From August 1-3, 2018, the Global Economy and Development Program at Brookings hosted the 15th annual Brookings Blum Roundtable on challenges to and opportunities for U.S. foreign assistance and global leadership. The following is one of six briefs related to this year’s theme: “Invigorating U.S. Leadership in Global Development.”

If the U.S. is to exercise global leadership with its foreign assistance, it should view its contributions and support through a Sustainable Development Goals lens. This would reinforce the long-standing principle of U.S. assistance that it respect universal country ownership rather than a U.S. driven agenda.

Almost three years have passed since the Sustainable Development Goals and Agenda 2030 were adopted by 193 countries at the United Nations General Assembly. Since then, focus has switched to implementation. Here the news is not good. Indicators of 14 out of 16 targets directly related to individuals (like poverty, education, or child mortality) are unlikely to get more than half way to their agreed 2030 endpoint. Child obesity is headed in the wrong direction. Violence against women may only reach 10 percent of the target level.1It has become commonplace to say that “business-as-usual” will not suffice, but it is less easy to be clear about what needs to change, whose actions need to change, and how can change be organized.

There is an urgency to SDG implementation. Time is running out. If the estimated trends do not change, many lives will be lost or damaged, and, in the longer-run, development trajectories for the next few decades will be adversely affected. A narrow window of opportunity that exists today is closing.

Consider the following: more infrastructure will be put in place in the next 15 years than the entire stock of the world’s current infrastructure. Make it low carbon and sustainable, and the worst effects of climate change can be averted. From a different perspective, think about the fact that more people are now moving to cities than ever before, or than ever will again. Plan cities smartly, in terms of inclusive public services, transport and land-use, and inequality in our societies can be reduced. Also, reflect on the demographic bulge unfolding in Africa, the last place on earth where the number of children will expand over the next 15 years. Only by keeping these children alive, healthy and skilled can we avoid a generation being left behind.

In each case, choices made now and over the next fifteen years will lock in carbonization, urbanization, and demographic trends that will shape the future of humanity for decades to come.

If there is to be change, someone has to lead it. The U.S. can and should resume its role as leading the world towards sustainable development. U.S. citizens agree: in 2017, two-thirds responded “yes” to the question “Do you think it will be best for the future of the country if we take an active part in world affairs?”2 The U.S. should align its foreign assistance with the SDGs and, using that framework, build local and international coalitions with a range of government and non-government actors, including business, civil society and academia. To do that, it should consider:

- What the Federal or local government needs to do to get the U.S.’ own house in order.

- How to catalyze and partner with the U.S. corporate sector, non-governmental organizations and

civil society. - Where to engage internationally.

What the federal and local governments need to do domestically

Global leadership on sustainable development should begin with credible domestic action. Agenda 2030 is universal and, between 2016 and 2018, 112 countries have submitted voluntary national reviews of their implementation plans at the U.N.’s High Level Political Forum. The U.S. is not among them. The domestic SDG agenda for the U.S. (and indeed for most other countries) can be distilled into three broad action areas:

- reinvigorate the long-term trend of overall economic growth;

- re-couple economic progress with social well-being, and;

- de-couple economic growth from environmental “bads” (pollution, carbon emissions).

The U.S. is not faring well on any of these. Growth is picking up, but, according to IMF forecasts, this is cyclical. Real GDP growth could accelerate this year and next to levels just shy of 3 percent thanks to the fiscal stimulus, but this will dissipate, and growth is projected to return to 1.4 percent (0.6 percent per capita) by 2023. On the need for re-coupling, the gulf between growth and well-being is well-illustrated by stories of opioid use and rising suicides occurring alongside economic recovery. De-coupling of environmental bads has been thrown into question by the U.S. withdrawal from the Paris Agreement and the weakening of fuel economy standards and other environmental regulations that the Trump Administration believes are constraining growth. The growth/environment policy trade-off is tilting back toward growth.

The SDGs provide a frame for analyzing and tackling these issues in a coherent way to improve the chances of sustainable long-term progress. Indeed, the U.S. would do well to learn from the SDG-related processes of other countries.

