The United States faces a persistent housing shortage, reflected in high home prices, low vacancy rates, and limited housing turnover. A large body of research points to restrictive local land use regulations as the primary driver, with recent increases in construction costs, labor shortages, and mortgage interest rates making matters worse.

Some proposals to alleviate the shortage would reduce or eliminate capital gains taxes for owner-occupied housing. Under current law, married homeowners may exclude up to $500,000 of capital gains from the sale of a primary residence ($250,000 for singles) but have to pay taxes on gains above those amounts. The argument is that homeowners—particularly older households with large accumulated gains—are reluctant to sell because of capital gains taxes and that lowering or eliminating those taxes would increase turnover and ease housing shortages.

We show, however, that even under current law, 95% of all households—and 90% of households aged 65 and older—would owe no federal capital gains tax on a home sale because their accrued capital gains fall below existing exclusion thresholds. Raising the tax-exempt level of capital gains on housing would have no effect on them. Instead, it would provide large benefits to a small group of high-income, high-wealth households. As a result, cutting capital gains taxes on housing cannot plausibly alter selling behavior very much or meaningfully increase housing supply.

An expanded exclusion overwhelmingly benefits high-income households

Prior research suggests that increases in the tax-exempt level of capital gains on housing did increase turnover somewhat. However, because the tax-exempt level is higher now, fewer households would be affected by a further increase.

To evaluate this issue, we use household-level data from the Federal Reserve Board’s 2022 Survey of Consumer Finances, which provides detailed information on household income, wealth, and accrued housing capital gains. We rank households by Expanded Income, which captures a wide array of cash and non-cash resources and provides a more complete picture of households’ economic position than adjusted gross income, particularly for homeowners and retirees.

Using this information, we calculate how much each household would have to pay in capital gains tax if they sold their house. This does not predict selling behavior; instead, it isolates who stands to benefit from an expanded exclusion if homes are sold.

