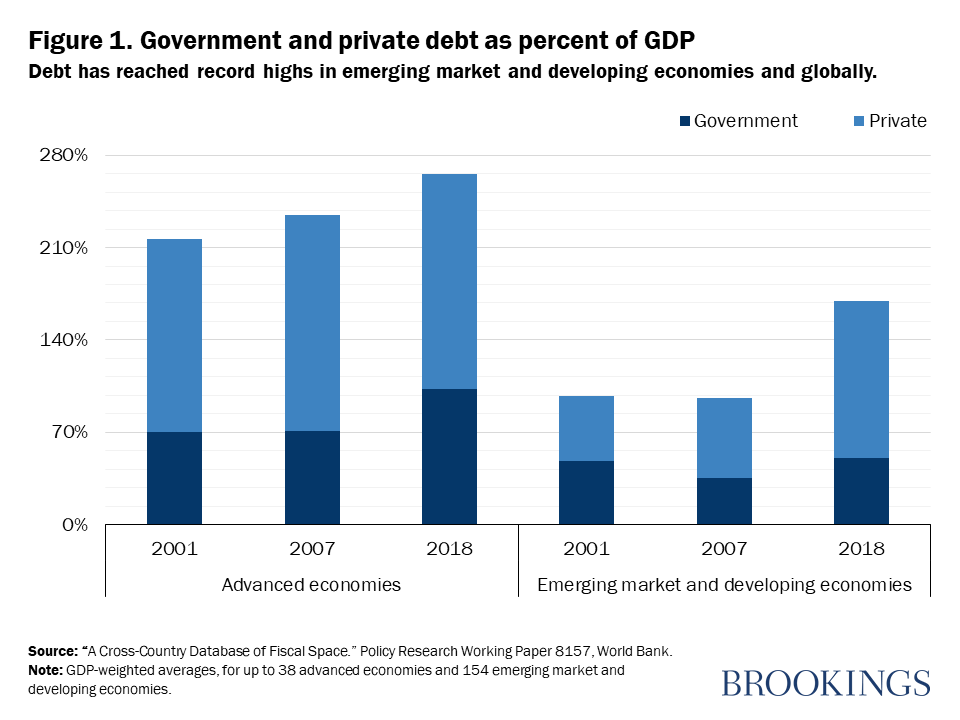

Global debt has reached a level not seen since 1970. The current environment of low interest rates and subpar growth performance has triggered a debate about benefits and costs associated with debt. This debate has mainly focused on advanced economies. However, emerging market and developing economies (EMDEs) also face record-low borrowing costs and many have rapidly accumulated debt since the global financial crisis (Figure 1). Since 2001, their total debt has risen by about 70 percentage points of GDP to a historic peak of almost 170 percent of GDP in 2018.

In accumulating debt, the trade-offs EMDEs face are even starker than those of advanced economies, given their history of debt crises and their pressing spending needs to achieve development goals. In an environment of weak global growth and low interest rates, could cheap debt be just the medicine these economies need to meet their development goals?

Debt as medicine?

There is no question that debt has multiple benefits. Debt accumulation can support investment for growth-enhancing purposes and fund safety nets for vulnerable groups. When growth is weak, it can support activity with fiscal stimulus. It can expand the supply of safe assets when borrowing conditions tighten.

Promoting long-term growth. Today’s investment in physical and human capital can lay the foundation for stronger growth tomorrow, which is the main driver of long-term poverty reduction. The expected slowdown in potential growth in EMDEs—the rate of growth an economy can sustain at full capacity—lends urgency to the need for additional investment. In addition, EMDEs have large investment needs to meet the Sustainable Development Goals.

Stabilizing short-term growth. Temporary debt accumulation helps stabilize short-term macroeconomic fluctuations by funding government spending or tax cuts that support activity. The effectiveness of such government borrowing is measured by the fiscal multipliers—the output effects of additional government spending or tax cuts—that vary with country characteristics and the economy’s cyclical position.

Providing safe assets. Sovereign debt constitutes a safe asset for investors, as an alternative to private debt whose issuers may default. When risk aversion rises, demand for safe assets increases while borrowing conditions for private borrowers tighten. In these circumstances, an accumulation of government debt, with its proceeds redistributed to private household or corporates, can ease financing constraints.

