After two years of negotiations, the United Kingdom agreed to join the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) this past July, with final ratification expected in 2024. The U.K. will then join Australia, Brunei, Canada, Chile, Japan, Malaysia, Mexico, New Zealand, Peru, Singapore, and Vietnam by becoming the agreement’s first new and first non-Pacific member. This realizes a major goal of the U.K.’s “Indo-Pacific tilt,” a post-Brexit strategy to draw closer to the Indo-Pacific region. The marriage promises to be fruitful: British accession will generate varied benefits for the U.K. and also elevate the CPTPP’s role in economic cooperation at a challenging time.

The U.K.’s Indo-Pacific tilt

The conservative case for U.K. withdrawal from the European Union (EU) has long promised an agile foreign policy that would raise Britain’s economic and political profile across the world. The first post-Brexit Integrated Strategic Review 2021, the government’s principal foreign policy paper, set out a vision for a “Global Britain” that would reenergize historic relationships, partly through an “Indo-Pacific tilt” that prioritizes political and economic bonds with this region.

The tilt has since led to tangible political advances — including dialogue relations with the Association of Southeast Asian Nations and the defense agreement with Australia and the United States known as AUKUS — but its economic opportunities have proved critical in the aftermath of Brexit. Recent official and academic estimates find that withdrawal from the EU apparently lowered U.K. GDP by 2%-3% and depressed British trade; a new International Monetary Fund report argues for major reforms to revive business confidence and investment. In this setting, deeper trade and financial relations with Asia are particularly attractive.

To this end, the government took only 11 months after Brexit to ratify 33 comprehensive “continuity” agreements that replace EU free trade agreements (FTAs) that the U.K. would have lost otherwise, and to launch new bilateral FTAs with Japan (2021) and Australia and New Zealand (2023). The tilt — including joining the CPTPP — has now survived two changes in government (not so for the phrase “Global Britain”) and earned top billing in the Integrated Review Refresh 2023.

Membership in the CPTPP will add value to earlier trade initiatives and set a framework for future gains, but it will not offset the costs of leaving the EU, by far the U.K.’s most important trading partner. Government estimates of gains from the CPTPP suggest modest benefits: an increase in GDP of 2.0 billion pounds ($2.4 billion) or 0.06% of its expected level in 2040, and an expansion of bilateral trade with CPTPP countries of 4.9 billion pounds ($6.0 billion) or 3.9%. We recently re-estimated these effects with a new global trade model and found significantly larger gains in GDP of 7.0 billion pounds ($9.6 billion) or 0.23% of expected 2035 levels, still well below estimated Brexit losses. (The government’s estimates may not include the effects noted below and may make more conservative assumptions about reductions in non-tariff barriers, which are notoriously difficult to estimate.)

But context matters: Incremental gains from the CPTPP are small because they are partly preempted by recent U.K. bilateral agreements, which were necessary since accession to the group was uncertain and time-consuming. Current estimates also omit potential benefits from the future growth of the CPTPP.

For a better view of the policy’s overall effects, we also estimated the total U.K. benefits generated by the CPTPP and the overlapping U.K. bilateral agreements. These are more than twice as large as the incremental gains from the CPTPP alone. The latter gains are derived from new preferential trade agreements with Malaysia and Brunei, greater utilization of prior agreements, and more trade with rules of origin now shared by all 12 members. Japan particularly welcomed U.K. membership; in addition to economic gains, these large countries will share outsized influence on the agreement’s future.

