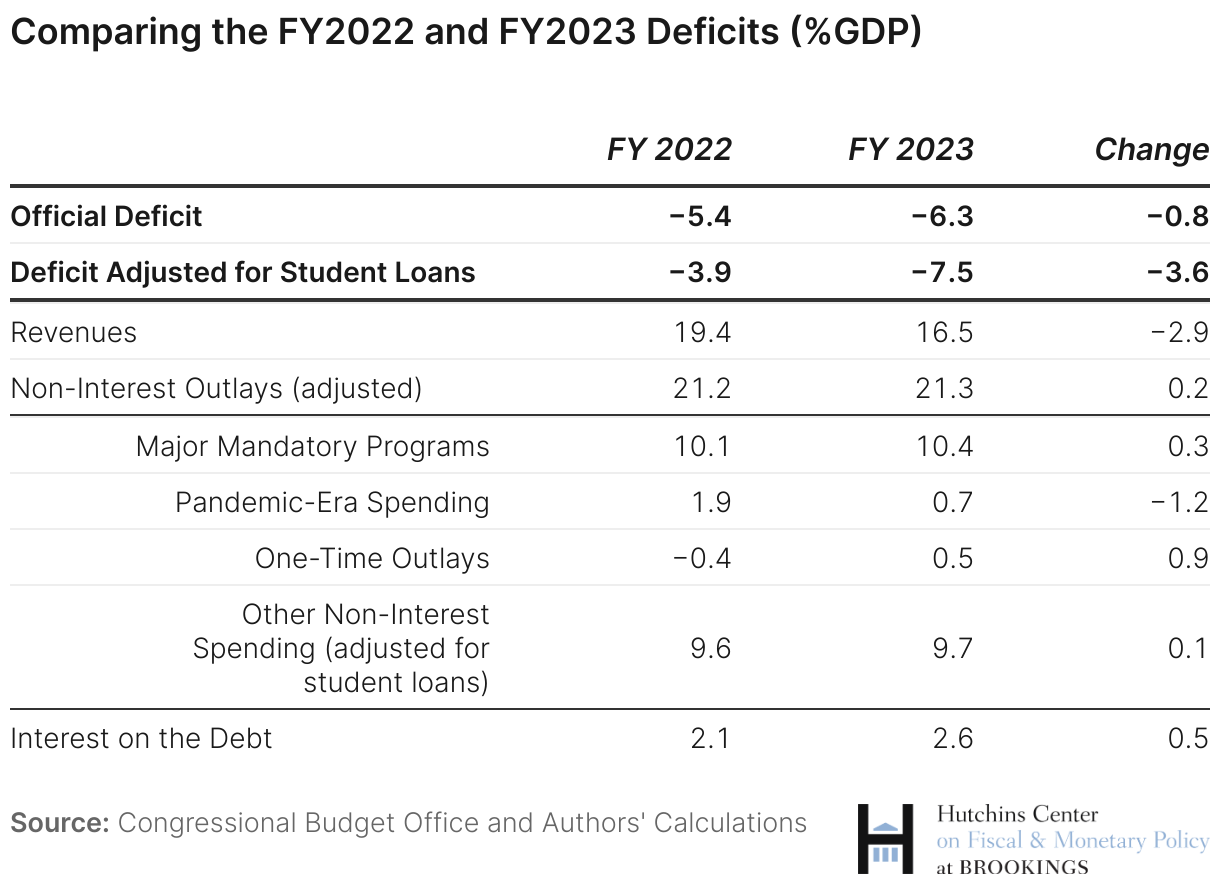

The federal budget deficit—the difference between government spending and revenues—increased from 5.4% of GDP in FY 2022 to 6.3% of GDP in FY 2023. Adjusting for the effects of President Biden’s student loan forgiveness program, which boosted the deficit in FY 2022 when it was announced and decreased it in FY 2023 when it was ruled unconstitutional, the increase was significantly larger—from 3.9% of GDP last fiscal year to 7.5% in 2023.

Why did the deficit increase so much?

As shown in the table below, a decline in revenues explains most of the increase. Revenues were extraordinarily robust in FY 2022—reaching 19.4% of GDP compared to the 2018-2019 (pre-pandemic and post-Tax Cuts and Jobs Act) average of 16.3% of GDP. Most of the strength was in individual income taxes—likely reflecting robust capital gains realizations because of the strong stock market, as well as lags in the adjustments of income tax brackets for inflation (which temporarily pushed people into higher tax brackets).

