This article is part of the Brookings Center for Sustainable Development compendium “Innovations in public finance: A new fiscal paradigm for gender equality, climate adaptation, and care.” To learn more about the compendium’s chapters, cross-cutting themes, and policy-relevant insights, see the “Introduction: Six themes and key recommendations for embedding gender equality, care, and climate in fiscal policy.”

Introduction

In Colombia, gender gaps persist across various dimensions, including labor force participation, unemployment, informal employment, unpaid care work, and political representation. These disparities underscore the need for fiscal policies that go beyond the notion of neutrality on the tax side as well as more aggressive use of public expenditures to address structural gender inequalities.1 Effective gender-responsive policy must align with both revenue and spending. While fair taxation helps prevent deepening disparities, targeted public investment—especially in universal care services and care infrastructure—can directly promote gender equality.

This brief explores how Colombia can use newly available tax data and macroeconomic modeling to design fiscal policies that enhance the enabling environment for gender equality and women’s empowerment (hereafter, we use the term gender-responsive fiscal policy). It begins by analyzing newly accessible tax data to assess the distribution of income, wealth, and tax burdens by sex, revealing expected patterns—like women’s underrepresentation in top income percentiles—and surprising ones, such as a higher female presence in top wealth brackets, likely due to intra-household tax planning. While tax systems appear neutral in their treatment of men and women at similar income levels, neutrality does not guarantee equality. In reality, men and women face markedly different economic conditions.

The report then discusses Colombia’s gender budgeting efforts to implement the country’s strong legal framework for gender equality, including the establishment of a public system to support caregiving. Given the lack of budget transparency and sex-disaggregated administrative data on expenditure, Colombia’s gender budget is not as effective as it could be. As an alternative, we report the results of a computable general equilibrium model that incorporates unpaid care work to show that investing in public childcare infrastructure not only improves gender equality and women’s labor force participation but is a high-return strategy to boost national productivity and revenue generation. Based on this analysis, we argue that expenditure—not taxation—is a more effective fiscal policy lever for improving outcomes for men and women.

What administrative tax data tell us about taxation of women’s income and wealth in Colombia

