In a previous blog, we shed some light on the outlook for the global consumer class and its recovery from COVID-19. In this blog, we want to put the United States’ decline in consumer spending in perspective and share new results from our models of sectoral decline and recovery across industries.

As the United States is looking toward 2021, businesses and consumers ask themselves: When will the economy recover after the greatest recession in a century? When will my industry recover?

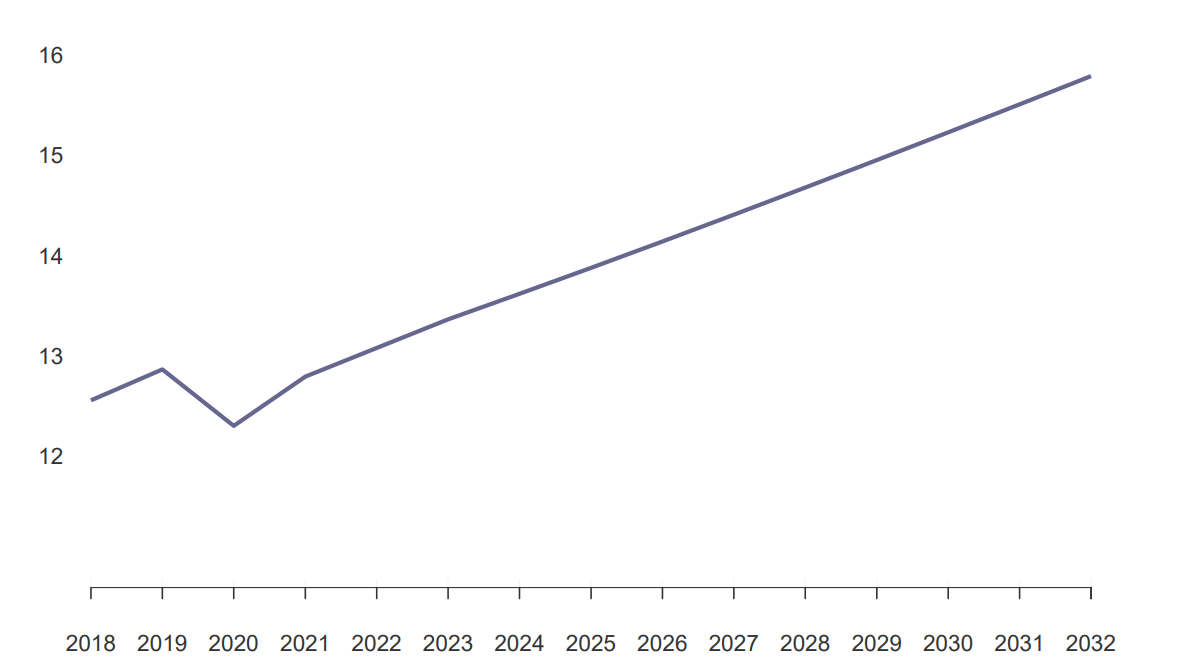

The United States is the world’s largest economy and the world’s largest consumer market. In 2020, American residents will spend around $12.5 trillion on durable and nondurable goods and services. This is more than half a trillion less than last year. It is likely to take until 2022 before personal consumption expenditure recovers to where it was in 2019, and, given population growth of 2.5 million people per year, only in 2023 will the average American spend the same amount as in 2019.

Figure 1. Total real US personal consumption expenditures will take until 2022 to exceed 2019 levels (in $ trillion)

Source: BEA for 2018, 2019; World Data Lab projections based on IMF and other forecasts for GDP growth