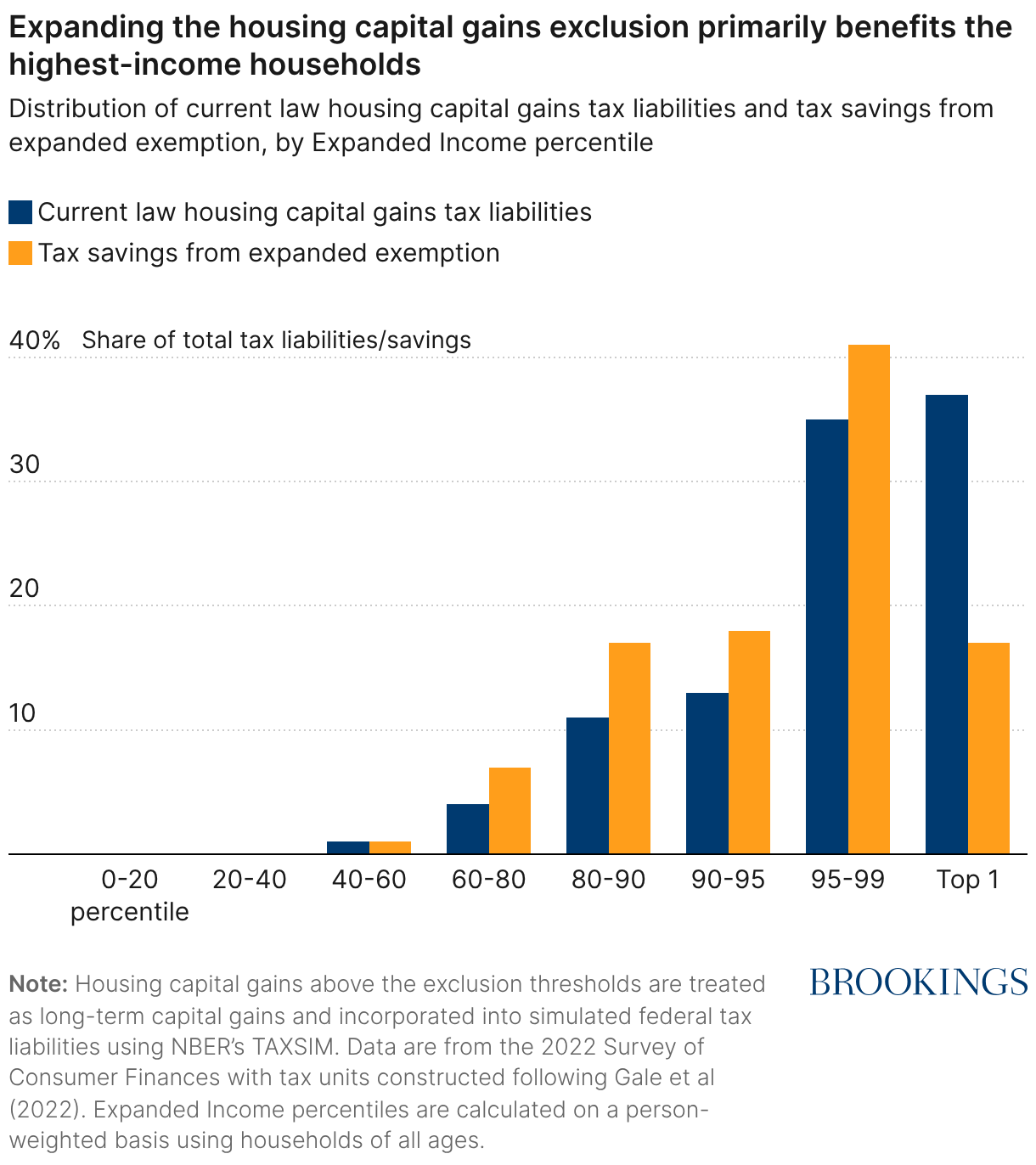

Figure 1 summarizes the distribution of capital gains tax liability under an “if sold” scenario, as well as the distribution of tax reductions under a doubling of the tax-exempt level of housing capital gains (e.g., to $1 million for married couples). These distributions indicate that a small share of households would bear any capital gains tax liability from selling under current law, and that small share would gain almost all the tax benefits of raising the tax-exempt level.

Roughly 85% of the total potential capital gains tax liability under current exemption thresholds falls on households in the top 10% of the expanded income distribution, with more than one-third (37%) borne by households in the top 1%. This concentration reflects the distribution of housing capital gains, which are overwhelmingly held by households with high incomes and substantial wealth.

The benefits of the exclusion are also highly concentrated. The vast majority (76%) of the total reduction in capital gains tax liability from doubling the exclusion would accrue to households in the top 10%, and nearly one-fifth (17%) would accrue to the top 1%. Households outside the top two deciles would receive little to no benefit from such a policy change.

