In recent years, the world has encountered a range of compounding shocks: droughts, floods, wildfires, cyclones, and most recently, a worldwide pandemic that has taken over 3.3 million lives—some estimates even indicate up to 13 million deaths. Although the pandemic will (eventually) pass, the next global challenge is already upon us. Climatic shocks are expected to increase in frequency and severity.

Agriculture—still the most important sector in many poor countries—is directly affected by climatic shocks. Besides threatening global food security and stability, these shocks can cripple livelihoods, disrupt value chains, and even undermine macroeconomic stability. Climatic shocks have caused significant budget volatility in recent years and deepened corruption challenges. Agriculture insurance can be an antidote to these risks: It de-risks lending to the farm sector enabling repayment of loans, reduces budget volatility of agriculture-related fiscal expenditures by transferring climatic risk to the private sector, increases fiscal space during shock years, and stimulates growth of the agriculture sector, which can unlock job creation potential. It can even reduce the scope for fiscal leakages and corruption.

The case for public policy

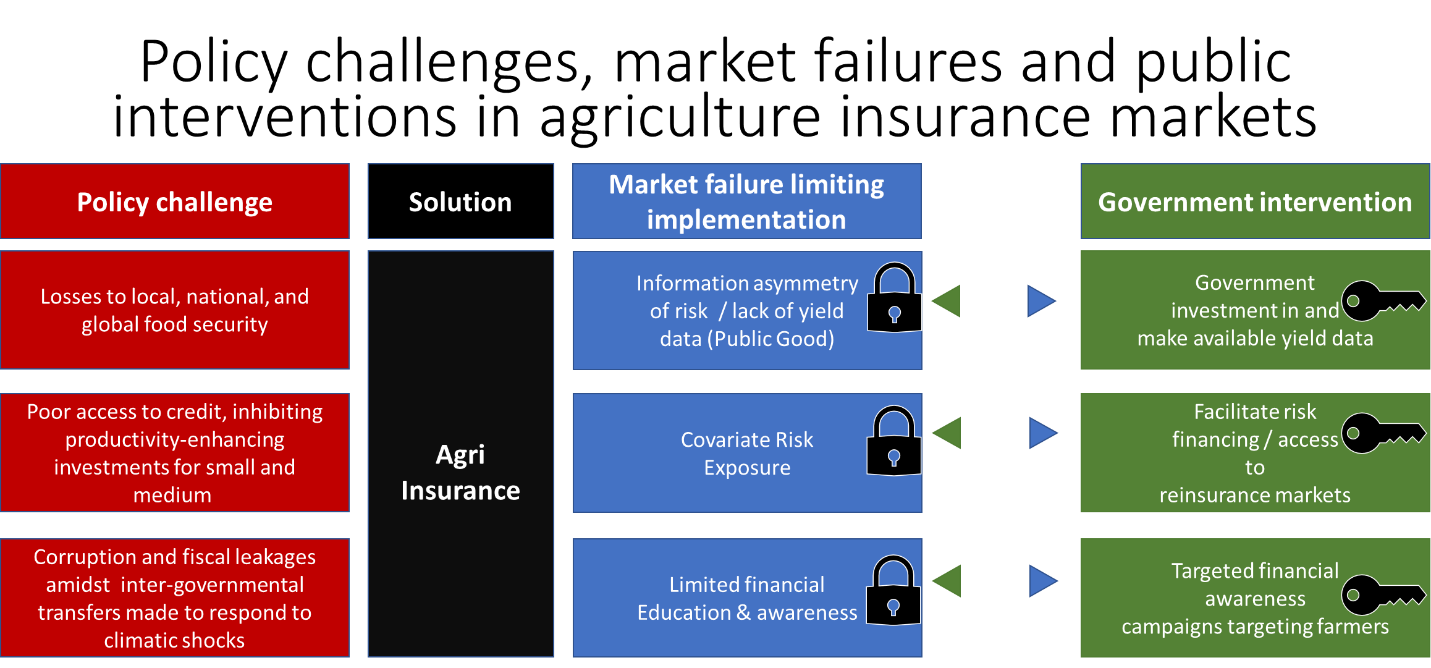

But agriculture insurance suffers from market failures and information asymmetries that require government intervention to achieve scale and sustainability (see “Government Support to Agricultural Insurance” by Olivier Mahul and Charles Stutley). Information asymmetries arise as farmers understand their risk profile better than insurance companies, introducing scope for anti-selection and moral hazard. Insurance companies need high quality yield data to vet and underwrite products. Being both non-rivalrous and excludable, yield data are a public good, necessitating government intervention to avoid monopolization. Besides, while insurance companies are in the business of managing risk, they often have limited appetite for agricultural risk given its exposure to catastrophic losses from single events. This leads to rationing of exposure or even refusal to underwrite agricultural risks by insurance companies. Finally, farmers often have low levels of financial awareness requiring public support for financial education programs.

Figure 1. A straightforward rationale for government intervention

Source: Authors

Success stories

There are many examples where governments, in partnership with the private sector, have used agriculture insurance to manage the financial impacts of climatic shocks and to support growth of the agriculture sector. Here are three—with many more in the book referenced above. First India, where the government wanted to raise productivity in small and medium farms. Since these farmers were unable to access credit due to poor collateral, this stunted investment. In Gujarat state, the government launched a public-private agriculture insurance program called the Comprehensive Crop Insurance Scheme of India where subsidized agriculture insurance served as collateral for credit. This increased the flow of credit to farmers, both in coverage and size, from 19 percent to 27 percent of the credit portfolio. The scheme was the inspiration for a national program, though farmers in India continue to face major obstacles in insuring their crops.