Revenues in FY 2023 were 16.5% of GDP—a bit above the 2018-2019 average. Revenues were depressed by several one-time or temporary factors. First, the IRS delayed both corporate and individual income tax filing deadlines for Californians affected by severe winter storms to November 2023 (which falls in FY 2024), lowering revenues in FY 2023 by about 0.3% of GDP. Second, refunds from the pandemic-era Employee Retention Tax Credit (which ended in 2021) surged in FY 2023 as businesses submitted amended returns, also lowering revenues by about 0.3% of GDP (relative to roughly 0.15% in FY 2022). Finally, high interest rates reduced Federal Reserve profits, causing the Fed’s remittances to the Treasury to fall from 0.4% of GDP in FY 2022 to about 0. Without these special factors, and assuming average Fed remittances, receipts would have been about 17.4% of GDP—less than in FY 2022, but still strong relative to recent history.

Spending excluding interest was just a touch higher as a share of GDP in FY 2023 than in FY 2022. Spending on the major mandatory programs—Social Security, Medicare, and Medicaid—rose by 0.3% of GDP. Reductions in spending on pandemic programs (the enhanced Child Tax Credit, Coronavirus Relief, and the Public Health and Social Services Emergency Fund) were largely offset by one-time spending increases by the Federal Deposit Insurance Corporation and Pension Benefit Guaranty Corporation and by low spectrum auction receipts (which are counted as negative spending). Higher interest rates pushed up the cost of debt service, increasing total outlays by 0.5% of GDP in FY 2023 relative to FY 2022.

What happened to the federal debt in FY 2023?

Despite the 7.5% of GDP adjusted deficit, the debt to GDP ratio rose only 1.6 percentage points from FY 2022 to FY 2023—from 96% to 97.6%. The intuition for this much smaller increase is as follows: High inflation raises the government’s borrowing costs—which boosts interest payments and the deficit as a share of GDP—but, because not all the government’s debt rolls over each year, high inflation boosts nominal GDP growth more. The change in the debt to GDP ratio is approximately equal to the primary deficit (revenues less non-interest spending) as a share of GDP less last year’s debt to GDP ratio multiplied by the difference between the government’s borrowing rate and the growth rate of GDP. So, by boosting GDP growth more than it boosts interest rates, an increase in inflation lowers the rise in the debt to GDP ratio, despite increasing the deficit.

How do the deficit outlook and debt outlook compare to pre-pandemic projections?

In January 2020, the CBO projected that the deficit would be 4.5% of GDP in FY 2023. The actual deficit was about 3% of GDP higher. However, the bulk of that difference is accounted for by pandemic-era programs, one-time outlays, and temporarily lower revenues. As of May 2023, CBO was projecting that deficits from 2024 through 2030 would be 0.9% of GDP higher on average than they had projected in January 2020. The increase is largely accounted for by higher interest payments on the debt accumulated during the pandemic, as higher projected discretionary spending is largely offset by lower than projected mandatory spending and stronger revenues.

What does the recent run-up in interest rates mean for the federal debt?

Interest rates have increased sharply in recent months. On November 20, 2023, the interest rate on 10-year inflation-protected Treasuries was 2.1%—up from 1.6% in January 2023, but down from the 2.5% observed just three weeks earlier. It is hard to know exactly what caused this surge in interest rates—and therefore hard to know whether it will persist. But if it does—and if it is not accompanied by higher productivity—it will make stabilizing the debt to GDP ratio more difficult.

When interest rates are below the growth rate of the economy—as they were for most years since 2010—the government can run small primary deficits (non-interest spending less revenues) without increasing the debt to GDP ratio. If interest rates are higher than economic growth, the government must run a surplus to keep the debt to GDP ratio from rising. High interest rates mean that a given set of tax and spending policies will lead to a steeper rise in debt to GDP and, also, that larger spending cuts (or revenue increases) will be needed to stabilize the debt to GDP ratio for any given level of the debt and deficit.

It’s possible that higher interest rates will be accompanied by (or are potentially the result of) higher productivity growth—perhaps from the adoption of artificial intelligence. Higher productivity growth has two effects. First, it lowers the primary deficit (revenues less non-interest spending) because revenues rise and spending falls as a share of GDP when productivity increases. Second, higher productivity growth boosts GDP, lowering any given level of debt relative to GDP.

