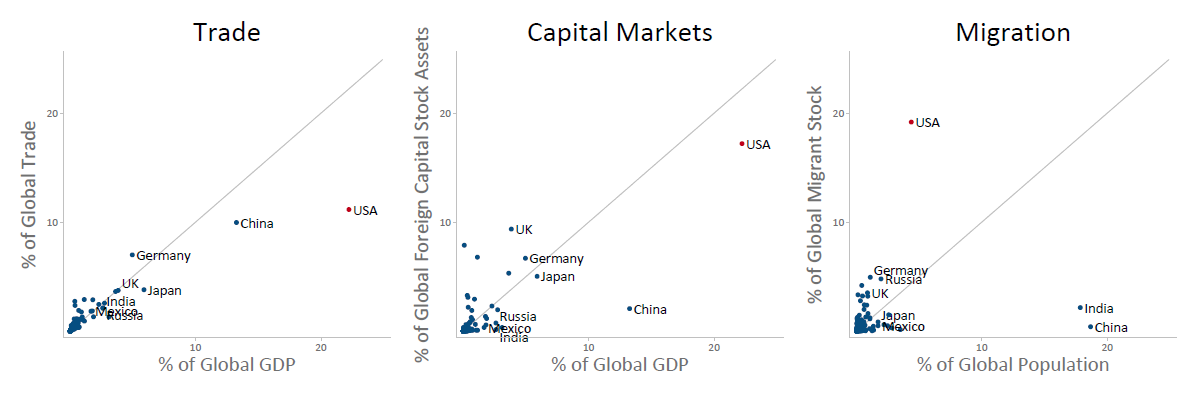

Indeed, America holds the largest share of global trade, foreign capital stocks, and migrants. Yet, relative to its size, America is not as globally integrated as many other countries. It is those areas where the U.S. is most globally intertwined, as measured by the vertical axes of Figure 2, that the direct impact of a Trump presidency on globalization could theoretically be greatest.

Figure 2: Global shares of trade, capital markets, and migration

Authors’ calculations based on Lane and Milesi-Ferretti 2014, U.N. 2015a, and World Bank 2016. Capital stock assets include estimates of external debt, foreign direct investment (FDI), and portfolio equity stocks. Full description of sources and methodology are available in this report.

For instance, despite the prominence of trade during the election campaign, the U.S. is a relatively closed economy. It accounts for only 11 percent of global trade volumes—far below its 24 percent share of global GDP. That said, this likely understates the country’s footprint in global trade given that the U.S. imports many final goods whose production occurs along international supply chains. By contrast, the U.S. plays a fuller role in global capital markets. Within those markets, the area that may be most directly vulnerable to Trump’s policies is outward foreign direct investment (FDI). The U.S. lays claim to 18 percent of global FDI assets. However, the U.S. is most globalized, relative to other countries, in terms of its openness towards migrants. The country is home to 19 percent of the world’s migrant stock, while accounting for only 4 percent of the world’s population. In fact, the U.S. is the top destination for migrants from 60 countries. The expulsion of large numbers of migrants and greater restrictions on the number of future entrants would directly alter this aspect of the global economy.

While the direct effects of the U.S. turning inward on global economic integration are important, they are still likely to be relatively small in terms of the three series presented in Figure 1. Much larger effects are possible in terms of the impact Trump’s policies could have by changing the behavior of other countries. This is the second level at which we see Trump’s effect on globalization unfolding.

We may see countries retaliate against U.S. protectionist policies. This is the basis for concerns that Trump could precipitate a trade war.

We may see countries retaliate against U.S. protectionist policies. This is the basis for concerns that Trump could precipitate a trade war. The threat has already been made explicit by the state-sponsored Chinese tabloid, Global Times, which proposed that China respond to aggressive trade policies by cancelling contracts with U.S. suppliers, imposing tariffs on U.S. imports, and limiting the number of Chinese students studying in American universities, and by French presidential candidate Nicolas Sarkozy who has suggested that the Europe Union impose a tax on U.S. products and limit the participation of foreign companies in EU public contracts if Trump withdraws from the Paris climate accord.

Countries and their leaders may instead imitate Trump’s policy agenda, whether in pursuit of similar electoral success or on the basis that his election gives his anti-globalization agenda legitimacy. In the past week, politicians from Italy, Hungary, Greece, and elsewhere have invoked Trump’s victory as justification for policies that reverse the pattern of globalization.

Alternatively, countries may repudiate global norms and institutions that underpin the globalized economy, if they feel that the U.S. is no longer committed to upholding the liberal economic order. This reflects the widely held belief that the stability of the existing economic order hinges on the example set by the U.S., as the longstanding global economic hegemon. Such an outcome foreshadows chaos, but with the era of U.S. global economic pre-eminence coming to a close, those norms and institutions, from World Trade Organization membership and rules, to the various U.N. conventions concerning the treatment of migrants and refugees, were always likely to be tested soon. Trump’s election may usher a more rushed transition as emerging markets that have benefited most from the open global economy come to its defense. There is already some evidence of this kind of realignment, as members of the TPP seek to patch together the deal without the U.S., and China makes the case for its alternative regional trade deals.

The third and final way in which we interpret the effect of Trump’s election on the future of globalization is the injection of a huge amount of uncertainty.

The breaking of globalization’s first wave a century ago is proof that the forces of global economic integration are neither irresistible nor irreversible.

The breaking of globalization’s first wave a century ago is proof that the forces of global economic integration are neither irresistible nor irreversible. Trump’s ascent to the White House adds to the evidence, representing the biggest shift in the U.S.’s orientation vis-à-vis the global economic system in the post-war period. This policy discontinuity is a source of uncertainty in and of itself. We have assumed that Trump will deliver on his anti-globalization agenda, yet for now it remains unclear whether he will pursue it in full and what constraints to its implementation will arise. Perhaps the most important risk concerns how he will respond to unanticipated events over the period of his presidency, through the prism of his anti-globalist perspective. This uncertainty alters the way we view the direct and indirect effects of Trump’s policies described earlier by reducing our confidence in them and expanding the range of possible outcomes.

Taking these considerations together, our view on globalization’s future has indeed changed. We are much less assured that the open global economic order will endure.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Donald Trump and the future of globalization

November 18, 2016