As policymakers search for equitable and efficient ways to address the large looming federal deficits, one option should top their list: closing the “Angel of Death” loophole. This refers to the fact that if a person dies holding assets with capital gains, the increase in the asset value escapes the income tax. In a new study (Gale, Hall, and Sabelhaus 2024), we show that taxing those unrealized capital gains upon an owner’s death can raise significant amounts of revenue, would be highly progressive, and would make the economy more efficient as well.

Background

A capital gain is the increase in the value of an asset over time. As such, a capital gain represents income to the asset’s owner. But the U.S. revenue code does not tax capital gains as they grow; it only taxes gains when the owner “realizes” them or sells the assets. The overwhelming majority of realized capital gains go to the highest-income households. In 2018, the top 1% of households ranked by income obtained 69% of realized long-term capital gains; the top 20% received 90% of the gains (Tax Policy Center 2018).

Taxation on realization (i.e., when the asset is sold) has two advantages. It provides the seller with liquidity (to pay the tax), and it provides an easy way to assign a value to the capital gain (based on the sale price). But it also creates problems. It creates a so-called “lock-in” effect: The seller is discouraged from selling the asset because the after-tax return to holding it rises (compared to the return on a fully taxable asset) the longer the asset is held. The lock-in effect is the source of much tax sheltering, since investors can accrue gains on a tax-deferred basis and finance those investments with tax-advantaged debt (given tax-deductible interest payments).

But these issues pale in comparison to the protected treatment of unrealized gains at death. The capital gains tax never touches unrealized gains on assets held until the owner’s death—the so-called “Angel of Death” loophole (Kinsley 1987). The basis (original cost) of an asset left to an heir is “stepped up” to the asset’s current value. This turns out to be quite a big deal. About 27% of all wealth and 41% of the wealth held by the top 1% takes the form of unrealized capital gains (Bricker et al. 2020). Basis step-up not only loses billions of dollars in revenue, but it also provides an enormous tax cut for the very wealthiest families, distorts behavior, and makes the lock-in effect even stronger.

Here’s an example. If your uncle bought an asset for $100 and sold it the day before he died at $300, he would owe capital gains tax on the $200 gain. If, instead, he held onto the asset until death and bequeathed it to you, you would receive the asset with a new basis of $300, not $100. If you eventually sell the asset for $350, your basis would be $300, and you would pay tax on only $50 of capital gains. It’s as if the $200 increase in value never occurred as far as the income tax is concerned: It never faces any tax.

The simplest solution to this problem would be to end basis step-up at death, which would result in “carryover basis.” The basis of an asset would not change when bequests are made. When the asset is later sold by an heir, the taxable basis would be the same as when the decedent owned it, set at the time of the decedent’s purchase of the asset. Under a carryover basis system, capital gains tax would continue to be owed when the gain is realized. In the example above, the realized capital gain would be $250 (the heir’s sale price of $350 minus the decedent’s basis of $100), rather than $50 under the current system.

This approach was enacted in 1976 but then repealed in 1980 before it ever went into effect. The tax code currently uses this approach for assets transferred inter vivos but not for bequests. The Congressional Budget Office (CBO) (2024) estimates that carrying over the basis at death starting in 2025 would raise almost $200 billion in revenue over the next 10 years.

Shifting to carryover basis discourages lock-in and tax shelters. It also maintains the practice of taxing capital gains at realization and thus retains the advantages related to investor liquidity and ease of valuation.

One potential argument against carryover basis is that a taxpayer may not always be able to document the basis of a long-held asset. To address this, a carryover basis regime should stipulate a “default basis” (say, 10% of the sale price). Taxpayers would be entitled to prove their basis is higher than the default. If they do not, the 10% default basis rule would apply, and the capital gain would be deemed to be 90% of the sale price.

Alternatively, unrealized gains could be taxed at death. Canada, for example, treats death as a realization event (Canada Revenue Agency 2024, OECD 2021) but does not have an estate or inheritance tax. To address liquidity issues, Canada exempts capital gains on principal residences and provides a lifetime deduction of CA$1 million for qualified farm and fishing property.