The CPTPP’s opportunity

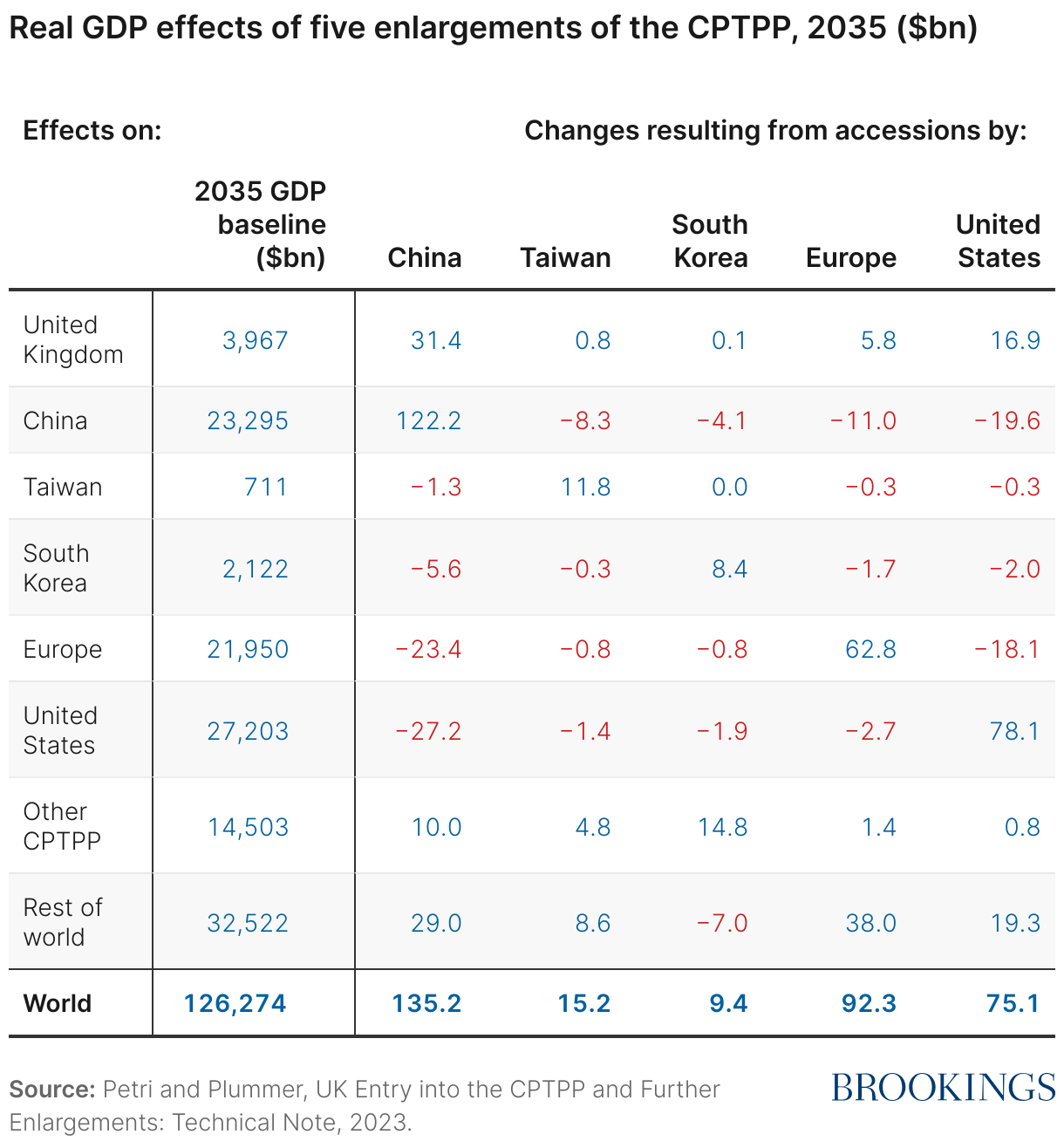

CPTPP members also benefit from U.K. accession — we estimate $4.8 billion or 0.03% of their total projected GDP — though these gains are modest for the reasons that U.K. estimates are small. But admitting new members could generate much larger gains all around. The smooth entry of the U.K. has opened the gate; the list of applicants already includes six economies — China, Taiwan, Ecuador, Costa Rica, Uruguay, and Ukraine — and many more have expressed interest.

We ran simulations of five further additions that would materially affect the CPTPP’s scale and geopolitics: China, Taiwan, South Korea, the European Union, and the United States (each is assumed to enter separately). The numbers are much bigger, as shown in the table below. Note that the partners were not selected for likelihood of entry but for overall policy interest.

China’s accession would generate the greatest benefits among the five scenarios given its deep trade linkages with the CPTPP region. They would be the largest not only for China but also for the world, the U.K., and current CPTPP members. Non-members would lose, including especially the EU and the United States. However, together the EU and United States would generate more gains than China while also imposing significant costs on China. Taiwan would benefit the most from accession in proportion to its GDP (1.7% of its annual real GDP) and Europe the least (0.3%).

Still, several scenarios are highly uncertain. China and Taiwan applied in September 2021, but despite promises of a response “within a reasonable period of time,” the accession process has yet to begin. There is no sign that a CPTPP accession working group is being formed to negotiate terms. Accession requires unanimous support and political considerations make such unanimity currently improbable. While senior U.K. officials have taken steps to reengage with China in recent weeks, the U.K. will not likely support a Chinese application now; the 2023 Integrated Review Refresh stresses the “epoch-defining challenge [China] poses to the international order.”

South Korea has the best chance of joining early. Its trade policies are aligned with those of the other members and improving relations with Japan has minimized overt opposition. The ball is in South Korea’s court: the government announced its intention to apply in April 2022 but has yet to file a formal application. So far, candidates have been considered in the order of application, but the CPTPP should adopt a flexible approach and consider South Korea quickly; its accession would be a boon and involve far fewer complications than other cases.

Finally, EU and U.S. entries are long shots. Neither lacks analytical support: Important EU think tanks and observers, including former Trade Commissioner Cecilia Malmström, strongly favor accession, and leading American experts and much of the business press would welcome U.S. membership. Official support is another matter. The EU Council’s 2021 EU Indo-Pacific Strategy does not mention the CPTPP; the commission’s plate is full and it would take great effort to marshal support for a new, multilateral trade initiative. In the United States, popular politics has turned sharply against trade agreements, including the CPTPP’s predecessor, the Trans-Pacific Partnership, which the United States once led and later abandoned.

Promising but uncertain prospects

The CPTPP is arguably the world’s leading comprehensive FTA and sets the pace for other regional agreements and global standards. The accession of the U.K. and the growing list of candidates make further enlargements likely. Incentives for membership are rising and early candidates will get better economic results and more say in the agreement’s evolving membership and content.

Members may also decide to update aging provisions, particularly on the digital economy, a topic of great interest to all five economies considered above. The Indo-Pacific Economic Framework, launched by the United States in lieu of trade agreements, indicates such interest focused on a similarly defined region. An implicit but energetic dialogue is underway.

Quick, far-reaching results cannot be expected. Even the Indo-Pacific tilt may not survive further changes in the U.K. government. Yet the dynamic that the CPTPP and the tilt established should endure, building a platform for wider cooperation.

Authors

Related Content

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

The UK’s Indo-Pacific tilt and the CPTPP’s prospects

October 6, 2023