In Kenya, the provision of relief to farmers was a constant fiscal drain. The catastrophic drought in 2008-2011 was estimated to have had an overall impact of $12 billion—about 11 percent of 2011 GDP. As part of the response, the government adopted a National Disaster Risk Financing Strategy, under which an agriculture insurance program implemented in partnership with the private sector targets vulnerable farmers (this World Bank project document provides details). The insurance is bundled with high-quality inputs and sold to farmers as a package. In return for the premium, if the rains fail, the insurance compensates them for losses. If rainfall is good, they get bumper crops. Payouts are delivered via mobile money that increases the speed and transparency of relief support and promotes financial inclusion by providing access to savings. Over half a million farmers are now protected under the program, which strengthens the financial resilience of the farmers and agriculture-related value chains to shocks, while also protecting the government from budget volatility by transferring some of the risk to private markets.

In Kenya and India alike, governments have provided support for the data collection to design the insurance products, as well as premium co-financing to lower the cost to farmers and incentivize insurance companies to extend coverage.

Finally, agriculture insurance can reduce corruption and fiscal leakages. In February 2021, President Ramaphosa of South Africa identified corruption as one of the most serious impediments to South Africa’s development. In the current model, after a “State of Disaster” is declared, payments are made from National Treasury to provinces and municipalities and then to farmers, opening several channels of fiscal leakage. With agriculture insurance, insurance companies pay claims directly to the beneficiaries in the event of shocks. Payouts are made into beneficiary bank accounts or their mobile money accounts, reducing both delay and diversion.

A fiscal instrument for the times

With a jaw-dropping $16 trillion of fiscal support provided to countries worldwide and vaccine rollout working its way around the world, public balance sheets are too weak to support the recovery. Budget volatilities resulting from climatic shocks could very well lead to many countries being tipped into debt distress or worse. Agriculture insurance offers a way to reduce volatility, strengthen resilience, and support productivity growth in the agriculture sector—a sector that provides livelihoods to billions, food security to everyone, and stability to entire economies. With compounding shocks, utilizing innovative insurance solutions is more important than ever.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Agricultural insurance: The antidote to many economic illnesses

May 26, 2021