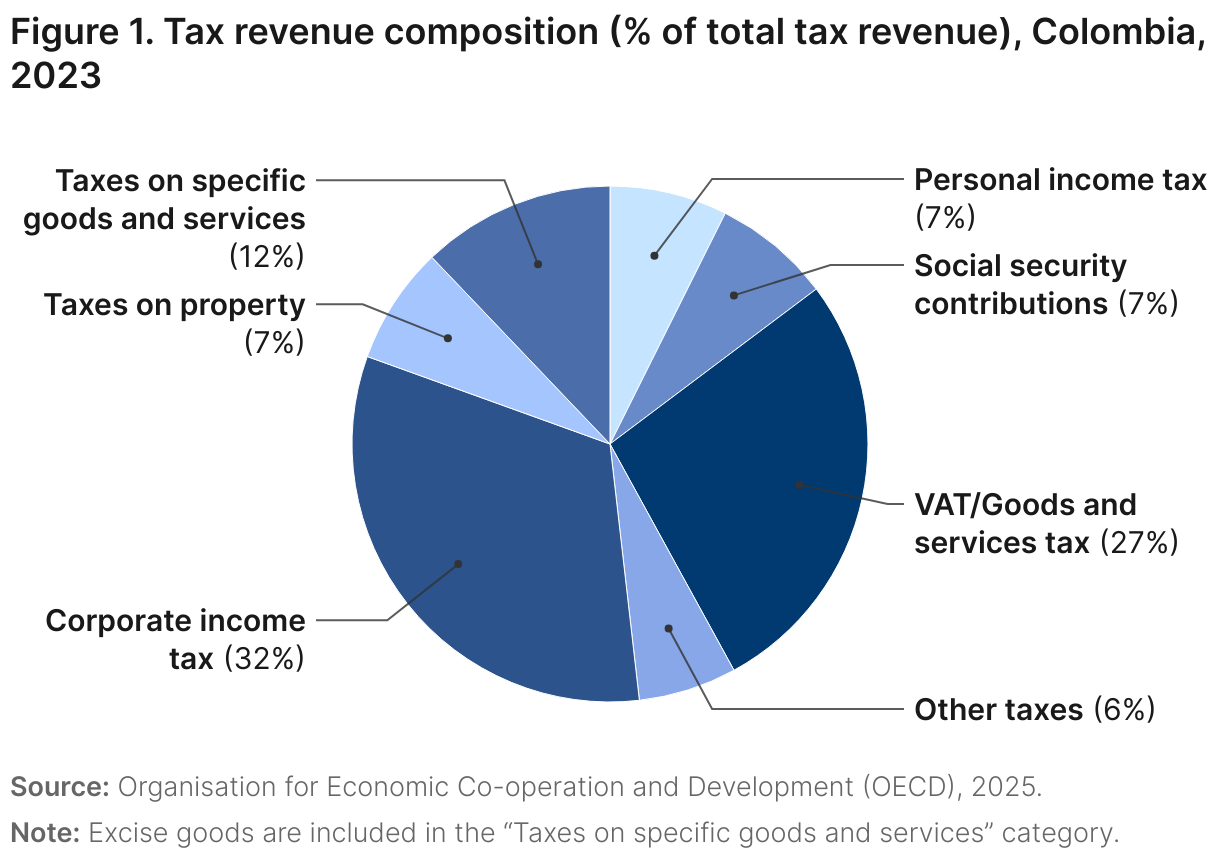

In 2023, Colombia’s tax-to-gross domestic product (GDP) ratio rose to 22.2%, up from 19.7% in 2022 (see Figure 1).2 Corporate income tax (CIT) accounted for the largest share of revenue in 2023 (32.3% of total tax revenue) followed by the value-added tax (VAT) (27.3% of the total tax revenue). In 2022, these two were also the largest shares of revenue, but VAT was followed by CIT (31.8% and 25.4% respectively). This tax composition reflects a system that leans heavily on business and consumption taxes, with personal income and wealth taxes playing a comparatively smaller role.3

