This article was originally published by the Open Banker in November 2024.

America returned to limited deposit insurance and the sky didn’t fall; heck, few noticed. First National Bank of Lindsay Oklahoma failed on October 18, 2024, the first bank to fail with uninsured depositors taking losses since the most recent cycle of bailouts began with Silicon Valley Bank (SVB) in March 2023. Here is why we should commend the Federal Deposit Insurance Corporation (FDIC) for following the law which prioritizes protecting ordinary Americans and resolving banks in the least costly manner; why we should celebrate the return of true bank failures; and why we should resist the temptation to bail out uninsured depositors the next time a bigger bank fails.

That a small bank can fail, uninsured depositors can lose money, and a financial panic not ensue ought to give pause to those who defend every bailout as necessary to avoid a greater financial panic. At the same time, we need to have a frank discussion about why bank regulators were OK with a handful of people and businesses in small-town Oklahoma losing money in a bank but not the billionaires and venture capitalists who were bailed out under the guise of protecting small businesses trying to meet payroll when the Federal Reserve, FDIC, and Treasury Department opened the spigots for SVB. Consumer Financial Protection Bureau (CFPB) Director Chopra’s commentary is spot on in diagnosing this problem, but in my opinion, calls for the wrong solution of extending greater deposit insurance. Instead, we need to stop bailing out the wealthy and well-connected and instead operate a banking system in which not all deposits at the bank are insured.

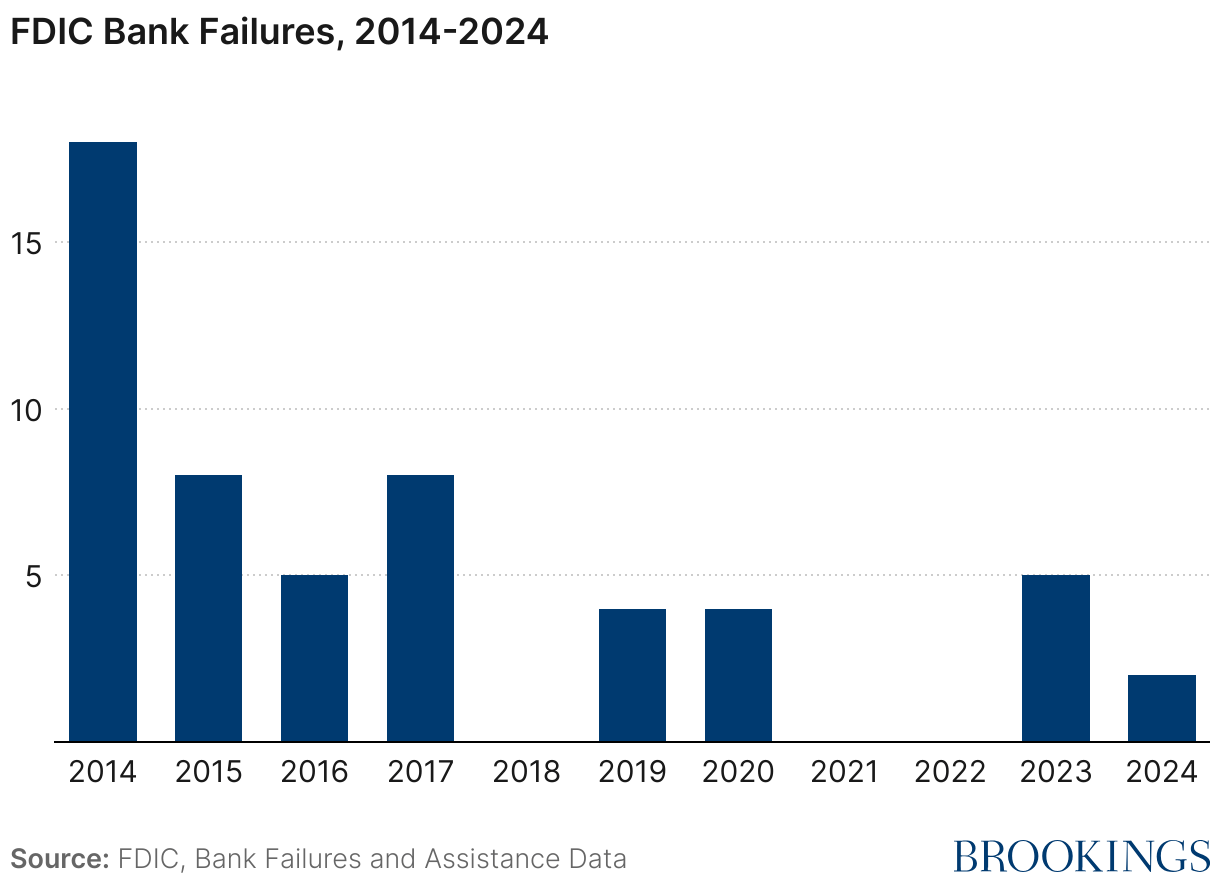

Banks failing is the norm. At least one bank failed every calendar year since the FDIC was created in 1933 until 2005. No bank failing in 2005 and 2006 was the signal that the financial system was dangerously unstable. After the great financial crisis, the norm returned. Fifty-four banks have failed since 2014 as shown in the chart below. It is a testament to the American financial system’s strength that banks can and do fail and we do not have a crisis.

What happened?