Relative to current law, taxing unrealized gains at death would raise significantly more revenue: CBO (2024) estimates that it would raise about $536 billion over the next 10 years. Other studies have generated a variety of generally similar estimates, adjusted for the period under consideration.1 Relative to carrying over the basis, taxing gains at death reduces the lock-in effect, reduces tax sheltering, makes the treatment of gifts and bequests consistent, and simplifies recordkeeping because individuals do not have to keep track of the original purchase price of inherited assets once the tax is paid.

However, taxing gains at death creates different challenges for investors compared to eliminating basis step-up and moving to carryover basis. After death, an investor’s estate would owe tax without receiving a payment for an asset and may find it difficult to pay the tax on time. This could be addressed either by people protecting their estate by buying life insurance to cover the capital gains tax liability and/or allowing estates to pay the tax over a period of time (e.g., five or ten years). A capital gains tax at death requires the potentially difficult valuation of some privately held and non-marketable assets, like family businesses or art, but the estate tax already requires that. If unrealized gains were taxed at death, the tax would need to be deducted from the estate value before applying the estate tax.

Methodology and Results

In our new work, we develop a methodology for estimating the revenue and distributional effects of taxing capital gains at death and apply the approach to data from the Survey of Consumer Finances (SCF). We examine several estate and inheritance tax reforms and a tax on unrealized gains at death at 23.8% (the top rate on realized capital gains in 2024).

To measure capital gains at death, we largely follow previous work using the SCF (Avery, Grodzicki, and Moore 2015). For real estate holdings, the SCF asks about current value and original purchase price. For stocks and mutual funds, the survey asks about current value and any unrealized gains on those holdings. For closely held businesses, the survey asks about current value (what the business would sell for) and the basis for tax purposes.

We find that unrealized capital gains account for more than one-third of all bequeathable wealth—and are 154% the size of annual gross domestic product (GDP) in 2021. Compared to total bequeathable wealth, unrealized gains wealth is distributed similarly by age but—within older age groups—the distribution is skewed towards the wealthy. In 2021, 70% of all unrealized capital gains were held by households where the head is 55 and older and 83% of the growth within that age group from 1997 to 2021 accrued to the top 10% of the bequeathable wealth distribution. Notably, the top 1% of households with heads aged 55 and older controlled unrealized gains wealth equal to 47% of GDP in 2021 and accounted for almost half of all unrealized gains wealth growth since 1997 as a share of the economy.

We model the revenue and distributional effects of a tax at death on unrealized capital gains at a flat rate of 23.8% (the top long-term capital gains rate). Both the revenue and distributional effects of any unrealized gains tax will depend crucially on the exempt amount, which determines the size of the base as well as the distribution of the tax burden.

