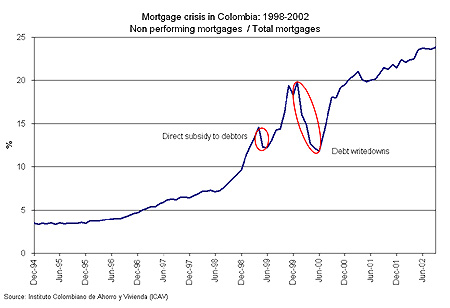

As many other Latin American countries, Colombia faced a severe financial crisis in the late 1990s. As is currently the case in the U.S., the root cause of the problem was a rapid increase in loan-to-value ratios that made mortgage delinquencies and defaults climb to unprecedented levels. In Colombia, this was the result of an implosion of real estate prices after the end of the housing bubble of the mid-1990s combined with an increase in interest rates. At that time mortgages were indexed to the nominal deposit interest rate, causing a significant increase in the outstanding value of the loans. With an increase in the numerator and a decrease in the denominator, LTVs rose very rapidly causing an increase in delinquencies and foreclosures that make the current U.S. crisis pale in comparison (see figure).

How did Colombia deal with this situation and what are the lessons for the U.S.? In addition to discarding the existing indexation system, the Colombian government responded by adopting four measures:

- Large banks that were too weak to survive were intervened while the smaller banks were allowed to fail. The government then appointed new administrators and injected capital into the public-owned banking system. The cost of these rescue operations was approximately 4 percent of GDP (if the same amount were to be allocated in the US it would be equivalent to $552 billion). About two-thirds of this outlay was later recovered by selling two banks in 2005-06. The government still owns one large bank. In the end, not a bad deal for the government or the banking sector.

- A facility was created by the government to provide capital to private banks. To access this facility, banks were required to put their distressed assets outside their balance sheets. The government took preferred shares, while shareholders had to provide more capital and lost control over key decisions, including dividends. The preferred stock received interest. All these loans were paid back and the government made a profit because interest rates were not subsidized.

- A facility was created by the government to collect the toxic assets of the government-owned banks. This entity began gradually selling the bad assets at market prices. A large chunk of the remaining assets of this facility were auctioned in 2007 at a profit to the government.

- Write downs and other forms of debt relief like subsidies for the repurchase of foreclosed homes were given to mortgage debtors. The Colombian Treasury issued debt that was given to the banks in exchange for the write offs (with a cost to the banks because these bonds paid a lower rate than the original mortgages). On average about 15 percent of the original debt was taken out of the households’ balance sheet. The cost to taxpayers was equivalent to 1.6 percent of GDP. If something of this magnitude were to be given to households in the U.S. it would be equivalent to $221 billion. This money was never recovered and did little to solve the problem

In the U.S., it is now argued, as it was then said in Colombia, that households have too much debt to maintain while their assets are losing value. Congress is proposing the idea that households are buried under a pile of debt that is essentially impossible to pay and these homeowners must be rescued. In addition, certain Members of Congress ask, if everyone is getting relief, why not America’s working families?

The figure below shows why households should not be given debt relief as part of the recovery plan in the U.S. as it show that in Colombia, non-performing loans actually decreased momentarily right before the relief announcements (loans had to be performing to be eligible) but increased dramatically afterwards. Of course, the higher the fraction of NPLs the more difficult the problem is. So if households believe that delinquencies are somehow rewarded no rescue package will ever be sufficient. Although it may be tempting for Congress and the administration to provide help to troubled homeowners, it is a bad idea that the U.S. has to avoid, not because it is costly and ineffective, but because it makes matters worse.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Op-edLessons from Another Crisis: Why Providing Debt Relief for Households is Not a Good Idea

September 30, 2008