Editor’s Note: Sarah Binder writes on the failed candidacy of Larry Summers to lead the Federal Reserve.

Larry Summers to President Obama (2013):

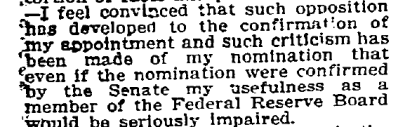

Thomas Jones to President Wilson (1914):

We have to reach back nearly a century to find a case roughly analogous to the failed candidacy of Larry Summers to lead the Federal Reserve. Then, Progressives turned on several of Woodrow Wilson’s picks to serve on the newly created Federal Reserve Board, including Thomas Jones (who as president of International Harvester drew Progressive ire for his company’s allegedly corrupt practices). After the requisite exchange of letters between Wilson and Jones, Wilson promptly nominated a more acceptable business executive (Frederic Delano), who the Senate easily confirmed.

There’s been ample written already on Summers’ withdrawal, including Binyamin Appelbaum’s NYT piece and Neil Irwin’s Wonkblog coverage. Some additional thoughts to put the Summers pseudo-nomination in perspective:

First, nearly three months have elapsed since the president suggested to Charlie Rose that he would not reappoint Ben Bernanke. The extended flight of the Summers trial balloon lasted too long. Some argue that the intervening Syria debacle emboldened the left and helped to throw a roadblock in Summers’ path to confirmation. My hunch is that the Syria diversion mattered because it sucked all the wind out of White House efforts to recruit Senate support for Summers. More importantly, by never actually nominating Summers, the White House left his opponents in control of the confirmation contest. Opposition groups on the left (and supportive, list-prone economists) organized their troops for battle against Summers and in defense of Janet Yellen. The White House couldn’t publicly counter-lobby because they had no nominee to defend. A new Catch-22: The White House refused to nominate until confirmation seemed plausible, but failure to nominate helped to put confirmation out of reach.

Second, Summers’ withdrawal helps us arbitrate between competing accounts of advice and consent. High rates of presidential success in securing confirmation of their executive branch appointees might suggest that senators (and the president’s partisans in particular) defer to presidential choices. Alternatively, presidents might see their preferred candidates confirmed so regularly because they factor in the likelihood of confirmation before making their choices known. (By leaking his preference for Summers so early in the game, Obama has saved future scholars trips to his archives to ferret out the short list.) The Summers case obviously marshals against any semblance of senatorial deference to the president.

Third, the last blow to Summers came from Senator Jon Tester, a centrist red state Democrat from Montana, who sits on the Senate Banking Committee. Two elements of Tester’s Friday afternoon statement opposing Summers are worth noting. First, the opposition to Summers went beyond coastal liberals who disagreed with his past stance on deregulation; Tester’s opposition reminds us of historical tension between the Main Street and Wall Street wings of the Democratic Party. Second, the close party ratio on the Banking panel places enormous leverage in the hands of its far left Democrats, including Senators Jeff Merkley, Elizabeth Warren, and Sherrod Brown. I suspect we’ll continue to hear from the liberal wing of the party, which remains committed to greater restraints on the financial sector.

Fourth, once the Fed has a newly confirmed chair, it’s an open question whether we’ll see such conflict every time a vacancy occurs. Given Congress’s counter-cyclical attention to the Fed—rising as the economy sours, falling as it improves—the intensity over the fight about the Fed reflects in part a still recovering economy. A robust economy in the future might return Congressional debate about the Fed to a much lower pitch.

What happens next? Consider the aftermath of three failed (albeit each very different) confirmation battles: Reagan’s loss of Robert Bork for the Supreme Court in 1987, George W. Bush’s inability to get Harriet Miers confirmed in 2005, and Wilson’s failed Thomas Jones nomination in 1914. In each case, the president turned next to a safe (i.e. easily confirmable) nominee, seemingly eager to cut his losses and regain lost ground. For Obama, we might conclude that he will nominate Yellen (ending the yellin’ about the Fed and returning Washington’s focus to fiscal policy fights with the GOP). Still, it’s possible that the calculations that led Obama to float Summers in the first place might still guide the president’s thinking. Ultimately, whoever the president chooses will be compared not only to Summers but also to Yellen. If he doesn’t break the glass ceiling by choosing Yellen, the president will still be asked the question: “Why not?”

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Op-edSummers’ Fall

September 16, 2013