Below is a viewpoint from the Foresight Africa 2022 report, which explores top priorities for the region in the coming year. Read the full chapter on public health.

Never before in the last half century has Africa’s health care landscape seen so many changes and attracted so much interest. In fact, Africa’s health care sector would be worth an estimated $259 billion by 2030. While these trends reveal a lucrative opportunity for the private sector, if not well-regulated, Africa’s health care system could end up keeping more Africans below the poverty line. Thus, African countries have an opportunity to build on the health financing success of 2021 to strengthen the resilience of this sector and Africa’s people.

Never before in the last half century has Africa’s health care landscape seen so many changes and attracted so much interest. In fact, Africa’s health care sector would be worth an estimated $259 billion by 2030. While these trends reveal a lucrative opportunity for the private sector, if not well-regulated, Africa’s health care system could end up keeping more Africans below the poverty line. Thus, African countries have an opportunity to build on the health financing success of 2021 to strengthen the resilience of this sector and Africa’s people.

Out-of-pocket (OOP) health spending in Africa remains excessively high compared to other continents—just one weakness in Africa’s health systems that the COVID-19 pandemic has exposed. Indeed, despite the havoc the virus has wreaked, it has also provided the continent with opportunities to reshape its health infrastructure as well as its supply systems, urging a shift from donor and externally manufactured products to continental production systems leveraging opportunities created by the African Continental Free Trade Agreement.

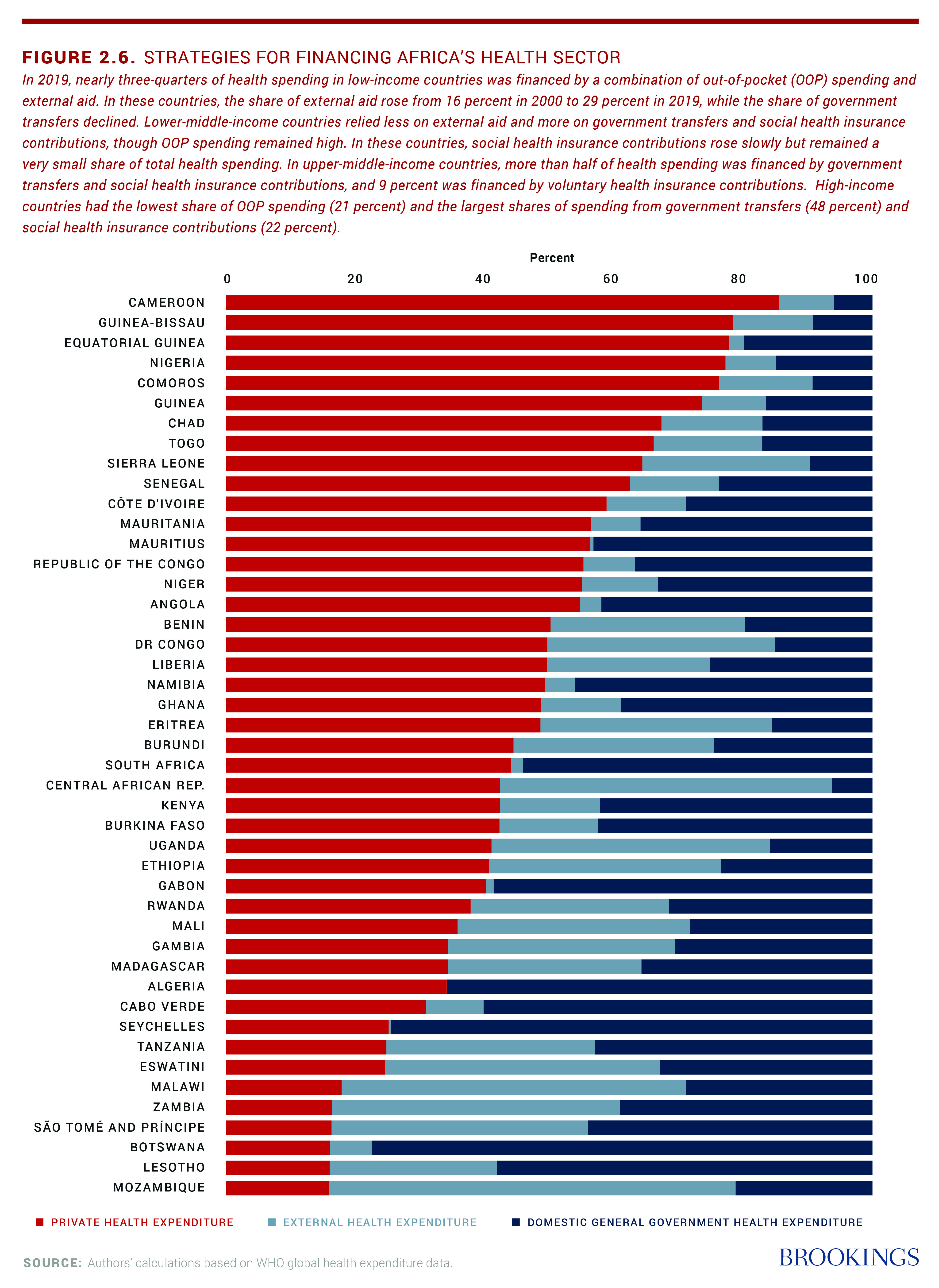

COVID-19 has created not only a health crisis, but an economic contraction never experienced before with such speed. In addition, the COVID-induced increase in unemployment is causing private sector spending on health to decrease at the same time COVID is adding to the cost of health care—in a region where private health expenditure already exceeds 50 percent of total health expenditure in over 15 countries (Figure 2.6 below). The immediate challenge for many governments is how to supply affordable and reliable health care in a fiscally constrained environment.