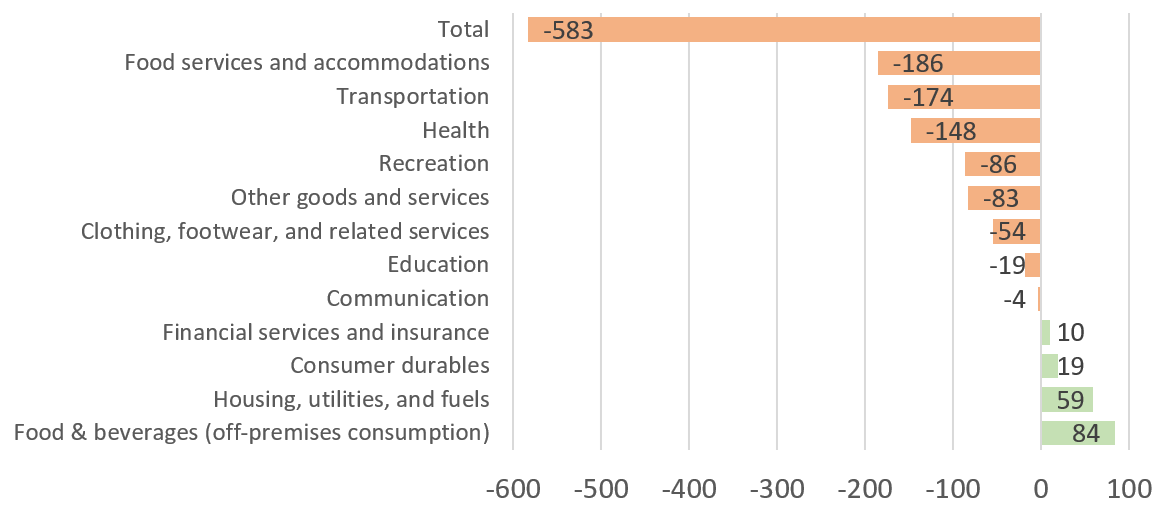

The fall in consumption, however, has not been even across sectors. As is now well known, the collapse in consumption has been heavily concentrated in services, while consumption of goods has had a very modest decline. Figure 2 summarizes the expected changes from 2019 to 2020.

Figure 2. Not all sectors are equal

Change in US sectoral spending patterns in 2020 (in $ billion)

Source: BEA and World Data Lab projections for Q4 2020

Sectors can be classified into three categories that cover both the impact of COVID-19 and the expected speed of recovery. The latter is derived from the modeling of sectoral trends over time.

- No negative impact. In some sectors such as food, housing, and financial services, consumers are expected to spend more in 2020 than they did in 2019. People still need to eat (and they now cook more at home than before) and manage their money. Specifically, consumer spending on food and beverages (purchased for off-premises consumption) sees a $84 billion increase from 2019 to 2020, the largest growth of any sector. Coming in at second, housing, utilities, and fuels increases by $59 billion. Consumer durables see an increase of $19 billion, while financial services and insurance increase by $10 billion.

- Severe contraction—fast recovery. For other aspects of the American economy the pandemic has resulted in severe contraction in consumer spending, with some sectors recovering faster than others. For example, food services and accommodations decrease by $186 billion, and transportation decreases by $174 billion. Despite COVID-19, health spending has been declining sharply, decreasing by $148 billion as many Americans delayed or skipped their visits to health professionals. Recreation decreases by $86 billion in 2020. We anticipate a faster recovery for these sectors, estimating sector spending to recover to pre-COVID sizes in 2023 or 2024.

- Severe contraction—slow recovery. Some sectors, on the other hand, may experience slower recoveries. Communication ($4 billion decrease), clothing ($54 billion decrease), education ($19 billion decrease), and other goods and services—such as personal care, social services, and labor organization dues ($83 billion decrease)—are not projected to recover to pre-COVID sizes until 2026 or later.

Figure 3. The COVID-19 impact across sectors is uneven

Source: World Data Lab estimates

These results are important to private investors, policymakers, as well as other stakeholders in consumer behavior. For private investors, the knowledge of how demand for their products will develop in the near and distant future is key in making informed decisions on handling the COVID-19 shock. For policymakers, the knowledge of COVID-19’s varying effects on different industries can help make stimulus more directed and thus more effective. Finally, the COVID-19 economic shock and the resulting shifts in consumer spending provide key insights into how sector-specific supply shocks can affect demand. These projections will be crucial in the determination of a path to economic recovery in years ahead.

Note: For questions on the underlying data models, please contact Thomas Mitterling ([email protected]).

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

The decline and recovery of consumer spending in the US

December 14, 2020