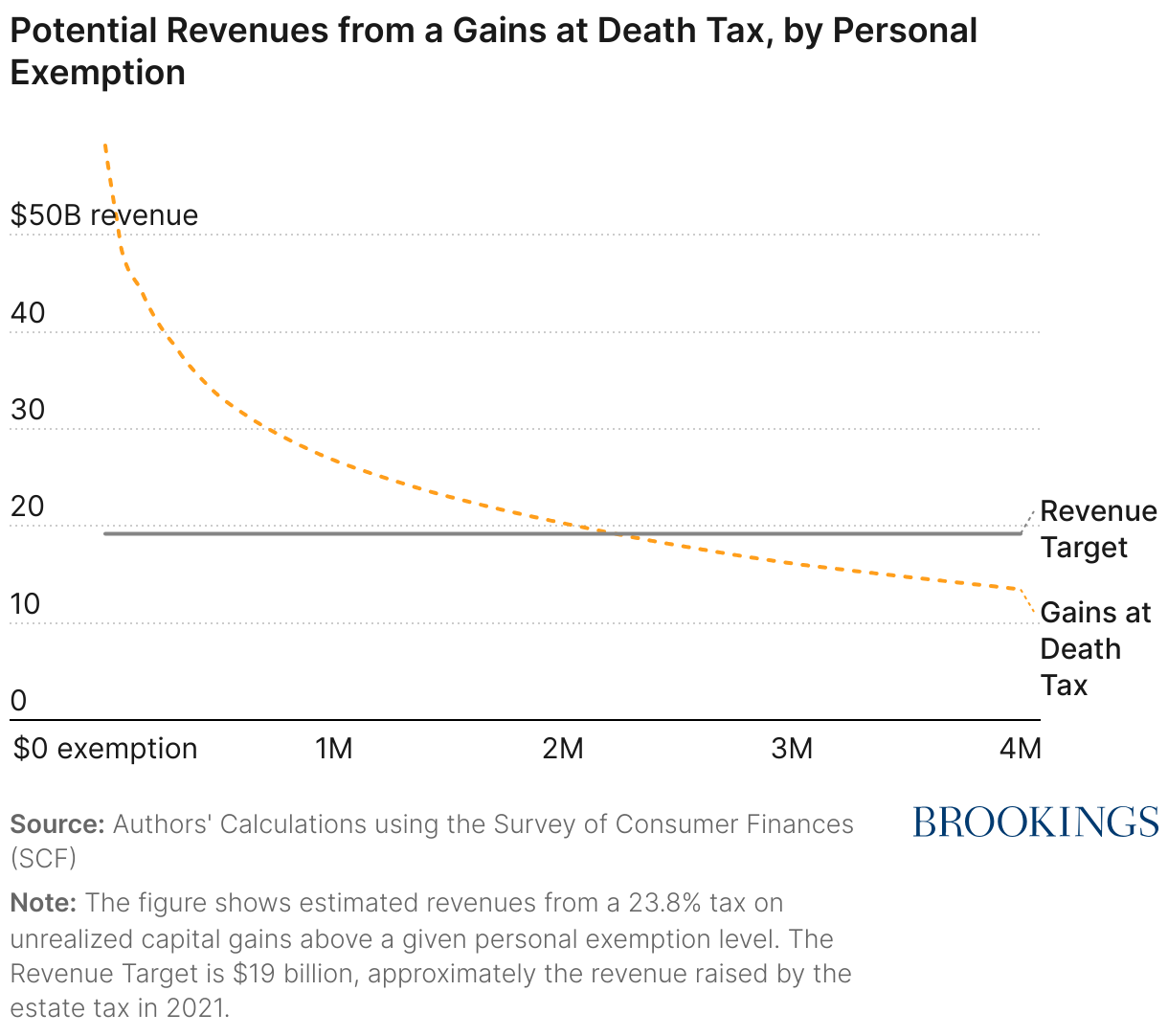

Figure 1 shows the potential revenues associated with different exempt amounts for the unrealized gains tax. The dark line at $19 billion shows the simulated revenue raised by the estate tax in 2021. An unrealized gains tax with an exempt amount of $2.22 million would have also raised $19 billion in revenue. With an exemption of $1 million, taxing unrealized gains at death would have raised about $27 billion in revenues in 2021, about 40% more than simulated revenues for the estate tax. With the elimination of any exempt amount, the tax could raise as much as $59 billion. That’s more than triple the current revenue raised by the estate tax.