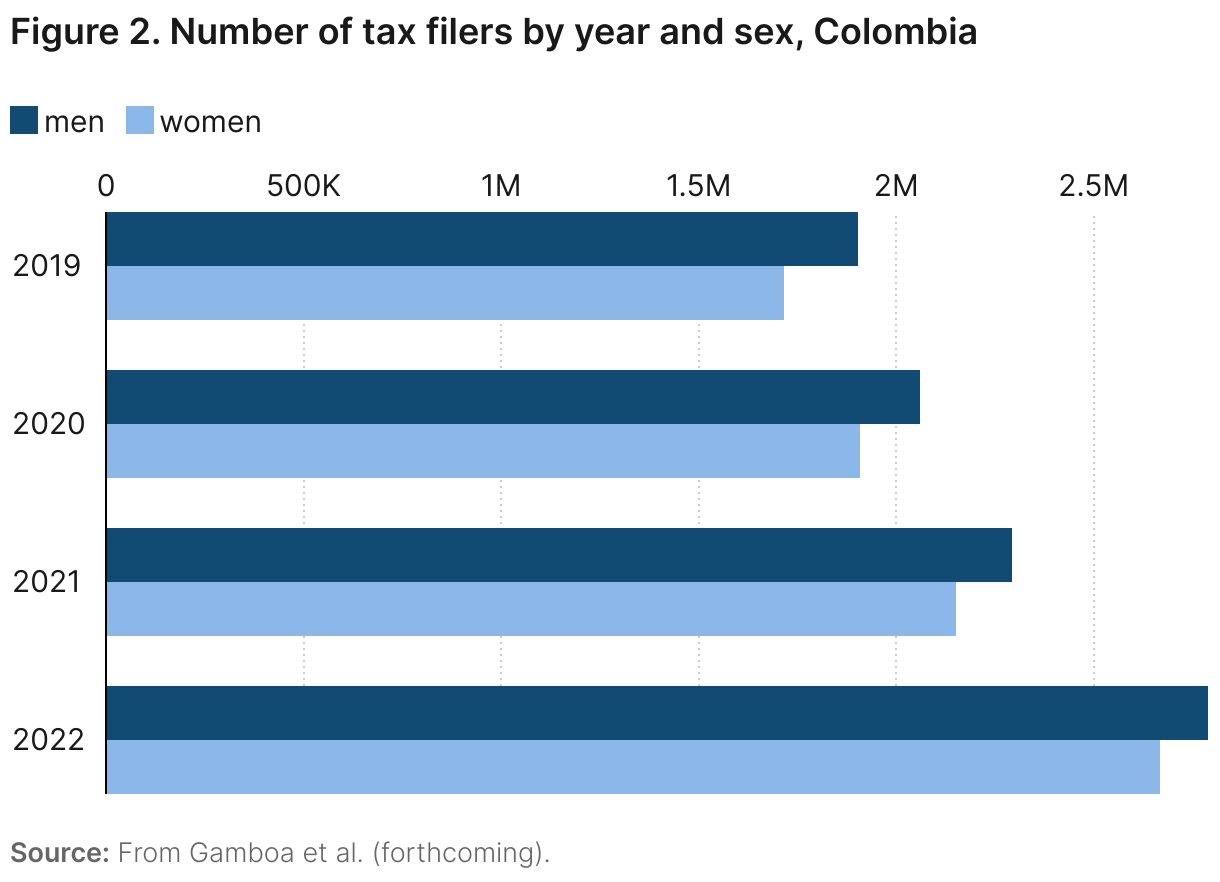

As part of a broader national effort to mainstream gender across all branches of government, Colombia introduced regulations requiring the collection of sex-disaggregated data, which included the National Tax and Customs Administration (Dirección de Impuestos y Aduanas Nacionales—DIAN). In response, DIAN began collecting information on taxpayer sex—a technically complex and initially resource-intensive process that has since become standard practice. Led by DIAN’s Unit for Differential Focus and Gender (PLURAL), this initiative revealed that from 2019 to 2022, the share of women among tax filers rose to just under 49% (see Figure 2). However, disparities remain—particularly among older taxpayers, where women tend to earn and own less. These findings could serve as a valuable tool for the Ministry of Equality, helping to support gender-sensitive tax incidence analysis, for instance, by highlighting income differences that shape how men and women are affected by the tax system.4

While the system relies largely on indirect and corporate taxes, understanding who bears the personal tax burden could be informative. In 2021, Colombia had nearly 37 million adults, but only about 3.1 million—just 8.4%—filed an income tax return, primarily due to high filing thresholds relative to average incomes. Among those who did file, marked gender disparities emerge: Only 42.7% of the top 5% of income earners were women. This share declines steadily at higher income levels—35.3% in the top 1%, 28.2% in the top 0.1%, and just 23.8% in the top 0.01% of income earners.5

Making disaggregated administrative tax data available to researchers has yielded key insights on issues such as the ways in which socioeconomic status is transmitted from parents to children,6 the effects of access to educational and other opportunities on income,7 the distribution of income and wealth at the top of the distribution,8 and the progressivity of tax systems.9 Even though tax data are sensitive, and access is usually highly restricted due to privacy concerns, it is important for policymakers to work alongside researchers to improve knowledge of the impacts of different types of taxes and the system as a whole on individuals and population groups. This enables tax systems to align more closely with policy goals, as well as to learn about the effects of non-tax policy on the key economic variables that are contained in administrative tax data.

Starting in August 2022, DIAN widened access to external researchers working in tandem with DIAN research staff. In keeping with the mandate from the 2022 tax reform bill approved by Congress, one of the first priorities was to conduct research on the way the tax burden was distributed by sex.10 Because tax returns only started asking the taxpayer’s sex in fiscal year 2022, taxpayer sex for fiscal year 2021 was obtained by matching tax returns with third-party data and using a machine-learning algorithm to infer the taxpayer’s sex where needed. The results of this analysis, reported by DIAN (2024) and in work by Gamboa, Iriondo, Komatsu, Reyes, and Tribin (2025), show that while women are underrepresented in high-income and wealth percentiles, there is no significant difference in effective tax rates for men and women of the same income or wealth levels.11

Colombia has a wealth tax, and all taxpayers who are required to file a return must report their wealth. Although wealth reporting requirements allow taxpayers at the top of the distribution to report wealth levels substantially below market value, it is reasonable to assume that the reported wealth distribution is a monotonic transformation of the real wealth distribution. Comparing the share of women in the top income percentiles to the share of women in the top wealth percentiles leads to a surprising result: In 2021, the share of women is higher in the top wealth percentiles than in the top income percentiles. In effect, of the top 5% of individuals by wealth, 49.9% are women, as are 45.7% of the top 1%, 38% of the top 0.1%, and 33% of the top 0.01%.12

The relatively higher representation of women in high wealth percentiles compared to women’s representation in high-income percentiles is the most interesting fact that emerges from disaggregating Colombian administrative tax data by taxpayer sex. Because wealth is the accumulation of income, it is not immediately obvious how women could accumulate enough wealth to make their representation in high-wealth percentiles larger than their representation in high-income percentiles. While this result warrants additional research, one possible explanation is that Colombian tax law allows married couples to reallocate a spouse’s wealth to the other spouse for tax purposes, leading to tax planning strategies that make relatively low-income women wealthier (at least for tax purposes). Importantly, this may not reflect real economic empowerment or financial control, but rather a legal tax avoidance strategy. This example challenges the assumption that tax rules affect all individuals equally, showing how formally neutral provisions can produce outcomes that obscure actual economic inequality and fairness.

The average income tax rate for women who file a tax return is lower than for men who file a tax return. Between 2019 and 2022, the average income tax rate for men went from 9% to 6%, whereas for women it went from 8% to 5%.13 However, lower income-tax rates for women are not explained by preferential treatment, but rather by the progressivity of the tax system combined with the lower incomes of women. That is to say, women face a lower average income tax rate, but simply because their incomes are lower than men’s incomes, and tax rates are lower for those with lower incomes. When average tax rates for men and for women in the same income brackets are compared, they are essentially identical.