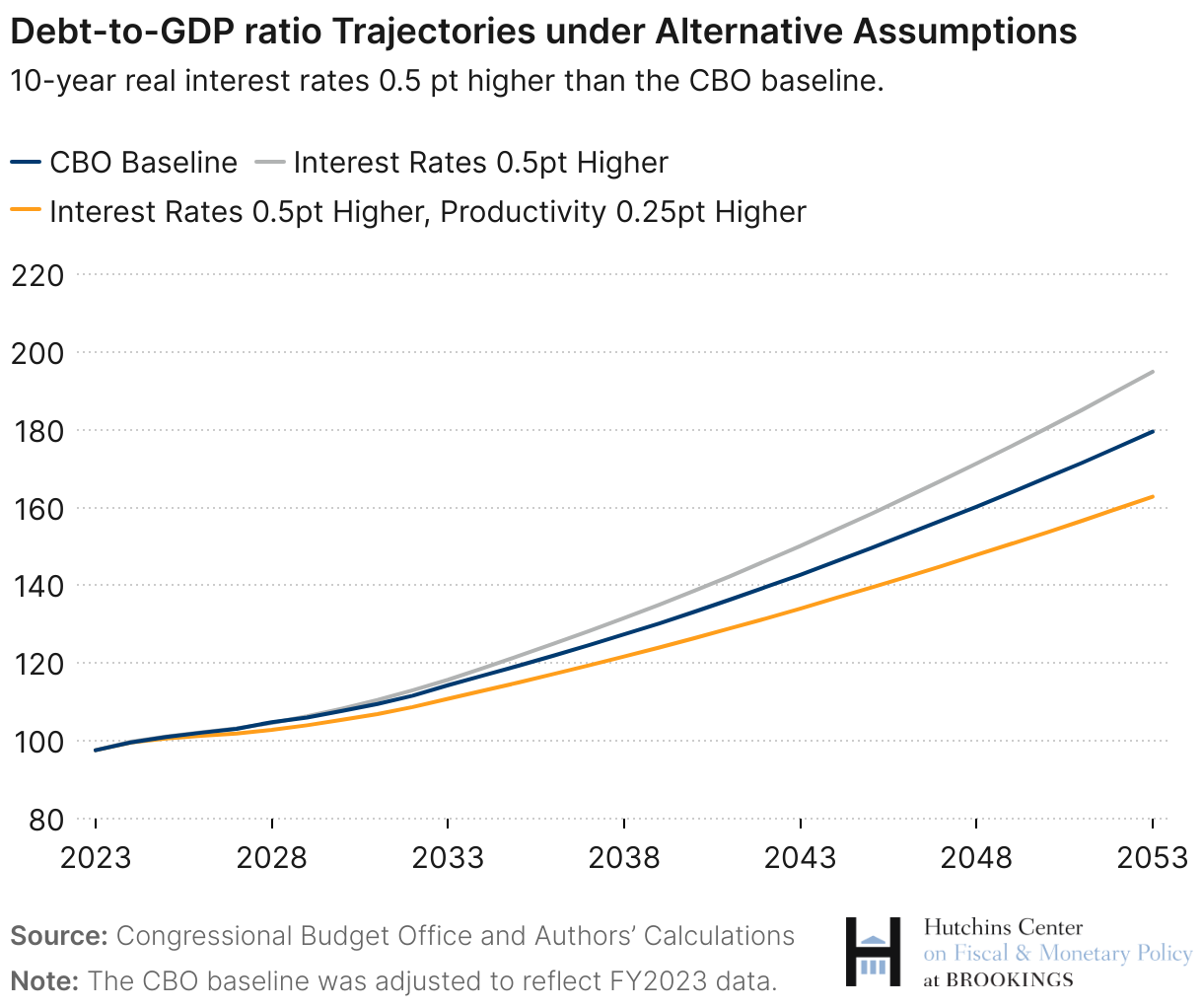

This graph shows a rough estimate of the effects of a 0.5 percentage point persistent increase in interest rates alone (about the difference between the inflation-adjusted rate that prevailed on November 20 and what CBO expected last May for 2025)—as well as the combined effects of that increase in interest rates combined with an increase in productivity only half as large (0.25 percentage point). Without an increase in productivity, the higher interest rates increase the debt to GDP ratio in 2053 from 180% in the baseline to 195%.1 But increases in productivity are quite powerful—even an increase in productivity growth of 0.25 percentage point is enough to more than offset the effects of the higher interest rates, bringing the debt to GDP ratio in 2053 down to 163% of GDP.

Bottom line

The recent increase in the deficit doesn’t fundamentally change the fiscal outlook for the U.S. Much of the increase is caused by temporary or one-off factors that have been offset in debt to GDP by inflation and strong growth. Persistently high interest rates, however, could exacerbate fiscal sustainability challenges unless accompanied by higher productivity growth.

Authors

Related Content

-

Acknowledgements and disclosures

The Brookings Institution is financed through the support of a diverse array of foundations, corporations, governments, individuals, as well as an endowment. A list of donors can be found in our annual reports published online here. The findings, interpretations, and conclusions in this report are solely those of its author(s) and are not influenced by any donation.

-

Footnotes

- In estimating this trajectory, we haven’t accounted for any macroeconomic feedback effects of higher interest rates on GDP growth. However, these effects would likely be fairly small, judging from CBO’s July 2023 analysis of a bigger rise in interest rates.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).