Electronic money, or e-money, emerged in the countries of the West African Economic and Monetary Union (WAEMU) following the adoption, in 2006, of a Central Bank Instruction establishing a flexible regulatory framework aimed at encouraging e-money business. The activity expanded in 2009 with the involvement of telecommunications operators in the provision of mobile telephone-based financial services, which increased the number of users and the volume of transactions.

A growing business

At the end of September 2015, 22 million people, or nearly a quarter of the people in the union, subscribed to financial services via mobile phone. Approximately 30 percent of those subscribers carried out at least one transaction per 90-day period.

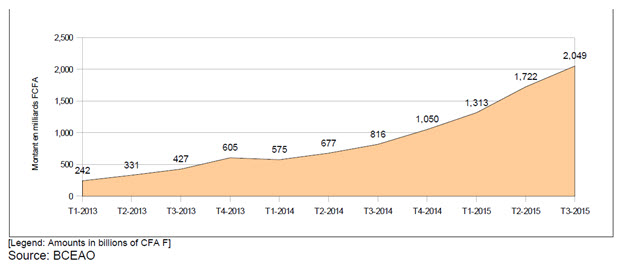

Some 500 million transactions took place over the first nine months of 2015. The cumulative value of the transactions was 5 trillion CFA francs ($8.5 billion) by the end of September 2015, a growth of 142 percent from September 2014. Between September 2013 and September 2014, this value grew from CFA 1 trillion to CFA 2.068 trillion, an increase of 107 percent.

The mobile phone financial services distribution network followed a similar upward trend, rising from 93,621 points of services in 2014 to more than 132,658 at the end of September 2015.

Figure 1. Trends in the value of transactions

The socioeconomic environment in the union goes a long way to explaining the success of mobile telephone payment services. Indeed, this method of providing money transfer or payment services is particularly well suited to people who lack access to the mainstream banking system, and also affords non-bank institutions the opportunity to offer users non-cash money against cash deposits, which can then be used for a variety of financial transactions.

The growing involvement of telecommunications operators

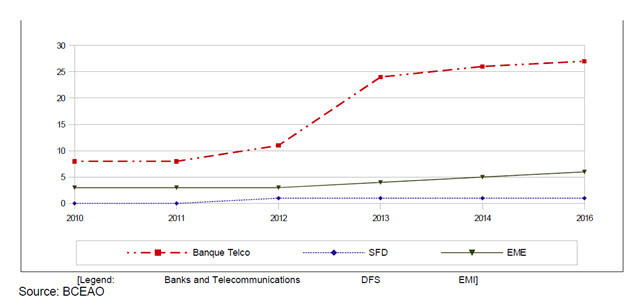

The market is increasingly dominated by partnerships between banks and telecommunications operators, which represented 25 of the 33 licensed or authorized e-money issuers at the end of December 2015. In the framework of this model, known as the bank model, the bank has responsibility for issuing the e-money.

The other seven non-bank institutions, under the non-bank model, are authorized to issue electronic money as “Electronic Money Institutions” (EMIs) [1].

In WAEMU, e-money issuers are supported by a regulatory framework that was revised in 2015 to ensure increased security and quality of payment services backed by electronic money.

Figure 2. E-money issuers in WAEMU

Note: DFS denotes microfinance institutions.

A revised regulatory framework

With the expansion of mobile phone financial services and the growing involvement of telecommunications operators, the Central Bank has revised its regulatory framework with the aim of enhancing the security and quality of payment services backed by electronic money. The most salient improvements must focus on:

- Increasing issuer accountability by clarifying users’ roles in partnerships with technical service providers. With this goal in mind, the activities of technical service providers have been restricted to technical processing or the distribution of e-money under the responsibility of the issuer. In addition, issuers are responsible for the integrity, reliability, security, confidentiality, and traceability of all transactions carried out by all of their distributors; Stimulating competition through transparent pricing with an obligation for issuers to publish their rates;

- Specific requirements in terms of governance and internal and external audits for electronic money institutions, standards of integrity on the part of the management, professional secrecy and regular infrastructure audits;

- Increased protection for bearers of electronic money, including keeping funds in dedicated accounts, requiring a constant equivalence between the amount of e-money and the balances in the dedicated accounts, and mandatory creation of a mechanism to take in and deal with complaints by bearers of electronic money;

- Reinforcement of the supervisory mechanism by reducing deadlines for reporting on issuers’ activities to the Central Bank and adopting sanctions for violations of regulatory provisions.

Provision of mobile-phone-based financial services

Mobile-phone-based financial services provided in WAEMU include three categories of services, namely services involving the use of cash (banknotes and coins), e-money services, and so-called “second generation” services.

The first type of service essentially involves deposits of cash or refilling of electronic wallets, as well as withdrawals. This type of service represents 24 percent of user transactions. Cash deposits predominate; they allow customers to provision their electronic money accounts.

Seventy-six percent of the funds deposited into e-money accounts are used, above all, for purchases of telephone credit, payment of bills, person-to-person money transfers, and money transfers from individuals to businesses and from individuals to government agencies. The main payment services found in WAEMU pertain to payment of water or electricity bills, payment of satellite television subscriptions, and purchases of goods in supermarkets or fuel at service stations.

Payments of taxes or income taxes to government agencies and payments of micro-loan installments are also made through mobile phone financial services, but are much less common.

So-called “second generation” services, namely micro-insurance, micro-savings, and micro-credit, are currently emerging in WAEMU. Their development could be an opportunity to provide access to the banking system for the users of the services.

Finally, interoperability is just beginning to be implemented based on bilateral agreements between stakeholders, particularly with a view to offering cross-border payment services between member states of the union.

Challenges

A review of the development of mobile phone financial services in WAEMU reveals some obstacles to the rapid development of this type of financial service within WAEMU. They include:

- a low number of active users, due to the high cost of the services;

- the fact that the services are not well known due to inadequate financial education;

- the low rate of digitization of government agencies’ payment systems; and

- insufficient partnerships between bank and non-bank issuers with a view to developing a more inclusive range of “second-generation” services.

In collaboration with all stakeholders, the Central Bank has developed a financial inclusion strategy to continuously improve, access to and use of diverse, tailored and affordable financial services. The implementation of these actions as described in the Central Bank of West African States (BCEAO) financial inclusion strategy should support the challenges mentioned above.

[1] EMI: any legal entity, other than a bank, financial payment institution, or decentralized financial system, that is authorized to issue payment instruments in the form of electronic money and whose business activities are restricted to electronic money issuing and distribution.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Mobile financial services are making headway in WAEMU

June 14, 2016