As a start, a stocktaking of the current situation is revealing. A recent review of national baselines on SDG indicators warns that the U.S. must overcome major challenges to meet 12 of the 17 goals.3In this, the U.S. is not alone. No country is on-track to meet all the goals. Yet other countries have set in train a process for action. They have requested their statistical offices to identify and monitor key indicators, adopted a national action plan for implementation, or at least modified or aligned an existing national plan or program with the SDGs. They have undertaken an assessment of a baseline and trajectories to identify the largest gaps and priority actions. Every G20 country, with two exceptions—the United States and Russia—has followed, or plans to follow, each of these steps. To be fair, the U.S. has set in place a national reporting platform to identify and update sustainable development statistics,4 but two-thirds of proposed indicators still require improvements or further exploration of the data.

Local mayors and governors are at the forefront when it comes to leading the domestic SDG agenda, rather than the federal government. New York City presented the first Voluntary Local Review to the U.N.’s High Level Political Forum in July. Other cities are joining in the effort. Los Angeles has undertaken Global Ambition, Local Action (GALA), a public commitment to the SDGs, and, through a partnership with Occidental College is mapping and prioritizing against the goals. Both Baltimore and San Jose have developed plans consistent with the U.S. Cities SDG Index developed by the Sustainable Development Solutions Network (SDSN).5In the SDSN U.S. Cities Index, common challenges for all U.S. cities include eradicating poverty (Goal 1), healthy food and diets (Goal 2), health and wellbeing for all (Goal 3), gender equality (Goal 5), providing affordable and clean energy for all (Goal 7), reducing inequality (Goal 10), and climate action (Goal 13).

On climate action, in particular, the We Are Still In campaign has attracted the support of local political and civic leaders representing over half the U.S. population, and significant local government participation is expected at the Global Climate Action Summit in California in September. This activist groundswell could provide a springboard for broadening the local agenda to take on other aspects of the SDGs, including social equity and inclusiveness issues.

Partnering with business

Sustainability concerns have become deeply embedded in many large corporations that now systematically look at business risks and opportunities stemming from climate change, pollution, decent work, and product safety. Indeed, in the U.S., businesses are moving way ahead of the government. About 80 percent of the companies listed in the S&P 500 now report publicly on their sustainability performance, and a growing number of companies are starting to align their sustainability strategies with the SDGs.6The issue, then, is not reporting individual company performance per se, but to set common standards, establish industry-wide goals, and develop comparable metrics to drive greater competition and impact at the company level.

The U.S. could be taking the lead in these areas, especially given the power of its financial institutions and intermediaries and the global footprint of its largest corporations. The prize is substantial. The Business and Sustainable Development Commission (2017) identified $12 trillion in new market opportunities in just four economic systems—food and agriculture, cities, energy and materials, and health and well-being. Banks seem to agree—setting an example, Bank of America, JPMorganChase, and Citigroup have made combined commitments to facilitate at least $50 billion per year in green finance through 2025. The competition to be sustainable will affect companies’ long-term ability to attract and retain talent, as well as their ability to build consumer loyalty and remain globally competitive.

Increasingly, attention is shifting to the role of investors. A growing body of evidence suggests that high-rated environmental, social, and (corporate) governance (ESG) companies are more profitable, have less volatility and risk, and have higher price/earnings valuations.7Outside the U.S., some investors, like Swiss Re, have begun shifting their entire portfolio towards ESG indices. With several ESG indices outperforming other benchmarks, ESG-based benchmarks could become a new standard for performance. This could trigger a wave of change. One Forbes analyst argues that, when 10 percent of top investors start to focus on system-level issues around sustainability, it generates attention among all stakeholders. When 30 percent of top investors focus on sustainability, there could be a culture change within the financial community. When a two-thirds threshold is reached, there will be systemic change.8

What is emerging from these and other studies is a new narrative of business and sustainability, one that recognizes that long-term profits and good performance on material non-financial aspects of business go hand in hand. Even in the world of impact investing, the vast majority (85 percent) of respondents believe there is no need to accept financial returns that are substantially below market in exchange for better ESG impact—the two simply go together.