Prior to the COVID pandemic, a number of suggestions for increasing public support for the health sector had been proposed, primarily through domestic resource mobilization. However, in the face of economic contraction, increasing government revenue in the short term is no longer feasible.

Out-of-pocket (OOP) health spending in Africa remains excessively high compared to other continents—just one weakness in Africa’s health systems that the COVID-19 pandemic has exposed.

The immediate focus of international financial institutions, therefore, has been to support African economies to raise additional concessional resources. Over the course of the crisis, the G-20 provided three phased options for additional liquidity: Debt service suspension, special drawing rights, and an innovative financing approach to vaccine acquisition. Multilateral financial institutions also increased disbursement of new credits to countries to support additional health spending.

The G-20–building on a proposal from the African finance ministers and the Economic Commission for Africa (UNECA)—adopted the African proposal for a debt service suspension initiative (DSSI) as the first liquidity injection for low-income countries. The DSSI allowed countries to suspend debt payment obligations to creditors in 2020 and 2021 so that the governments could use the financial resources to respond to the global health crisis. These newly available resources were used to purchase personal protective equipment (PPE) and also support local production of PPE, which helped stand up some part of the economy.

In early 2021, the G-20 further approved the issuance of Special Drawing Rights (SDRs)—which had been called for by African finance ministers early in the pandemic—to the magnitude of $650 billion, of which Africa received about 5 percent (worth around $33.6 billion). These additional resources increased liquidity to countries to respond to both the health and the economic crises.

Relying on African institutions to finance and fight the pandemic has served Africa well throughout the crisis. As such, Africa has put in place a number of new institutions and innovative financing approaches to fund vaccine acquisition.

The first such institution is the African Medical Supplies Platform (AMSP), whose strength lies in its ability to pool demand for medical supplies in a transparent manner—thereby commanding lower market prices. Another important innovation was the creation of the African Vaccines Acquisition Trust (AVAT) by pooling SDRs from countries like Egypt, Nigeria, and Zimbabwe. It provided early resources for the African Export-Import Bank (Afreximbank) to set up a facility for vaccine procurement. Under the leadership of African Union Special Envoy Strive Masiwiya, and in collaboration with the African CDC led by Dr. John Nkengasong and UNECA, AVAT has been able to procure over 40 percent of Africa’s COVID vaccine needs (including a 70 million Moderna purchase from the U.S.). With the support of a $500 million donation from the Mastercard Foundation, the costs of vaccines under the AVAT mechanism are on par with those procured via COVAX. Indeed, in 2022, a major focus for leaders must be to administer procured vaccines: As of the end of 2021, less than 10 percent of Africa is fully vaccinated. (For more on vaccine equity, see Michel Sidibé’s viewpoint.)

Afreximbank also developed the AVAT No-Fault Compensation Program for Participating Member States. This program, the first of its kind on the continent, provides no-fault lump-sum compensation in full and final settlement of any claims to individuals who have suffered a “serious adverse event” resulting in permanent impairment or death associated with a COVID-19 vaccine procured or distributed under the AVAT Framework within any of the participating member states.

The COVID-induced increase in unemployment is causing private sector spending on health to decrease at the same time COVID is adding to the cost of health care.

The development of these innovative mechanisms means Africa can now go to the market to procure its own health commodities, empowering Africa to move from importing over 90 percent of its health needs to producing equipment and pharmaceuticals on the continent. This dynamic has already begun with countries like South Africa, Senegal, and Algeria increasing capacity and Rwanda, Kenya, Nigeria, and Morocco setting up new capacity for health sector commodity manufacturing.

With the COVID-19 pandemic, the need for closer collaboration between health and finance ministers became even more important. Indeed, inclusive, efficient, and effective health care financing needs both working together. There is now a call to create a Global Health and Finance Board to address fundamental problems of global governance for health, some of which were so clearly exposed by the (mis)management of the pandemic.

Africa is ahead of the game on this effort: Under the leadership of the African Union heads of state, Africa CDC, and UNECA, relevant ministers have held bi-monthly coordination meetings to align resources and delivery. This new mechanism could also be used post-pandemic to build and structure financing for more affordable and improved health care on the continent. The World Bank, the Mastercard Foundation, UNICEF, GAVI and others are already working through this mechanism to help address the biggest health challenge for Africa in 2022: vaccinations.

The Brookings Africa Growth Initiative receives support from the Mastercard Foundation.

Brookings is committed to quality, independence, and impact in all of its work. Activities supported by its donors reflect this commitment and the analysis and recommendations are solely determined by the authors.

Related Content

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Strategies for financing Africa’s health sector

February 3, 2022