As wildfires scorch the west, and multiple hurricanes threaten the Atlantic coasts, it is clear that even amidst a global pandemic the problem of climate change requires attention. One barrier to action has been the inability to get the financial markets fully engaged. They move trillions of dollars, and if moved in the right ways they could be a powerful force for good.

In 2015, Mark Carney, then head of England’s central bank, rattled those markets (and the op-ed pages even more) by warning that global equities markets were poised for a major shock when governments started to regulate emissions of gases that contributed to global warming. The valuation of oil and gas companies, like many others, would be shattered as governments forced a transition away from big polluting activities, he warned. This “transition risk,” as it is known, wouldn’t just cause financial instability, but those impacts might also reverberate through the real economy.

What if Mark Carney’s warnings about market instability were right, but the real logic for financial stress was different? The real problem that climate change poses for the markets isn’t “transition risk,” but the mounting physical harms that will come in a warming world. Transition risk hasn’t much materialized because most governments aren’t doing much to impose deep cuts on emissions. With that failure, the world is headed for a lot more climate change — more droughts, more and stronger storms, wildfires, and many other hazards.

In new Brookings research, we are investigating the hypothesis that the physical risks of climate change are the real worry for financial instability. Over the next few months we will be digging deeper, working with partners who model catastrophic risks like hurricanes, studying the vulnerability of infrastructure, and analyzing how government policy perniciously invites investors to do risky things like build houses in the paths of hurricanes. This effort comes at a time when many other groups are worried about the same questions of financial instability (for example here and here).

This first paper looks at a foundational question: What do the markets already know about climate risk? Our answers come from looking at what firms and governments disclose to investors. More disclosure leads to better-informed investors and raises the odds that valuations will reflect real risks and capital will flow to the right places — for instance, ensuring that retirements funds are invested safely, and that infrastructure is built with environmental resiliency in mind.

We focus on the U.S. and on two classes of investments in particular: public equities (that is, stocks) and municipal debt. There’s a lot more climate disclosure information about equities — thanks in part to work from groups like Ceres that are putting a spotlight on these important investments. By contrast, very little is known about what the municipal debt markets know about climate change. That should be deeply worrying because municipalities are on the front lines of the physical impacts of climate change, such as the communities in California that have been eliminated by wildfires. Firms whose stocks trade can move around as needed and adjust. But you can’t move a city. Because municipalities are on the front lines, we start there.

The risks to municipalities

The municipal debt market stands at $3.9 trillion, and is a primary way that cities fund their basic infrastructure, such as toll roads, hospitals, and water systems. Understanding the exposures of municipalities requires estimating how climate change will hurt these assets, which is hard to do because most climate models run at very coarse geographical resolution. A few private companies are now doing this kind of analysis (for example, flagship firms such as AIR, and newer startups such as 427 and risQ). For analysts like us, who work in the public domain, notably helpful is academic research that is now delivering this information, such as the Climate Impact Lab (CIL).

A first fix on what’s happening comes from crossing information about the level of harm each community faces with what those same communities disclose when they borrow money from the market. Figure 1 shows the result for 590 U.S. counties, and nearly 1,500 municipal bonds randomly sampled from the Municipal Securities Rulemaking Boards (MSRB’s) EMMA website.

Figure 1

No matter how we slice the data — and we’ve looked at it lots of ways — there is no relationship between what the scientists know about climate risk and what these municipalities tell the markets about the risks they face. The data on the figure are a cloud.

This is concerning because most people, when they think about climate risks, they imagine a catastrophic event sweeping through town — like a hurricane or a flood. The big dangers that face communities, however, seem to be chronic events like repeated floods and heat stress that empty out communities, erode the tax base, and make it harder for municipalities to invest in the long term.