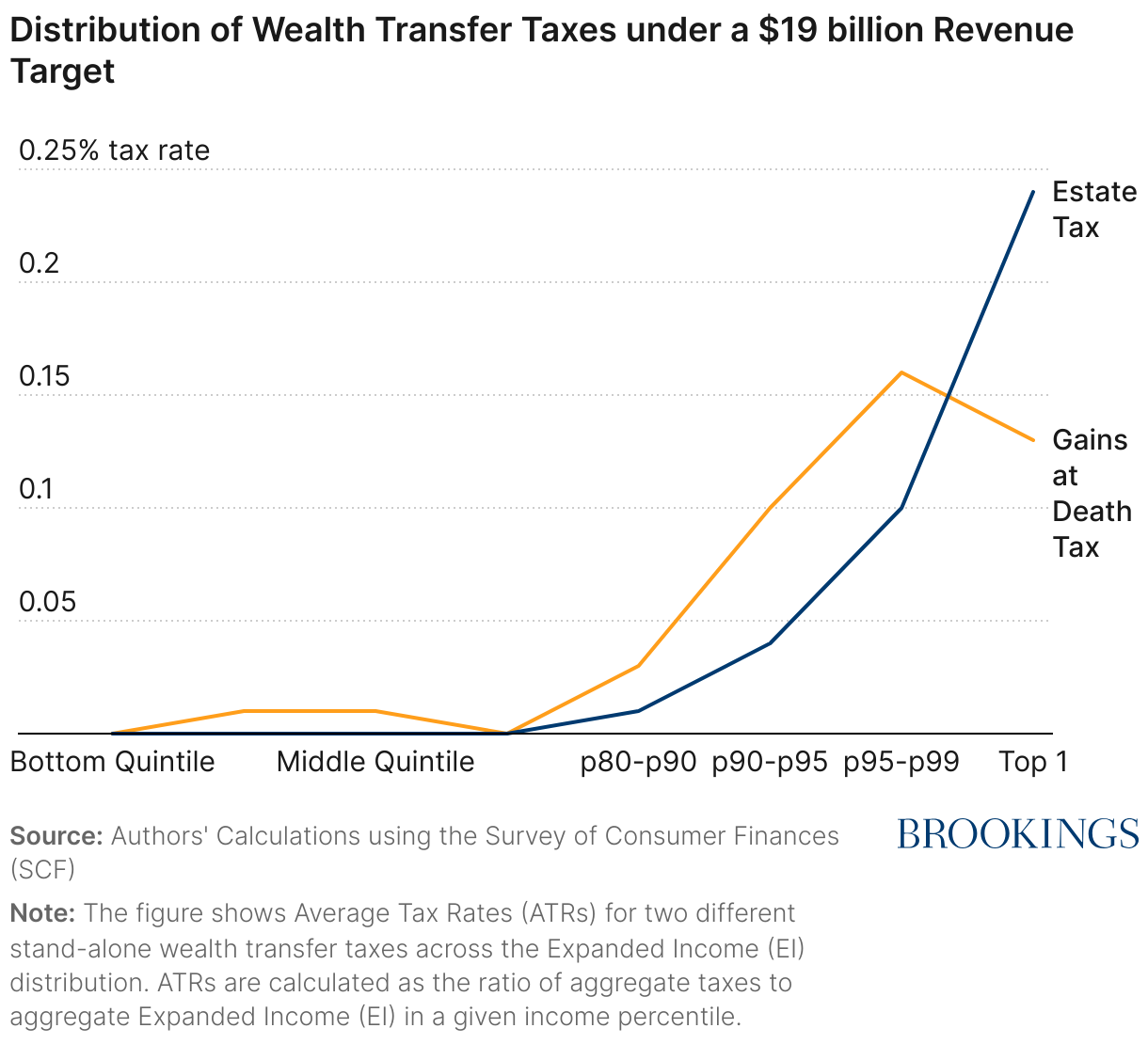

Even holding revenue constant and holding incidence assumptions constant (in this case, that the inheritor bears the burden of all wealth transfer taxes), distributional effects will vary across wealth transfer taxes because of differences in the tax base, the exempt amount, and the rate structure. We report average tax rates (the ratio of transfer taxes to income) and the share of tax payments by Expanded Income (EI) class, using both an inheritance-inclusive measure of EI and an inheritance-exclusive measure. The inheritance-inclusive measure better captures the ability to pay, while the inheritance-exclusive measure reports the economic status of inheritance recipients independent of their inheritance.

