One of the most dangerous deficits the United States faces is not one of trade, values, or military capabilities but a deficit in understanding how we are connected to other societies around the world. The political, economic, and media errors resulting from this deficit can shortchange American consumers, producers, workers, and their families.

Commercial connections are a leading case in point. It is remarkable that cross-border trade in goods is still widely considered to be the primary benchmark for international commerce. That measure has been out of date for at least a half-century, and now is completely misleading in a world of extended supply chains, rapid technological change, and revived strategic competition.

Why? Because international commerce is more than just trade in goods. It also includes trade in services, which many pundits and politicians tend to ignore. Services account for a smaller share of global trade than goods, but they have been growing faster. More American jobs depend on services than on goods, and services are a U.S. competitive strength.

Moreover, just as trade is more than flows of goods, international commerce is more than just trade. It also includes investment, a deeper form of commercial connectivity. Most U.S. companies would prefer to set up shop close to their customers in overseas markets, rather than send their goods or services across an ocean. They’ve been doing so for over a century. For decades they have been joined by firms from many other countries. As a result of their activities, America’s investment ties with many countries are now far more valuable than its trade links.

Other flows are also critical. Cross-border data flows not only contribute more to global growth than trade in goods, they underpin and enable virtually every other kind of cross-border flow. The United States is the world’s leading hub for international trade in products delivered through data flows. International flows of research and development, and of talent, have also become critical to knowledge economies like the United States. Many firms now invest as much in intangible assets related to knowledge flows as they invest in traditional capital like machinery, equipment, and buildings. Keeping all these flows in mind can help us make sense of the numbers that are thrown at us every day, and to identify our most important commercial partners.

America’s commercial ties with China, for example, resemble a two-lane highway full of goods. Those lanes are busy and crowded. Any type of accident on a two-lane highway can really snarl traffic—as we saw when supply chains were disrupted by the COVID-19 pandemic and the U.S.-China tariff war, and as we see now as Beijing restricts flows of raw materials and Washington imposes curbs on semiconductors and other products. Alongside the goods highway are narrow bike lanes for services. Bilateral data and knowledge flows are more like pedestrian walkways: slow, narrow, and often constrained. A further lane for investment has been under construction for years, but it is full of potholes, as Beijing and Washington impose more restrictions. China experienced a massive reversal in foreign investment flows in 2023, and JPMorgan Chase estimates that about half of the $250 billion to $300 billion of international money that flowed into Chinese bonds since 2019 has now left. Chinese foreign direct investment (FDI) in the United States is also very modest: just seven deals worth $1.8 billion in 2023 and five deals valued at $2.6 billion in 2022.

Companies seeking to avoid China tensions and supply chain disruptions are changing how and where they buy, sell, and invest. Mexico has been one beneficiary. Recent media stories have proclaimed that Mexico displaced China in 2023 as the top trading partner of the United States. As usual, those reports focused only on goods trade. If one adds services, however, Mexico has been America’s top trading partner for some time: U.S.-Mexico trade in goods and services was already greater than that between the United States and China in 2021 and 2022.