First the facts. Lindsay was a small national bank (about 1/200th the size of SVB) in a small town that once called itself “The broomcorn capital of the world.” The bank failed due to fraud. Fraud is a common cause of bank failures, as seen in a Kansas bank’s recent failure due to the CEO wiring millions to a crypto-scammer. Bank failures due to fraud are often proportionately expensive to resolve as compared to a bank that invested in poor-performing assets like SVB—assets can be recovered while fraud can mean the money is gone.

When a small bank fails in a small town, the options to find another bank to acquire the business are limited. The FDIC was able to offload about 20% of Lindsay’s assets and all of its insured deposits to nearby First Bank and Trust, another small community bank. This left just over $7 million in uninsured deposits from accounts with over $250,000. Those depositors may lose money.

The FDIC immediately offered half of that money to depositors, with the potential for more should the failed bank’s assets be worth more. The net loss to uninsured depositors should be no more than $3.5 million and quite possibly significantly less, or even nothing, depending on the eventual resolution of the bank’s assets.

Why we have this

Understanding why this failure, while tragic (my heart goes out to the victims of this bank fraud), is positive for the overall financial system requires going back to why the government-insured bank deposits: to protect the little guy. When FDR signed the law creating the FDIC and deposit insurance in the 1930s, the original limit was $2,500. Roosevelt’s logic is as sound today as it was in the Great Depression: Ordinary Americans need to know their money in the bank is safe, and only the Federal government can provide the ultimate guarantee.

Uncle Sam’s insurance is a massive gift to banks, but it is not free. Banks pay the premiums that fund deposit insurance. Some banks argue that deposit insurance is not taxpayer money, neglecting that the deposit insurance fund is part of the Federal government’s budget. Basic economics shows that banks pass deposit insurance costs on to customers, with some evidence that it is disproportionately passed to lower-income ones through fees.

The deposit insurance limit is not set on the basis of economics. The insurance limit was raised from $100,000 to $250,000 to build political support for the Troubled Asset Relief Program (TARP) bailout legislation after it originally failed a vote in the House of Representatives. Although the increase was written to be temporary (like TARP itself) it is hard to ever take back a government benefit, and the $250,000 limit was made permanent as part of the Dodd-Frank Act.

Checks and balances

The $250,000 limit fully insures over 99% of Americans’ bank accounts. The fortunate few who have more than $250,000 in a single bank have some risk if the bank fails. Those depositors, primarily wealthy individuals and businesses, have an incentive to keep an eye on their bank. After all, market forces are important. If bankers face no incentive from depositors to be prudent, more banks will fail and taxpayers will be on the hook again and again.

Charging bank regulators with a mandate preventing all banks from failing is a mistake for several reasons. First, it is impossible. Regulators are prone to error. SVB built up massive risk right under the Fed’s nose. Second, small banks are not examined regularly enough or closely enough to prevent fraud like what happened in Oklahoma and Kansas. And the cost of that level of continual monitoring likely exceeds the benefits, as fraudsters can lie to their regulators as well. Third, a system without bank failures is a perpetuity to existing holders of charters, a repudiation of basic capitalist principles of competition, which requires potential failure.

America’s banking system needs both appropriate prudential oversight and the market forces of businesses and wealthy people afraid that they will lose their uninsured money if they put it in the wrong bank. That is the system our laws have designed. The alternative of “a system of public guarantees for bank debts as far as the eye can see will mean only pain for our economy, our financial system and, perhaps most important, our politics,” as Peter Conti-Brown correctly argued.

Bank failure is a natural, normal, and healthy part of capitalism. America has over 4,000 banks and even more credit unions. Do we really want a world where these are perpetuities, incapable of failure? Regulators would constrain all sorts of positive innovations out of fear of failure. Or they would grow complacent, believing that they alone have designed a fool-proof system. A bank failed in every single year in modern American history up until 2005. Bank regulators were so proud of the lack of failure that they came to Congress crowing that the banking system had never been safer. Three years later it all collapsed.

A safe banking system must embrace failure. Poor decision-making must have consequences. Ordinary Americans should be protected, which our system does. The siren’s song to bail out the wealthy must be resisted. The FDIC did so in Oklahoma and guess what: There was no panic, no mass runs, no destabilizing systemic crisis.

The immoral inequity of bailing out billionaire venture capitalist depositors at SVB but not individuals and small businesses in Oklahoma was justified with the logic that having SVB fail would cause risk to the financial system, but letting these Oklahomans would not. This contradicts the promise of the Dodd-Frank Wall Street Reform Act, as President Obama said when he signed the law into place: “There will be no more tax-funded bailouts—period. If a large financial institution should ever fail, this reform gives us the ability to wind it down without endangering the broader economy.” Read carefully, President Obama could still be correct as the ability was given to regulators, but they chose not to use it.

I hope that instead of forgetting Lindsay Bank, financial reformers channel their outrage to prevent future bailouts of large financial institutions. I do not yet see enough strength to keep Odysseus tied to the mast the next time a larger bank fails, but I would hope that the memory of Lindsay—“broomcorn capital of the world”—Bank will be one tighter lash.

Author

-

Acknowledgements and disclosures

The Brookings Institution is financed through the support of a diverse array of foundations, corporations, governments, individuals, as well as an endowment. A list of donors can be found in our annual reports published online here. The findings, interpretations, and conclusions in this report are solely those of its author(s) and are not influenced by any donation.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Three cheers for normal bank failure

November 26, 2024