Studies in this week’s Hutchins Roundup find that teenagers who lived in public housing had higher earnings in adulthood and were less likely to be incarcerated, poor health may account for some of the decline in labor force participation of prime age men, and more.

Teenagers whose families receive housing assistance have higher earnings in adulthood

Fredrik Andersson of the Office of the Comptroller of the Currency and co-authors investigate the long-term effects of childhood participation in voucher-assisted and public housing. To control for the family characteristics associated with receipt of housing assistance, they contrast the adult outcomes of those who lived in voucher-supported or public housing when they were teenagers with the outcomes of their siblings who didn’t have such access. They find that siblings who received housing assistance had higher earnings at the age of 26 and were less likely to be incarcerated. The beneficial effects of housing assistance receipt were particularly strong for females from non-Hispanic black households.

Poor health may be contributing to the decline in labor force participation among prime age men

Alan Krueger of Princeton finds that about half of the prime age men, that is, men between the ages of 25 and 54, who are neither working nor looking for work, say they have a serious health condition that is a barrier to full time employment. He also finds that about half of the men not in the labor force take pain medication on a daily basis, and in about two-thirds of cases, they take prescription pain medication. Raising labor force participation will require a reversal of this and other trends and, perhaps, immigration reform, he concludes.

Demography accounts for much of the decline in the natural rate of interest

Demographic change – particularly the post-war Baby Boom, declining fertility rates and lengthening life expectancy – contributed substantially to the recent decline in the natural rate of interest and GDP growth rates, Etienne Gagnon, Benjamin Johannsen and David Lopez-Salido of the Federal Reserve Board find. Using an overlapping-generations model with a rich demographic structure, they show that demographic factors can account for a 1.25 percentage-point decline in the equilibrium real interest rate and real GDP growth since 1980. Had these demographic forces not been triggered, the US would be experiencing interest rates and GDP growth similar to their levels in 1980, they find. They conclude that real GDP growth and real interest rates will remain low in coming decades.

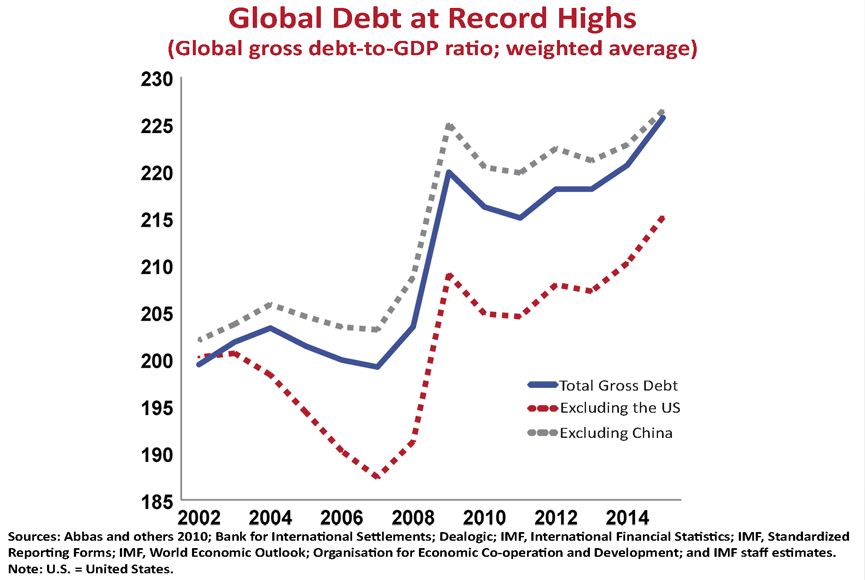

Chart of the week: High public and private debt levels may exacerbate risk of debt-deflation spiral

Quote of the week: “Given that generally positive view of the economic outlook, one might ask, why did we not raise the federal funds rate at our September meeting?” SAYS Fed Vice Chairman Stanley Fischer

“Our decision was a close call, and leaving the target range for the federal funds rate unchanged did not reflect a lack of confidence in the economy. Conditions in the labor market are strengthening, and we expect that to continue. And while inflation remains low, we expect it to rise to our 2 percent objective over time. But with labor market slack being taken up at a somewhat slower pace than in previous years, scope for some further improvement in the labor market remaining, and inflation continuing to run below our 2 percent target, we chose to wait for further evidence of continued progress toward our objectives. As we noted in our statement, we continue to expect that the evolution of the economy will warrant some gradual increases in the federal funds rate over time to achieve and maintain our objectives. That assessment is based on our view that the neutral nominal federal funds rate–that is, the interest rate that is neither expansionary nor contractionary and keeps the economy operating on an even keel–is currently low by historical standards. With the federal funds rate modestly below the neutral rate, the current stance of monetary policy should be viewed as modestly accommodative, which is appropriate to foster further progress toward our objectives.”

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Hutchins Roundup: Housing assistance, labor force participation, and more

Thursday, October 13, 2016