That women and men of similar income levels are taxed similarly is not surprising, as the tax system was not designed with the goal of redistributing from men toward women. The question remains, however, as to whether that should be the case. This was the subject of the policy debate over the tax reform of 2022, which concluded that it should not. For instance, it was suggested that expenditure on care work (which frees up women’s time to work in higher-earning occupations) should be tax-deductible. The measure was not implemented because it was considered to be highly regressive, as the demand for care work is driven by high-income women and care work is overwhelmingly supplied by low-income women, and the tax benefit under consideration would both reinforce the feminization of care work and benefit primarily high-income households. In the end, the view that the tax system should raise maximum revenue and maintain progressivity prevailed, and equality between men and women should be pursued primarily through public investment. Indeed, translating legal mandates into measurable outcomes requires a robust gender budgeting framework—something Colombia is actively building.

Gender budgeting: Definition and Colombia’s framework

Gender budgeting refers to the integration of gender analysis into fiscal policy processes to ensure that budgetary decisions advance equality in outcomes for women and men. Scholars such as Elson (2006) and Grown and Valodia (2010) argue that public budgets are not neutral—they encode government priorities that can either reinforce or reduce inequality.14 Gender budgeting involves not only quantifying expenditures on programs explicitly aimed at promoting gender equality, but also evaluating and reshaping overall spending to reflect its differential impacts on women and men. Over the past two decades, it has been increasingly recognized as a global public finance standard, promoted by institutions like UN Women and gaining traction within international financial institutions such as the World Bank and the International Monetary Fund (IMF).15 Both now monitor gender-responsive budgeting practices through platforms like the IMF’s Gender Data Portal and the World Bank’s Women, Business and the Law (WBL) initiative.16

Colombia has made notable efforts to institutionalize gender budgeting, supported by a growing legal framework. According to the World Bank’s WBL pilot initiative, this framework includes key legislative instruments such as Ley 2294 of 2023 (which establishes the current National Development Plan 2022–2026), Ley 2342 of 2023 (regulating the 2024 national budget), and Ley 1434 of 2011 (creating the Legal Commission for Women’s Equity). These laws collectively establish a National System of Equality and Equity, require the adoption of gender budget tracers, and mandate reporting of gender-related expenditures to Congress. Ley 2294 explicitly calls for coordination across the state to address structural gender inequalities and uphold the right to equality. The WBL pilot analysis confirms that this legal framework qualifies Colombia for a “Yes” on the existence of gender-responsive budgeting.

Significant gaps remain, however, in the implementation of gender budgeting. As also noted in the WBL data, Colombia lacks a statutory mandate for the use of sex-disaggregated data in the budget process and does not require ex-post gender impact assessments.17 Although Ley 2335 of 2023 instructs the national statistics agency (DANE) to collect data with a differential approach—including gender—it does not require this data to inform budgetary planning. Guidance documents, such as the Guía para la Inclusión del Enfoque Diferencial e Interseccional (2020), encourage the use of such data in gender diagnostics but lack legal authority.18 The OECD (2023) confirms that while Colombia includes “gender perspectives” in its budget reporting, these are not systematically evaluated for outcomes.19 As such, Colombia’s gender budgeting efforts, though comparatively advanced in legal terms, face key challenges in monitoring, evaluation, and data integration—issues that must be addressed to realize the full potential of gender-responsive fiscal policy.

One challenge is the lack of continuity of gender budgeting through political transitions. Most gender budgeting measures have been incorporated into National Development Plans (Plan Nacional de Desarrollo, PND), a key policy document that establishes the national strategy for the four-year term of each presidential administration. While these plans remain in force for the duration of a government’s term, each new administration can decide whether or not to include gender budgeting measures in their own strategic plan. As a result, a particular government’s approach is not necessarily carried across political cycles.

A comprehensive regulatory framework is needed to ensure consistency and permanence in gender budgeting practices, regardless of changing government priorities. Furthermore, greater transparency in public finance is essential for advancing gender-responsive budgeting in Colombia. Although the national budget is published, and it is possible to track allocations to each ministry or territorial entity, there is a significant lack of detailed, disaggregated information on actual expenditures, as noted earlier. While funding allocations are published, there is little visibility into how much is actually spent, on which programs, and with what outcomes—especially regarding gender equality objectives. In other words, while we know how much funding is assigned, we often do not know how—or whether—those funds are ultimately spent. This gap severely limits the ability to assess the effectiveness and equity of public spending. Without reliable data on real expenditures, it becomes difficult to carry out a comprehensive analysis of fiscal incidence overall and through a gender lens to hold institutions accountable for implementing policy priorities, including the country’s gender equality commitments.

The Colombian government has made care a national policy priority, as reflected in recent legislation and its broader commitment to gender budgeting.20 However, translating this legal framework into action requires understanding the financial implications of care policies—something made difficult by limited budget transparency and weak integration of care into fiscal planning. In this context, macroeconomic modeling has emerged as a critical tool to estimate the financial requirements of care investments and assess their potential economic and equity impacts. Models such as a gendered dynamic general equilibrium model for analysis of care (GEM-Care) help simulate the effects of targeted investments—such as in childcare—providing policy insights that are not captured in administrative data alone.21 We turn to this next.