Or debt as poison?

Debt accumulation also comes with a wide range of costs. The simplest guide to judging the case for public borrowing is a comparison of debt servicing cost—the interest due—and the rate of return on the spending financed by borrowing. This calculus can change rapidly, however, when interest rates sharply increase during financial crises. High debt can also limit the feasible size and effectiveness of fiscal stimulus during downturns. Finally, elevated debt levels can constrain long-term growth by crowding out productivity-enhancing private investment.

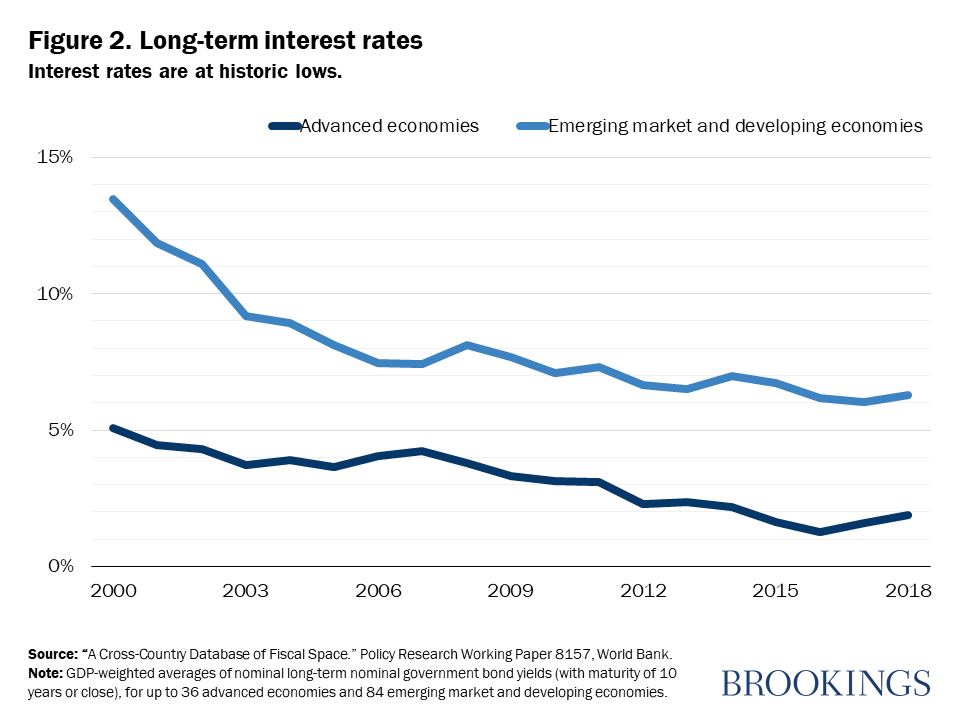

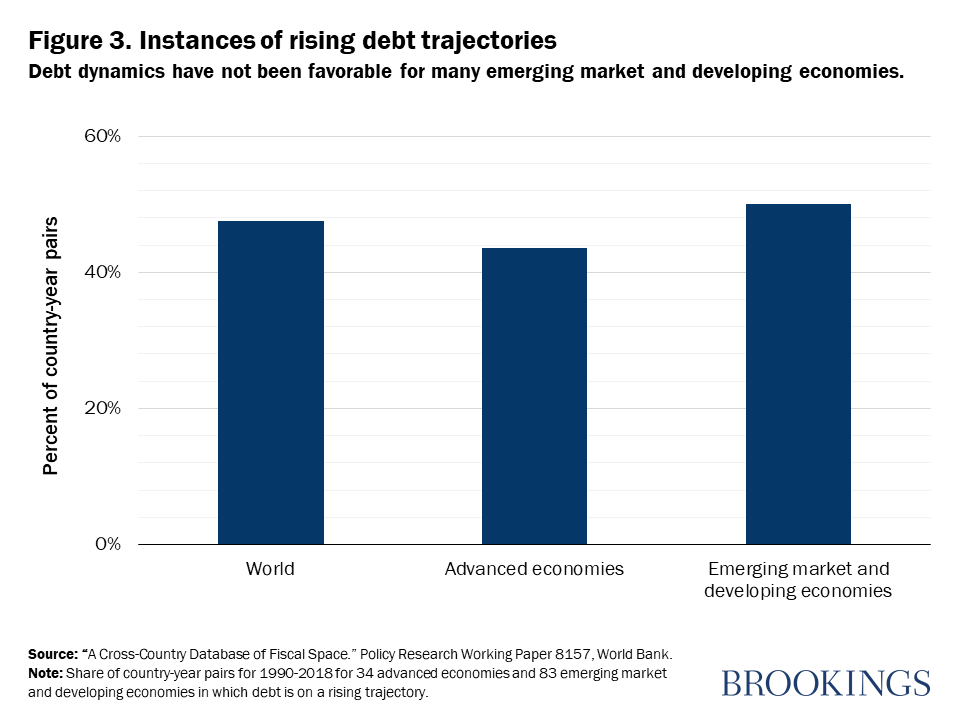

Worsening debt sustainability. Since the global financial crisis, government borrowing costs have been historically low (Figure 2). Demographic shifts and slowing productivity growth are expected to further depress real interest rates. The recent discussion on debt has focused on the differential between interest rates and nominal GDP growth; however, this differential has to be weighed against the accumulation of new debt, or the primary fiscal deficit. In fact, because EMDEs have grown rapidly through most of the past three decades, interest rates have been lower than growth rates in 61 percent of country-year pairs among 83 EMDEs since 1990. Yet, primary deficits have been sufficiently large to put debt-to-GDP on a rising trajectory in 50 percent of the country-year pairs over the same period (Figure 3).

Increasing vulnerability to crises. Mounting debt can erode investor confidence and raise the risk premium on sovereign debt. If investors fear that government debt is no longer sustainable, this could culminate in a debt crisis. It could lead to a currency crisis if concerns about foreign-currency-denominated debt induce a speculative attack on a pegged currency—like, Mexico’s peso crisis in 1994—or a banking crisis if private sector balance sheet vulnerabilities trigger concerns about bank liquidity as, for example, happened in multiple countries during the global financial crisis.