The idea that private business can contribute substantially to global progress on the SDGs is one that the U.S. should embrace and encourage. U.S. reporting standards, like the industry-specific disclosures recommended by the Sustainable Accounting Standards Board, could be adopted by more companies as the format to be used in Form 10-K filings that provide annual reports on firms’ financial performance. While the Securities and Exchange Commission has not issued specific guidance on disclosures, this is partly because of the view that rapidly changing technology and data availability can alter management’s discussion and analysis of financial conditions. Given the rapid pace of change, standards should evolve over time rather than be restricted to a standardized format. Nevertheless, greater comparability across firms would help provide valuable benchmarking information for management and for investors. The Task Force on Climate-Related Financial Disclosures provides guidance to companies on what constitutes effective financial disclosures across industries.9

Several countries are developing their own standards for sustainability reporting. The European Commission’s High Level Expert Group on sustainable finance made recommendations in early 2018 to pension funds to “proactively seek and incorporate” beneficiary preferences in their decision making. China has become the largest global issuer of green bonds and is pushing aggressively to set standards for compulsory disclosure of listed company environmental performance.

The U.S. government also works with U.S. companies and entrepreneurs to advance technology breakthroughs for development. The Development Innovation Ventures program of USAID uses a venture capital model to conceive, test, and scale new technologies in global health, trade, energy, food security, and other sectors. NGOs, universities, companies and social enterprises have partnered through this program. Its future, however, is uncertain.

The absence of strong U.S. initiatives could mean that U.S. businesses lose any first-mover advantages from setting global standards, developing new business models for development, or blending finance in novel ways.

Engaging internationally

The U.S. has been the largest aid donor in the world, by some considerable margin, ever since World War II, based in part on the highly successful experience with the Marshall Plan. From this vantage point, the U.S. was responsible for the creation of the Development Assistance Committee of the OECD, the Global Fund, Gavi, the Vaccine Alliance, and other institutions. It is also the dominant shareholder in the World Bank and the major regional development banks.

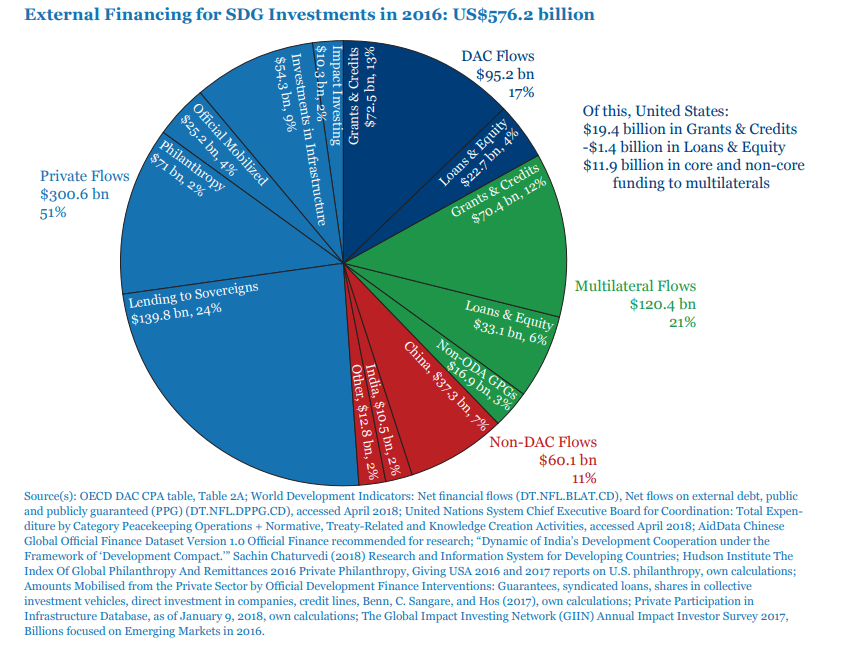

This U.S. leadership, however, has been eroded by a shake-up in the international development financing architecture. First, as illustrated in the figure that follows, official aid has become a far smaller share of the external financing for SDG investments.10 Second, non-aid sources of finance, particularly market-priced loans from official agencies, have become important. The U.S. has not had a large presence in these nongrant forms of development finance. For example, the foremost U.S. official lending institution, the Overseas Private Investment Corporation (OPIC), announced only $3.7 billion in new commitments for FY16, a small fraction of the total flows to developing countries. Across all official lending agencies, net U.S. lending was negative $1.4 billion in 2016—that is, U.S. public lending institutions reduced their exposure to the developing world.11