Figure 2 compares the progressivity of an estate tax and an unrealized gains tax using an inheritance-exclusive measure of EI. By construction, both taxes raise $19 billion under 2021 parameters. The estate tax is more progressive, imposing the greatest tax burden on the top 1% of the EI distribution, while the unrealized gains tax imposes a slightly higher burden on the 95th to 99th percentiles than the top 1%. That said, both taxes are extremely progressive: Neither impose a tax burden greater than 0.01% of aggregate EI on the bottom 80% of the distribution.

Conclusion

These estimates show that a stand-alone tax on unrealized gains at death can raise more revenue than the current estate tax. Taxing unrealized gains at death at a 23.8% rate is slightly less progressive than estate taxation (given the same revenue target), but it has important benefits such as closing the “Angel of Death” loophole and eliminating the associated lock-in effect. Policymakers should take these estimates into account as they evaluate wealth transfer tax options, as well as efforts to reduce budget deficits or improve government finances more generally.

Related Content

-

References

Avery, Robert B., Daniel J. Grodzicki, and Kevin B. Moore. 2015. “Death and Taxes: An Evaluation of the Impact of Prospective Policies for Taxing Wealth at the Time of Death.” National Tax Journal 68 (3).

Batchelder, Lily, and David Kamin. 2019. “Taxing the Rich: Issues and Options.” Available online at https://dx.doi.org/10.2139/ssrn.3452274

Bricker, Jesse, Laurie Goodman, Kevin B. Moore, and Alice Henriques Volz. 2020. “Wealth and Income Concentration in the SCF: 1989-2019.” Washington, D.C., Federal Reserve Board.

Canada Revenue Agency. 2024. “Capital Gains Tax Reporting for Deceased Individuals.” https://www.canada.ca/en/revenue-agency/services/tax/individuals/life-events/doing-taxes-someone-died/prepare-returns/report-income/capital-gains.html. Accessed 30 July 2024.

Congressional Budget Office (CBO). 2024. “The Long-Term Budget Outlook: 2024 to 2054.” Washington, D.C.: Congressional Budget Office.

Gale, William G., Oliver Hall, and John Sabelhaus. 2024. “A Preliminary Report on Taxing the Great Wealth Transfer: Revenue and Distributional Effects of Taxes on Estates, Inheritances, and Unrealized Capital Gains at Death.” Brookings Institution.

Gordon, Robert, David Joulfaian, and James Poterba. 2016. “Revenue and Incentive Effects of Basis Step-Up at Death: Lessons from the 2010 `Voluntary’ Estate Tax Regime.” American Economic Review Papers and Proceedings 106 (5): 662-667.

Kinsley, Michael. 1987. “The ‘Angel of Death’ Loophole.” The Washington Post. 25 June 1987.

Organization for Economic Cooperation and Development (OECD). 2021. “Inheritance, Estate, and Gift Tax Design in OECD Countries.” Paris: OECD.

Poterba, James M., and Scott Weisbenner. 2001. “The Distributional Burden of Taxing Estates and Unrealized Capital Gains at the Time of Death.” in Rethinking Estate and Gift Taxation, eds. William G Gale, James R. Hines Jr., and Joel Slemrod. Washington, D.C.: Brookings Institution Press.

Tax Policy Center. 2018. “Table t18-0231 – Distribution of Long-Term Capital Gains and Qualified Dividends by Expanded Cash Income Percentile, 2018.” Washington, D.C.: Tax Policy Center.

Authors

-

Acknowledgements and disclosures

The Brookings Institution is financed through the support of a diverse array of foundations, corporations, governments, individuals, as well as an endowment. A list of donors can be found in our annual reports published online here. The findings, interpretations, and conclusions in this report are solely those of its author(s) and are not influenced by any donation.

-

Footnotes

- See, for example, Avery, Grodzicki, and Moore (2015), Batchelder and Kamin (2019), Gordon, Joulfaian, and Poterba (2016) and Poterba and Weisbenner (2001).

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).