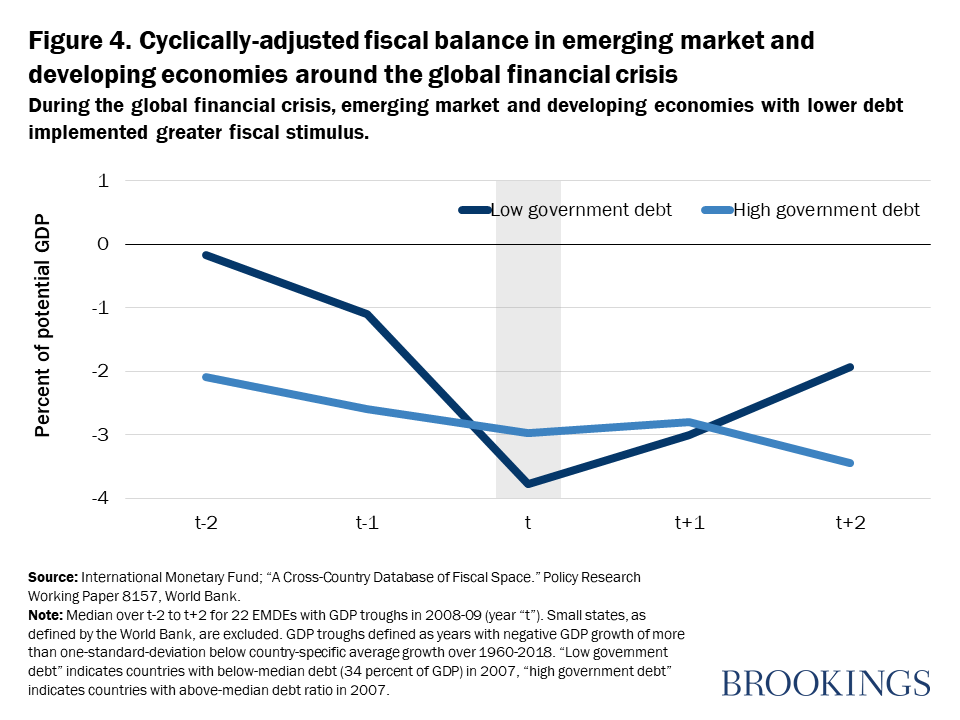

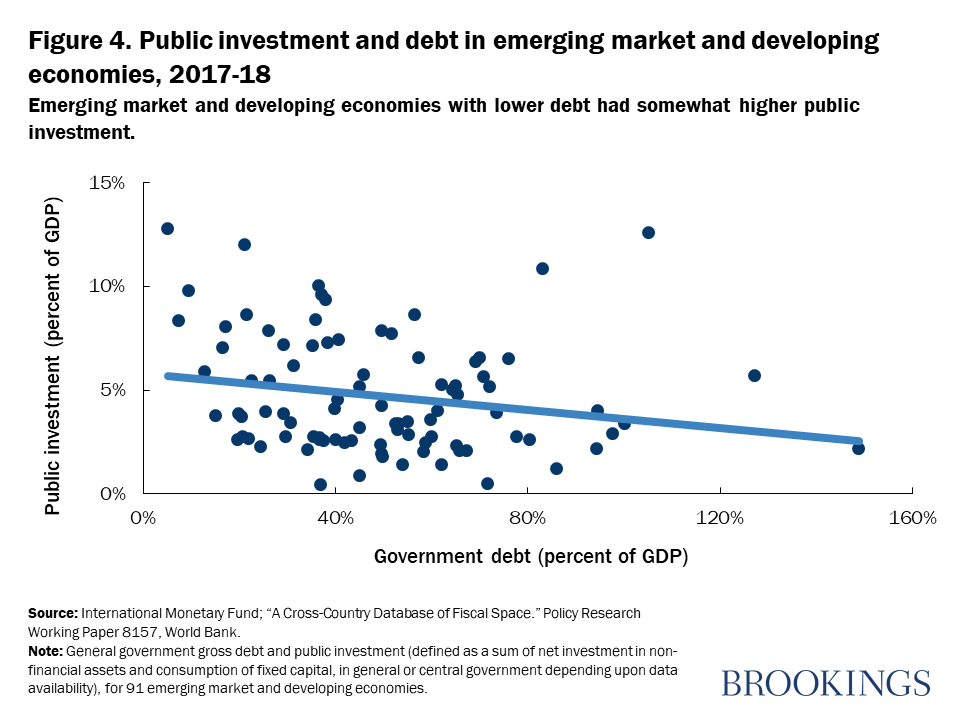

Constraining government action during downturns. High debt constrains governments’ ability to respond to downturns with stimulus. During the global financial crisis of 2008-09, fiscal stimulus was considerably smaller in countries with high debt than in those with low government debt (Figure 4). Not only the size but the effectiveness of fiscal policy could be constrained: High government debt tends to render expansionary fiscal policy less effective, reflected in lower fiscal multipliers.

Slowing investment and growth. With higher debt typically comes higher debt service. Spending on higher debt service needs to be financed through some combination of increased borrowing, increased taxes, and reduced government spending. Spending cuts may even reach critical government functions such as social safety nets or growth-enhancing public investment (Figure 5). High debt could also create uncertainty about macroeconomic and policy prospects and weigh on growth and crowd out private investment.

Adjusting the dose

Low-cost debt can be just the medicine EMDEs need to mend some of their development gaps. But, as the old adage goes, the dose makes the poison: Excessive debt accumulation has adverse side effects. In this context, the current low interest rates encourage complacency. History has repeatedly shown that borrowing costs can increase abruptly when adverse shocks strike. At that point, the risks inherent in the post-crisis debt buildup would become apparent. High debt will likely make governments more vulnerable to crises, limit the size and effectiveness of fiscal stimulus during cyclical downturns, and weigh on investment and longer-term growth.

Mechanisms and institutions can be put in place that help adjust the dose of debt that takes advantage of low interest rates while containing the adverse side effects of excessive debt accumulation. Greater debt transparency may mitigate costs associated with debt buildups and withstand political-economy pressures for debt increases.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Debt: The dose makes the poison

February 28, 2020