Investing in universal care services: A macroeconomic approach

Colombia has made clear constitutional and legislative commitments to care.22 The 1991 Constitution recognizes the state’s duty to protect family welfare and promote gender equality. Complementing this, Ley 1413 of 2010 (the Care Economy Law) mandates national time-use surveys and requires institutions like DANE, the finance ministry, and the national planning department to integrate data on paid and unpaid care work into national accounts and policy planning. The policy foundation was strengthened further by Ley 1804 of 2016, which established a comprehensive framework for early childhood development and the expansion of public childcare services.23

Yet this strong legal foundation has not been matched by corresponding support in fiscal planning. Gender budgeting efforts have yet to fully account for the cost of implementing care policies, and traditional economic models continue to overlook unpaid care work. This invisibility distorts public budgets, underestimates women’s contributions, and reinforces structural inequalities. Several papers have argued that recognizing and valuing unpaid care is not only a matter of social justice but a macroeconomic necessity.24 By integrating universal care services into fiscal policy, gender budgeting has the potential to transform public finance systems and rebalance who bears the cost of social reproduction.

In Colombia, the need to invest in universal care services is particularly urgent. According to the 2020-2021 National Time Use Survey (ENUT), women spend an average of 7 hours and 44 minutes per day on unpaid care work—more than twice as much as men.25 This unequal distribution of care responsibilities severely limits women’s participation in the formal labor market. Only about half of Colombian women are in the labor force, and female unemployment remains high compared to the averages of other Latin American and Caribbean countries.26 The WBL 2024 childcare indicator adds further nuance to this picture. While Colombia has established the legal framework to ensure access, affordability, and quality of childcare, implementation remains uneven. Gaps persist in areas such as financial support mechanisms for providers and regular monitoring of service quality. These shortcomings weaken the effectiveness of existing legislation and slow progress toward a more inclusive and productive economy.27

The implementation of legal commitments can be enhanced by sound economic analysis of their financing requirements. Here, macroeconomic models offer critical guidance. Using a gender-aware Computable General Equilibrium (CGE) model, Cicowiez et al. (2023) evaluate three childcare policy interventions in Colombia: childcare subsidies, expanded public childcare, and unconditional cash transfers.28 The model, GEM-Care, uniquely integrates unpaid care and market labor, showing how public investments in childcare infrastructure—especially public provision—is the only intervention among the three that delivers simultaneous gains in GDP and women’s labor force participation.

The GEM-Care simulations show that subsidized and public childcare reduces unpaid care time, redistributes labor within households, and boosts women’s formal employment. Notably, public childcare is more labor-intensive and redistributive than subsidies, offering larger macroeconomic gains and deeper gender equality improvements. By shifting care responsibilities from unpaid to paid work, such investments also raise GDP-measured consumption and expand formal employment—broadening the tax base and contributing to increased public revenue over the medium to long term. Subsidies also yield positive effects, particularly in boosting women’s paid work, but with more modest economic returns. In contrast, cash transfers—though widely used in Colombia to address inequality—are fiscally less sustainable and may inadvertently reduce formal labor market participation, especially among women.29 Beyond demonstrating these economic impacts, the GEM-Care simulations highlight crucial fiscal trade-offs. While all three childcare interventions—subsidies, public provision, and cash transfers—reduce unpaid care time, they differ significantly in their long-term effects on growth and equity.

These findings highlight a critical insight for fiscal policy: Not all social spending generates the same economic and gender equality returns. Reducing the cost of market-provided childcare—regardless of the financing mechanism—leads to higher female employment in the formal economy, as both paid and unpaid care sectors rely heavily on women’s labor. Under the scenario of a childcare subsidy equal to 0.5% of GDP (financed through income taxes), women’s time in paid work increases by 0.5–0.6%, and by 2030, the policy generates approximately 62,000 new full-time jobs for women and 52,000 for men and increases GDP, recovering the investment made.30

Colombia’s legislative groundwork for gender budgeting and care investment is solid, but the transformative power lies in execution. The Colombian gender budget can better incorporate the insights of gender-aware macro modeling, prioritizing strategies—like public childcare—that deliver the highest returns for inclusive growth, structural equality, and long-term development. When governments fund public universal care services and care infrastructure, they unlock women’s economic potential and enhance national growth. At the same time, the tax system must generate sufficient revenue to jump-start this public investment.

The findings from IMF research, WBL pilot data, and Cicowiez et al. (2023) converge on this point.31 Designing, targeting, and measuring the right policies is not a theoretical exercise—it is the key to achieving inclusive, sustainable development. As Colombia continues to strengthen its gender budgeting practices, its next challenge will be scaling up investment in universal care services. The country already has the laws; now it must act on the evidence.