The risks to companies

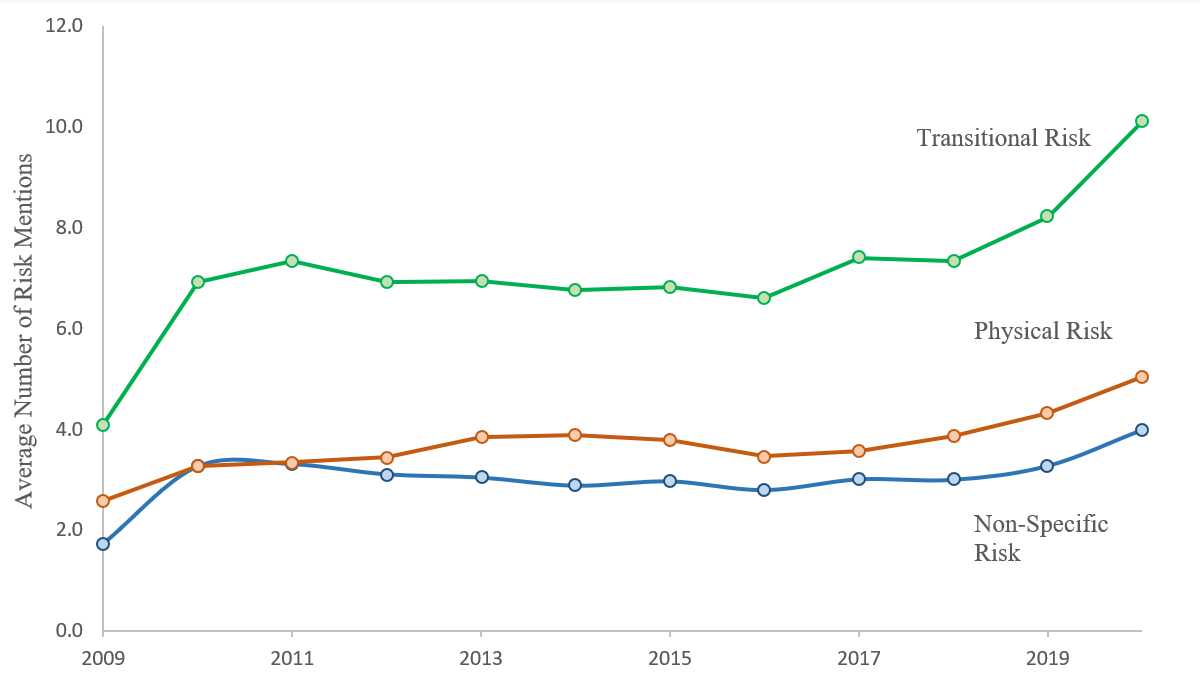

Turning to equities, the picture is a lot better. As shown in Figure 2 — which tracks average mentions of climate change risks by the 3,000 most important traded stocks — disclosure has gone way up since 2009. Today, about 60% of companies do say something about climate change in their public 10-k filings.

Figure 2

There’s a big bias in the picture: Disclosure about transition risk (what Mark Carney was worried about, in the main) has gone up a lot. But American corporate leaders say a lot less about their exposure to physical risk. Put differently, firms are getting good at telling investors what they already know — for example, about emissions and about the risks that government will regulate aggressively. But they say little about the place where the market is still flying blind: the physical risks of climate change.

What to do?

Fixing the disclosure problem isn’t easy, and better disclosure by itself won’t assure that our societies are better prepared for the large and growing impacts of a changing climate. But there is an urgent need to rebalance the disclosure debate toward physical risks. Even if governments start cutting emissions quickly, warming is already accelerating and the odds of severe impacts are rising quickly. Organizations like the California Coastal Commission are updating their planning systems with extreme sea level rise scenarios, for example. We must brace ourselves for a lot of climate change, and if we are unlucky those changes will be quite severe.

Some solutions lie with better rules on required disclosure — rules that, today, are mostly to issuers to interpret on their own and that stem from uneven application of existing rules such as at the Securities and Exchange Commission. In addition to better rules, many issuers need help seeing good models — especially in the municipal debt market. Municipalities that have big staffs working on climate-related topics can help by demonstrating practical methods for better disclosure. The costs for serious analysis of exposures remain high, and some of the key tools are hard to use. Fixing that problem will take time, but a place to start is with audits of public infrastructure (so that assets at risk and possible damages are easier to tabulate) and making publicly available climate hazard maps at a granular level. The credit ratings agencies are quickly learning a lot about climate risks and more transparency around those methods — while still protecting proprietary tools — would help catalyze a fuller public debate about what’s at stake.

Central to the problem of disclosure are two factors that quantitative analysts rarely talk much about. One is imagination: Part of the failure to reveal more information about physical risks of climate change is that market players have yet to see regular evidence of all the ways in which climate change will cause harm. Many of the harms that are easiest to imagine (e.g., hurricanes) may prove less threatening than those with longer term harmful impacts (e.g., heat stress). The other is policy signals that are still pointed in the wrong direction — creating a “moral hazard” that encourages people to invest in ways that invite climate damages because they believe that government (such as through the Federal Emergency Management Agency, FEMA) will bail them out.

Climate change is a topic that inspires emotive responses. That emotion helps explain ongoing gridlock in policy and why grappling with the impacts of climate change has become so much more urgent over the last decade. Getting this wrong has big implications for the financial markets, 401(k) retirement accounts, and the ability of communities to raise funds for schools and hospitals — problems everyone cares about, even when they are divided on so much else.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Markets are flying blind on climate change

September 16, 2020