Most senior households would see no benefit

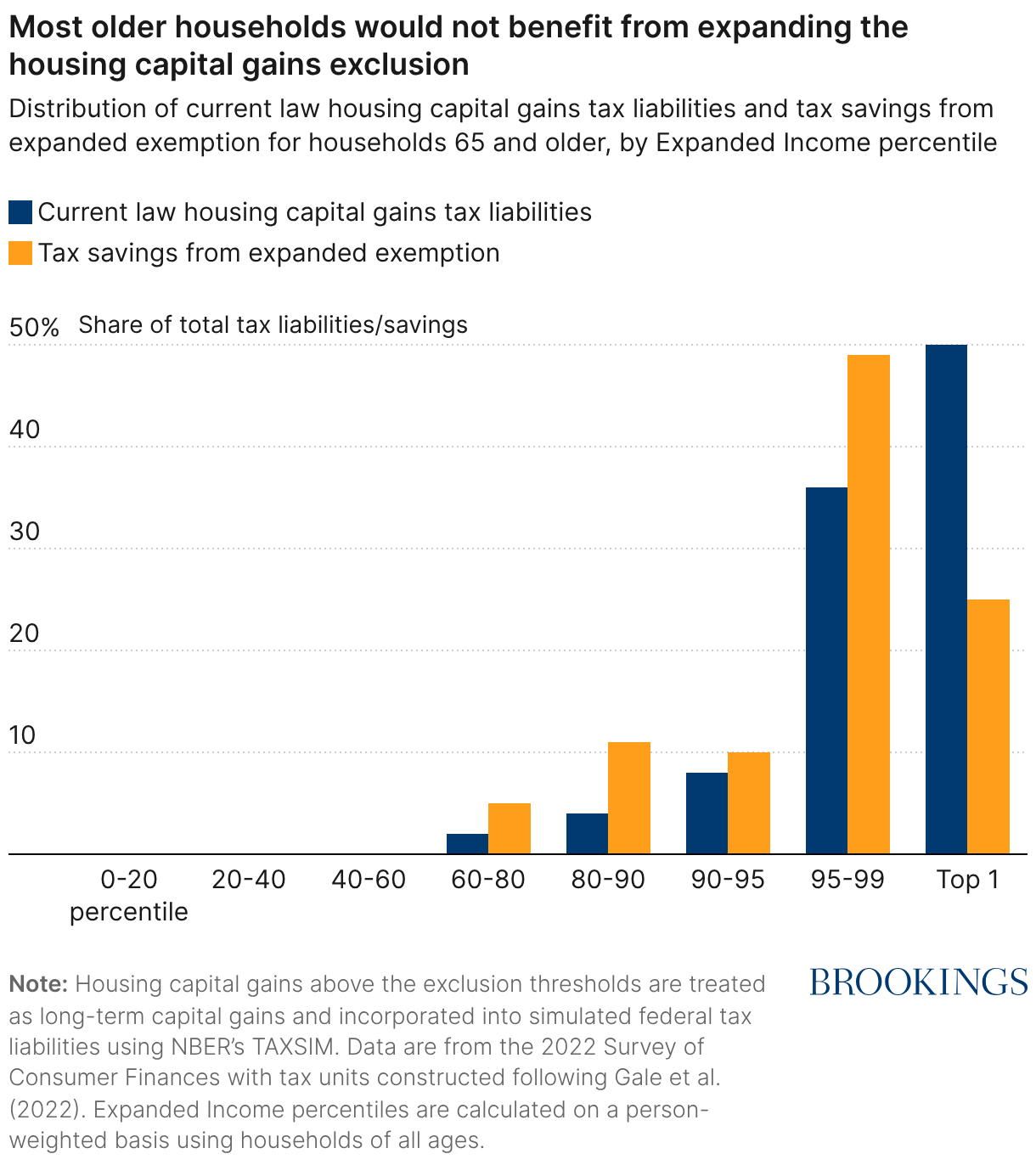

Older homeowners are often cited as the primary beneficiaries of proposals to expand the capital gains exclusion. Indeed, households headed by those 65 and older account for a substantial share of aggregate capital gains tax exposure (56%) and of the tax reductions (45%) associated with expanding the exclusion.

Figure 2 shows, however, that these aggregate patterns mask substantial heterogeneity within the senior population. The benefits of expanding the exclusion among older households are concentrated at the very top of the income distribution. Older households in the top 1% of the Expanded Income distribution account for half of total potential capital gains tax liability among seniors, and those in the top 5% account for the vast majority (74%) of the reduction from doubling the exclusion.

The capital gains exclusion won’t likely address affordability

Expanding the capital gains exclusion on home sales is often framed as a way to unlock housing supply, but the evidence suggests that it is poorly suited to that goal. Because capital gains tax liability on owner-occupied housing is already concentrated among a small group of high-income, high-wealth households, expanding the exclusion would likely do little to change selling behavior or meaningfully increase housing availability.

Instead, this policy would benefit high-income, high-wealth households and would add to an already extensive set of federal tax preferences for owner-occupied housing, including the exclusion of imputed rental income and the deductibility of mortgage interest and state and local property taxes. These provisions represent some of the largest federal tax expenditures and disproportionately benefit higher-income households.

In a housing market constrained by limited supply, policies that directly address barriers to housing construction are more likely to improve affordability than further expanding tax preferences for existing homeowners.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Will expanding the capital gains exclusion unlock housing supply?

Evidence on who benefits

February 2, 2026