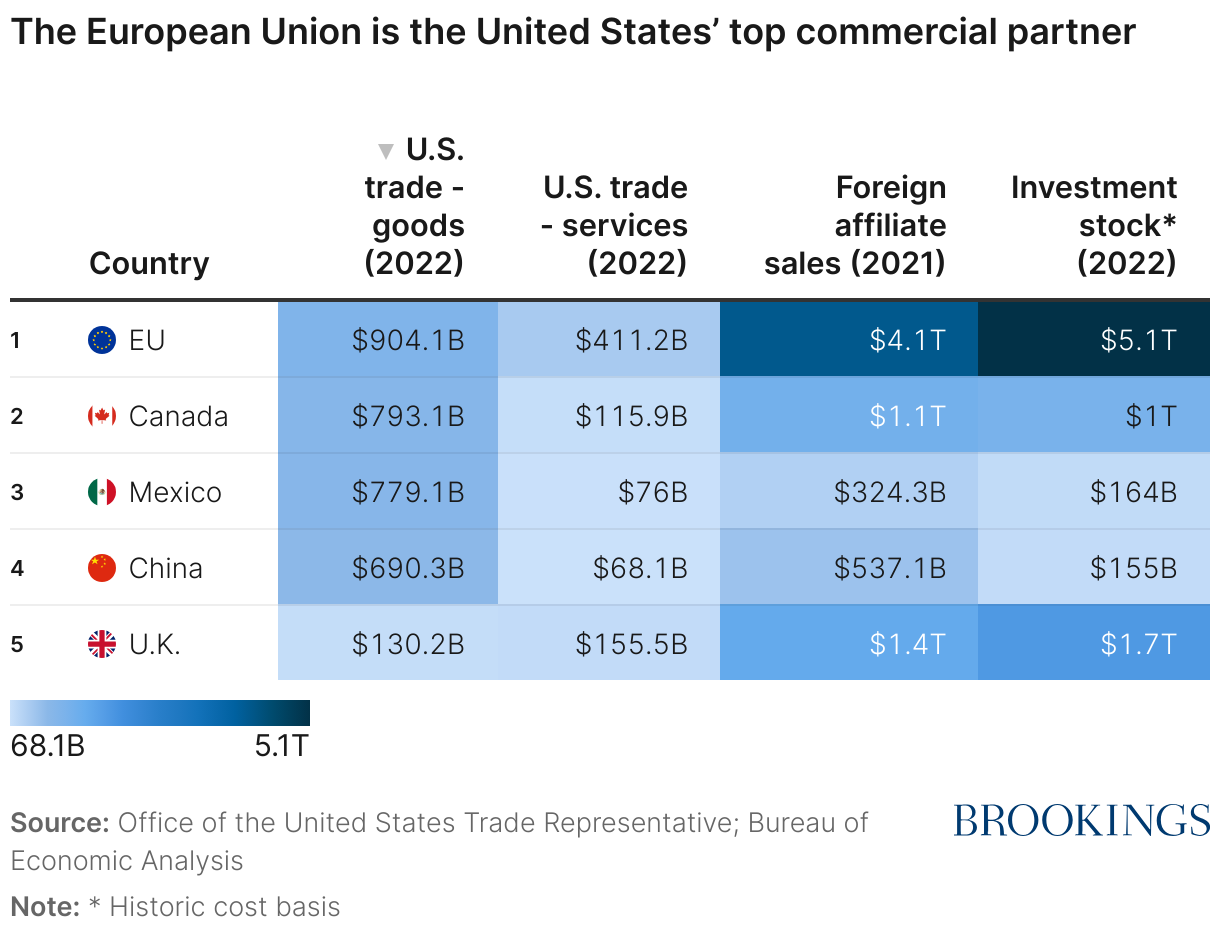

U.S. trade ties with China and Mexico are significant. Yet neither is America’s top commercial partner among foreign countries. That distinction belongs to the United Kingdom. U.S.-U.K. goods lanes are much smaller than U.S. goods highways with China or Mexico. U.S.-U.K. services trade, however, is greater than U.S. services trade with China and Mexico combined—nearly $156 billion in 2022, the last year of available data, versus U.S.-Mexico services trade of $76 billion and U.S.-China services trade of about $68 billion.

The real difference, however, can be traced to massive mutual investment. At $1.74 trillion, U.S.-U.K. investment stock is over 11 times more than U.S.-China investment stock ($154.8 billion) and over 10 times more than U.S.-Mexico investment stock ($164.1 billion). U.S. FDI in the U.K. alone is greater than U.S. FDI in the entire Asia-Pacific region. Sales of American and British affiliates in each other’s markets in 2021 ($1.4 trillion) were 21 percent more than the combined sales of U.S. affiliates in all of Latin America (including Mexico) and Latin American affiliates in the United States ($1.1 trillion). Those investments also create jobs: U.K. companies are the largest source of onshored jobs in the United States, just as U.S. companies are the largest source of onshored jobs in the U.K.