China, by contrast, has encouraged its two large public banks, the China Development Bank and the China ExIm Bank, to lend more to developing countries. These two institutions alone had outstanding foreign loans of about $675 billion in 2016. The Bank for International Settlements reported that total Chinese cross-border claims amounted to $970 billion in Q2, 2017. (This includes claims on developed country counterparties, but it appears that for a significant number of African and emerging and developing countries in Asia, Chinese banks are the main lenders.12)

External Financing for SDG Investments in 2016: US$576.2 billion

A project-by-project compilation of Chinese development financing suggests that loans and credits reached $37 billion in 2014, and this would seem conservative. At that level, Chinese financing would be significantly larger than the $30 billion provided annually by the U.S. and very different in its composition. U.S. flows are primarily grants, and considerable amounts (about one-third) flow through multilateral organizations. Chinese flows are mostly loans that flow directly through Chinese institutions.13 (The same pattern shows up in other emerging economies. India, for example, disbursed about $10 billion in development financing in 2016, to 63 countries, with the vast majority being lines of credit.)

There are also major differences between the U.S. and China in terms of the intended purpose of their development finance. The U.S. gives substantial humanitarian aid (over $6 billion per year) to wherever it is needed in the world. China is focused on infrastructure lending within carefully selected countries of strategic interest. China’s signature initiative for development finance is the Belt and Road Initiative (BRI), currently accounting for about one-third of its aid. The scale and scope of the plan is enormous, with financing gaps of over $100 billion per year in participating countries. China alone will not fill these funding gaps, but the BRI offers some insight that lack of demand will not be the key constraint on China’s development finance.

Beyond the BRI, China has invested significantly in sub-Saharan Africa, as well as in Latin America. There is considerable debate as to the quality and impact of these investments. On the negative side, arguments run from complaints that Chinese foreign investments are motivated more by a need to off-load slack in its domestic construction industry through overseas infrastructure projects rather than to meet developmental purposes, to the lack of attention to ESG standards and maintenance in the use of the assets being built, to the dangers posed by high debt levels linked to Chinese finance. On the positive side, analysts point to the fact that workers in China-sponsored projects are largely African, the loans extended to governments are not predatory loans, and there is little evidence of land grabs.14 Some countries like Ethiopia have used Chinese investments to sharply increase public investment and generate favorable growth dynamics. It is too early to tell which of these narratives is closer to reality, but there is no doubt that the Chinese model is dramatically different from the U.S. model in scale and composition.

Conclusion

The U.S. has long exercised global development leadership through its role as the world’s largest aid donor in absolute terms (by some considerable margin) and through its influence in the multilateral development institutions that it created. In addition to its own leadership role, the U.S. government has also proactively supported U.S. companies, universities, foundations, and humanitarian organizations in their efforts to invest and operate internationally and engage on global development issues.

The new world of development finance, however, revolves around loans, often for infrastructure projects. It engages private businesses. On this front, other countries, in particular China, have leapfrogged the U.S. both in the instruments they use and in the standards they are setting for sustainable finance.

At the same time, the priorities for the global development agenda are no longer being set by large individual donors like the U.S. They have been determined through a multilateral accord of 193 countries that negotiated and agreed on the SDGs as the framework to guide them through 2030. The U.S. has been slow to align its own policies and approaches to this agenda and risks losing credibility and competitiveness by failing to seriously address the domestic components of the agenda.

The agenda for the U.S. is therefore threefold:

- Show through its domestic programs that it is taking the SDGs seriously and that it is prepared to use this experience and its international assistance to help other countries achieve their goals.

- Strengthen its partnerships with the private sector, especially with financial intermediaries, to set standards that more closely align finance and long-term development, and devise options through which large corporations could adopt an SDG focus for their domestic and international operations alike.

- Add blended finance to its toolkit, especially in areas like sustainable infrastructure where affordable long-term debt is a key constraint, and scale this up to establish itself as a leader in this area. Here, the U.S. needs to take a hard-nosed look at how it views developing country creditworthiness. Too cautious an approach leaves gaps unaddressed; too aggressive an approach can lead to debt distress and developmental backsliding. The quality of design and implementation of debt-financed investments are vital to finding the right balance.