Conclusion: Turning data into action

Colombia has taken important steps toward a more equitable fiscal system. Disaggregated tax data has uncovered some gender inequalities and challenged the assumption that formal neutrality guarantees fairness. Without corrective mechanisms, taxation can mirror inequality rather than reduce it. Yet tax reform alone is insufficient. The real engine of change lies in public spending—especially in universal care services. Colombia’s legal framework and policy simulations provide a blueprint for inclusive, sustainable development. The next phase requires political will, accountability, and consistent implementation. By aligning fiscal decisions with gender equity goals, Colombia can fulfill its constitutional promise and become a model for gender-responsive public finance.

Authors

-

Acknowledgements and disclosures

The Brookings Institution is a nonprofit organization devoted to independent research and policy solutions. Its mission is to conduct high-quality, independent research and based on that research, to provide innovative, practical recommendations for policymakers and the public. The conclusions and recommendations of any Brookings publication are solely those of its author(s), and do not reflect the views or policies of the Institution, its management, its other scholars, or the funders acknowledged below.

This publication is supported by the Gates Foundation, the William and Flora Hewlett Foundation, and the Norwegian Agency for Development Cooperation (Norad). The findings and conclusions contained within are those of the authors and do not necessarily reflect positions or policies of the donors.

Brookings recognizes that the value it provides is in its absolute commitment to quality, independence, and impact. Activities supported by its donors reflect this commitment.

-

Footnotes

- Iregui-Bohórquez, Ana María, Ligia Alba Melo-Becerra, María Teresa Ramírez-Giraldo, and Ana María Tribín-Uribe. 2025. El Camino Hacia La Igualdad de Género En Colombia: Todavía Hay Mucho Por Hacer. Books. Banco de la Republica de Colombia. https://doi.org/10.32468/Ebook.664-493-8.

-

Revenue Statistics in Latin America and the Caribbean 2025. 2025. OECD Publishing. OECD.

https://www.oecd.org/en/publications/2025/05/revenue-statistics-in-latin-america-and-the-caribbean-2025_2922daa3.html. - Ibid.

-

Gamboa, Luis Fernando, Ana Maria Tribin, Luis Carlos Reyes, Eduardo Iriondo, and Hitomi Komatsu. (n.d.). “A Brief Description of the Presence of Women in the Income Taxpayer’s Population in Colombia during 2019–2022.” Unpublished manuscript. Forthcoming; Gamboa, Luis Fernando, Luis Carols Reyes, Ana Maria Tribin, and Hitomi Komatsu. 2024. “Sex-Disaggregating Tax Administrative Data: Experience from Colombia’s Tax and Customs Authority. Gender and Tax Dialogue Knowledge Note.” World Bank.

https://openknowledge.worldbank.org/server/api/core/bitstreams/a0f68bbb-0096-4dda-b2a2-7b8f36adf141/content. - Ibid.

-

Chetty, Raj, Nathanial Hendren, Patrick Kline, and Emmanuel Saez. 2014. “Where Is the Land of Opportunity? The Geography of Intergenerational Mobility in the United States.” The Quarterly Journal of Economics 129 (4): 1553-623.

https://academic.oup.com/qje/article/129/4/1553/1853754 -

Chetty, Raj, John N. Friedman, and Jonah E. Rockoff. 2014. “Measuring the Impacts of Teachers II: Teacher Value-Added and Student Outcomes in Adulthood.” American Economic Review 104 (9): 2633-79.

https://doi.org/10.1257/aer.104.9.2633. -

Piketty, Thomas, and Emmanuel Saez. 2003. “Income Inequality in the United States, 1913–1998*.” The Quarterly Journal of Economics 118 (1): 1–41. https://doi.org/10.1162/00335530360535135.; Kopczuk, Wojciech, and Emmanuel Saez. 2004. “Top Wealth Shares in the United States: 1916–2000: Evidence from Estate Tax Returns.” NBER Working Paper 10399. Preprint, National Bureau of Economic Research, March.

https://www.nber.org/system/files/working_papers/w10399/w10399.pdf.; Alvaredo, Facundo, Anthony B. Atkinson, Thomas Piketty, and Emmanuel Saez. 2013. “The Top 1 Percent in International and Historical Perspective.” Journal of Economic Perspectives 27 (3): 3-20.

https://doi.org/10.1257/jep.27.3.3. -

Alstadsæter, Annette, Niels Johannesen, and Gabriel Zucman. 2019. “Tax Evasion and Inequality.” American Economic Review 109 (6): 2073-103.

https://doi.org/10.1257/aer.20172043. - Gamboa, Luis Fernando, et al., “Sex-Disaggregating Tax Administrative Data: Experience from Colombia’s Tax and Customs Authority. Gender and Tax Dialogue Knowledge Note.”