Arguably, the most significant commercial partner for the United States is not a country; it is the European Union (EU). Since the EU comprises 27 countries, some may consider comparisons with China, Mexico, or the U.K. unfair. But EU member states have delegated their sovereignty over trade matters to the European Commission; its trade commissioner speaks, acts, and negotiates for the union. The commission also handles the EU’s Single Market, where most commerce can flow without facing intra-EU tariffs or the type of restrictions that characterize the U.S.-Mexico-Canada free trade agreement (USMCA) or commercial connections in East Asia.

The commercial highway connecting the EU with the United States looks less like a two-way street than a 12-lane Autobahn. Not only are there fewer speed limits and wider goods lanes than either partner has with China, but there are additional lanes for services, investment streams, and sales by companies on each side of the Atlantic. Trans-Atlantic digital lanes carry 75 percent of global digital content. Innovation lanes hosting research and development flows are the most intense between any two international partners. Jobs lanes employ more than 16 million Americans and Europeans.

China’s rise as a global goods powerhouse can easily lead one to conclude that China is the main trading partner of the United States and the EU. This is not true. U.S.-EU goods trade in 2023 (about $946 billion) was 39 percent higher than U.S.-China goods trade ($575 billion) and 15 percent higher than EU-China goods trade ($805 billion). U.S.-EU services trade totaled $411 billion in 2022, the last year of available data. That was about six times more than U.S.-China services trade ($68 billion) and 3.6 times more than EU-China services trade ($122 billion).

Putting goods and services together, U.S.-EU trade totaled $1.3 trillion in 2022. EU-China trade of $1.06 trillion was only about 82 percent as large, and U.S.-China trade of $758.4 billion was only 58 percent as large. German officials and business leaders regularly state that China is Germany’s top trading partner. But China-Germany trade in goods and services of $348.45 billion was about 12 percent less than U.S.-Germany trade of $394.15 billion in 2022. And both U.S.-China trade and EU-China trade weakened in 2023, while U.S.-EU trade strengthened.

The discrepancies are even more glaring when one looks at investment. U.S. investment stock in the EU in 2022 ($2.7 trillion) was more than 21 times more than U.S. FDI stock in China ($126.1 billion). EU investment stock in the United States in 2022 ($2 trillion) was double the level of comparable investment from all of Asia ($1 trillion).

Comparisons with USMCA are also instructive. U.S. goods and services trade with USMCA partners Mexico and Canada totaled $1.76 trillion in 2022, more than the equivalent U.S. trade with the EU of $1.3 trillion. But as mentioned, most firms prefer to set up shop in the other market rather than conduct trade across borders. Mutual investments by U.S. and EU firms, and the jobs, sales, and wealth they generate in each other’s markets, far outstrip U.S., Mexican, and Canadian investments in North American markets, and are far greater than any trade flows. U.S.-EU foreign affiliate sales of $4.1 trillion in 2021 were three times more than USMCA foreign affiliate sales of $1.4 trillion. The combined U.S.-EU investment stock of $5.1 trillion in 2022 was four times more than the combined U.S.-Canada-Mexico investment stock of $1.3 trillion.

In sum, when one compares the full spectrum of U.S. commercial relations with other countries around the world, it becomes clear that the United States and the EU are each other’s most significant commercial partners, as they have been for decades. Of course, specific sectors of each economy are dependent on China and other countries for things like critical raw materials. However, given geopolitical differences, these dependencies have become a cause for concern. The dense commercial linkages binding the U.S. with the EU, the U.K., and other European democratic market economies offer a solid geo-economic and geostrategic grounding from which each side of the North Atlantic can address those concerns. Indeed, if they can manage to stick together and identify ways to harness their combined potential more fully, they will equally be prepared to address the further tremors still to come.

Author

Related Content

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Who is America’s top commercial partner? (Hint: It’s not China.)

March 21, 2024