Related Books

Author

-

Footnotes

-

H. Kharas, J. MacArthur and K. Rasmussen, “Counting People Left behind: Estimating SDG Trajectories to 2030,” The Brookings

Institution, July 2018 - 2017 Chicago Council Survey

-

Guido Schmidt-Traub, Christian Kroll, Katerina Teksoz, David Durand-Delacre, Jeffrey D. Sachs “National baselines for the Sustainable

Development Goals assessed in the SDG Index and Dashboards,” July 2017, Nature Geoscience 10(8) -

Official U.S. Federal Statistics for the U.N. Sustainable Development Goals, October 2017, “Measuring America: U.S. Statistics for

Sustainable Development” https://sdg.data.gov/statistics/ -

J. Espey et al. “Leaving No U.S. City Behind: the U.S. Cities Sustainable Development Index, 2018.” http://unsdsn.org/wp-content/

uploads/2018/06/US-Cities-Index-Report.pdf -

J. Nelson, “Collective Action on Business Standards, Goals, and Metrics to Achieve Scale and Impact for the SDGs” in Desai, Kato,

Kharas and McArthur From Summits to Solutions, Brooking Press, 2018 -

MSCI, November 2017, “Foundations of ESG Investing”

https://www.msci.com/documents/10199/03d6faef-2394-44e9-a119-4ca130909226 -

Bob Eccles, March 2018, “Measuring Investors’ Contributions To The Sustainable Development Goals,” Forbes. https://www.forbes.

com/sites/bobeccles/2018/03/11/measuring-investors-contributions-to-the-sustainable-development-goal/2/#eaf233052f02 - Task Force on Climate-Related Financial Disclosures, https://www.fsb-tcfd.org/about/

-

Such financing consists of: (i) cross-border investments made by official providers of development finance; (ii) private investments

that are mobilized within such projects; (iii) private finance for infrastructure (no data is available for other sectors); (iv) sovereign

borrowing from private capital markets; (v) philanthropic flows and (vi) private impact investments. The Figure also includes all

flows to finance U.N. peacekeeping and work towards global norms and standards, on the grounds that these are integral to achievement

of the SDGs, even if they are not considered as ODA because they do not uniquely benefit developing countries. There are

many other investments that could also contribute to the SDGs, for example foreign direct investment in the food system could help

alleviate hunger, but there are no good data that would allow us to disaggregate FDI into SDG-related and other investments so we

are limited to only including private investments in infrastructure where data do exist. - The BUILD Act is a welcome effort to reverse these data.

-

E. Cerutti and H. Zhou, February 2018. “The Chinese banking system: Much more than a domestic giant,” Vox CEPR Policy Portal,

https://voxeu.org/article/chinese-banking-system -

China also provides considerable grant/concessional credit financing, estimated at $5.8 billion most recently, a volume that would

make it the fifth largest aid giver in the world. -

D. Bräutigam, “U.S. politicians get China in Africa all wrong,” The Washington Post, April 12, 2018. www.washingtonpost.com/news/

theworldpost/wp/2018/04/12/china-africa.

-

H. Kharas, J. MacArthur and K. Rasmussen, “Counting People Left behind: Estimating SDG Trajectories to 2030,” The Brookings

Institution, July 2018

Development Goals assessed in the SDG Index and Dashboards,” July 2017, Nature Geoscience 10(8)

Sustainable Development” https://sdg.data.gov/statistics/

uploads/2018/06/US-Cities-Index-Report.pdf

Kharas and McArthur From Summits to Solutions, Brooking Press, 2018

https://www.msci.com/documents/10199/03d6faef-2394-44e9-a119-4ca130909226

com/sites/bobeccles/2018/03/11/measuring-investors-contributions-to-the-sustainable-development-goal/2/#eaf233052f02

that are mobilized within such projects; (iii) private finance for infrastructure (no data is available for other sectors); (iv) sovereign

borrowing from private capital markets; (v) philanthropic flows and (vi) private impact investments. The Figure also includes all

flows to finance U.N. peacekeeping and work towards global norms and standards, on the grounds that these are integral to achievement

of the SDGs, even if they are not considered as ODA because they do not uniquely benefit developing countries. There are

many other investments that could also contribute to the SDGs, for example foreign direct investment in the food system could help

alleviate hunger, but there are no good data that would allow us to disaggregate FDI into SDG-related and other investments so we

are limited to only including private investments in infrastructure where data do exist.

https://voxeu.org/article/chinese-banking-system

make it the fifth largest aid giver in the world.

theworldpost/wp/2018/04/12/china-africa.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).