- Gamboa, Luis Fernando, et al., “A Brief Description of the Presence of Women in the Income Taxpayer’s Population in Colombia during 2019–2022.”; “Estadísticas de ingresos y riqueza en clave de género: un zoom en las personas más ricas de Colombia. Elementos Conceptuales Para Una Tributacion Con Enfoque de Genero.” 2024. DIAN. https://www.dian.gov.co/dian/cifras/Informesespeciales/02-Estadisticas-de-Ingreso-y-Riqueza-en-Clave-de-Genero-PLURAL.pdf

- Gamboa, Luis Fernando, et al., “Sex-Disaggregating Tax Administrative Data: Experience from Colombia’s Tax and Customs Authority. Gender and Tax Dialogue Knowledge Note.”

- Gamboa et al., “A Brief Description of the Presence of Women in the Income Taxpayer’s Population in Colombia during 2019–2022.”

-

Elsen, Diane. 2006. Budgeting for Women’s Rights: Monitoring Government Budgets for Compliance with CEDAW. UNIFEM. https://gender-financing.unwomen.org/en/resources/b/u/d/budgeting-for-womens-rights-monitoring-government-budgets-for-compliance-with-cedaw.; Grown, Caren, and Imraan Valodia, eds. 2010. Taxation and Gender Equity: A Comparative Analysis of Direct and Indir. Routledge.

https://www.routledge.com/Taxation-and-Gender-Equity-A-Comparative-Analysis-of-Direct-and-Indirect-Taxes-in-Developing-and-Developed-Countries/Grown-Valodia/p/book/9780415492621?srsltid=AfmBOoqzVilq9h79Fe5OX_LpVH_KWtMS3BvTVfWW9DUCqmuTJS7PuGPf -

Gender Responsive Budgeting in Practice: A Training Manual. 2006. UNFPA, UNIFEM.

https://www.unwomen.org/en/digital-library/publications/2010/1/gender-responsive-budgeting-in-practice-a-training-manual. - IMF. n.d. “IMF Data Mapper: Prominent Gender Budgeting Countries Covered in the Surveys.” Accessed July 23, 2025. https://www.imf.org/external/datamapper/profile.; Women, Business and the Law 2024. n.d. World Bank. Accessed July 22, 2025. https://openknowledge.worldbank.org/entities/publication/853a55af-f1ba-4979-949c-61979af2fbb9.

-

“Women, Business and the law 2024.” 2024. World Bank.

https://bit.ly/WBL2024_FullReport - “Guía para la Inclusión del Enfoque Diferencial e Interseccional.” 2020. Departamento Administrativo Nacional de Estadística. Dane. https://www.dane.gov.co/files/investigaciones/genero/guia-inclusion-enfoque-difencias-intersecciones-produccion-estadistica-SEN.pdf

- Gender Budgeting in OECD Countries 2023. 2023. OECD Publishing. OECD. https://www.oecd.org/en/publications/gender-budgeting-in-oecd-countries-2023_647d546b-en.html.

-

“Política Nacional Cuidado.” 2025. Consejo Nacional De Política Económica Y Social República De Colombia Departamento Nacional De Planeación, February.

https://colaboracion.dnp.gov.co/CDT/Conpes/Econ%C3%B3micos/4143.pdf. - GEM-Care is a computable general equilibrium (CGE) model designed to incorporate gender, unpaid care work, and household decision-making into macroeconomic analysis. For more information, see: Lofgren, Hans, Kijong Kim, Marzia Fontana, Martin Cicowiez. 2020. “A Gendered Social Account Matrix for South Korea.” CWE-GAM Working Papers Series. American University. Washington. D.C. https://research.american.edu/careworkeconomy/wp-content/uploads/sites/2/2020/05/LofgrenPDFFINAL2.pdf

-

Care economy under the Ley 1413 of 2010 refers to: ” unpaid work carried out in the household, related to maintaining the home, caring for other members of the household or community, and sustaining the paid labor force. This category of work is of fundamental economic importance in society.” Ley 1413 de 2010 (2010).

https://www.funcionpublica.gov.co/eva/gestornormativo/norma.php?i=40764. -

Meurs, Mieke, Ana Maria Tribin, Maria Floro, and Stephan Lefebvre. 2020. “Prospects for Gender-Sensitive Macroeconomic Modelling for Policy Analysis in Colombia: Integrating the Care Economy.” CWE-GAM Working Paper Series 20–02. Preprint, Program on Gender Analysis in Economics (PGAE) American University, March.

https://research.american.edu/careworkeconomy/global-dimensions-of-care-work/. -

Chakraborty, L., V. Nayyar, and K. Jain. 2020. Determining Gender Budgeting in Multi-Level Federalism. March.

https://hdl.handle.net/1885/733747728; Hara, Nobuko. 2007. “Towards a Political Economy of Care.” Journal of International Economic Studies 21 (March): 17–31. https://doi.org/10.15002/00002042; Klatzer, Elisabeth, and Angela O’Hagan. 2020. “Moving Boundaries with Gender Budgeting: From the Margins to the Mainstream: From the Margins to the Mainstream.” In New Perspectives on Political Economy and Its History, edited by Maria Cristina Marcuzzo, Ghislain Deleplace, and Paolo Paesani. Palgrave Studies in the History of Economic Thought. Palgrave Macmillan.

https://doi.org/10.1007/978-3-030-42925-6_4. -

“National Survey on Time Use (ENUT) 2020-2021: Boletin Tecnico.” 2022. DANE, October.

https://www.dane.gov.co/index.php/estadisticas-por-tema/pobreza-y-condiciones-de-vida/encuesta-nacional-del-uso-del-tiempo-enut. - Olivieri, Sergio, and Miriam Muller. n.d. Gender Equality in Colombia : Country Gender Assessment. World Bank. Accessed July 23, 2025. https://documents1.worldbank.org/curated/en/665381560750095549/pdf/Colombia-GA.pdf.

- “Colombia: Women, Business and the Law 2024.” 2024. World Bank. https://wbl.worldbank.org/content/dam/documents/wbl/2024/pilot/WBL24-2-0-Colombia.pdf.

-

Cicowiez, Martin, Hans Lofgren, Ana Tribin, and Tatiana Mojica. 2023. “Women’s Market Work and Childcare Policies in Colombia: Policy Simulations Using a Computable General Equilibrium Model.” Philippine Review of Economics (Online ISSN 2984-8156) 60 (1): 1.

https://scispace.com/pdf/womens-market-work-and-childcare-policies-in-colombia-policy-2bpf4pg4.pdf - Ibid.

- Ibid.

- “1. Gender Budgeting and 2. Gender Equality Indices.” n.d. IMF. Accessed September 16, 2025. https://www.imf.org/external/datamapper/datasets/GD.; “Women, Business and the Law 2024.” 2024. World Bank. https://openknowledge.worldbank.org/entities/publication/853a55af-f1ba-4979-949c-61979af2fbb9.; Cicowiez et al. “Women’s Market Work and Childcare Policies in Colombia: Policy Simulations Using a Computable General Equilibrium Model.”

https://www.oecd.org/en/publications/2025/05/revenue-statistics-in-latin-america-and-the-caribbean-2025_2922daa3.html.

https://openknowledge.worldbank.org/server/api/core/bitstreams/a0f68bbb-0096-4dda-b2a2-7b8f36adf141/content.

https://academic.oup.com/qje/article/129/4/1553/1853754

https://doi.org/10.1257/aer.104.9.2633.

https://www.nber.org/system/files/working_papers/w10399/w10399.pdf.; Alvaredo, Facundo, Anthony B. Atkinson, Thomas Piketty, and Emmanuel Saez. 2013. “The Top 1 Percent in International and Historical Perspective.” Journal of Economic Perspectives 27 (3): 3-20.

https://doi.org/10.1257/jep.27.3.3.

https://doi.org/10.1257/aer.20172043.

https://www.routledge.com/Taxation-and-Gender-Equity-A-Comparative-Analysis-of-Direct-and-Indirect-Taxes-in-Developing-and-Developed-Countries/Grown-Valodia/p/book/9780415492621?srsltid=AfmBOoqzVilq9h79Fe5OX_LpVH_KWtMS3BvTVfWW9DUCqmuTJS7PuGPf

https://www.unwomen.org/en/digital-library/publications/2010/1/gender-responsive-budgeting-in-practice-a-training-manual.

https://bit.ly/WBL2024_FullReport

https://colaboracion.dnp.gov.co/CDT/Conpes/Econ%C3%B3micos/4143.pdf.

https://www.funcionpublica.gov.co/eva/gestornormativo/norma.php?i=40764.

https://research.american.edu/careworkeconomy/global-dimensions-of-care-work/.

https://hdl.handle.net/1885/733747728; Hara, Nobuko. 2007. “Towards a Political Economy of Care.” Journal of International Economic Studies 21 (March): 17–31. https://doi.org/10.15002/00002042; Klatzer, Elisabeth, and Angela O’Hagan. 2020. “Moving Boundaries with Gender Budgeting: From the Margins to the Mainstream: From the Margins to the Mainstream.” In New Perspectives on Political Economy and Its History, edited by Maria Cristina Marcuzzo, Ghislain Deleplace, and Paolo Paesani. Palgrave Studies in the History of Economic Thought. Palgrave Macmillan.

https://doi.org/10.1007/978-3-030-42925-6_4.

https://www.dane.gov.co/index.php/estadisticas-por-tema/pobreza-y-condiciones-de-vida/encuesta-nacional-del-uso-del-tiempo-enut.

https://scispace.com/pdf/womens-market-work-and-childcare-policies-in-colombia-policy-2bpf4pg4.pdf

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).