Below is a Viewpoint from Chapter 1 of the Foresight Africa 2021 report, which explores top priorities for the region in the coming year. This year’s issue focuses on strategies for Africa to confront the twin health and economic crises created by the COVID-19 pandemic and emerge stronger than ever. Read the full chapter on the great reset.

Remittances—money sent by migrants to families back home—provide a financial lifeline to millions of households. Remittance flows to low- and middle-income countries reached $550 billion in 2019, surpassing foreign direct investment and official development aid. These are only recorded flows; the true size—including those through informal channels—is even larger.

Remittances—money sent by migrants to families back home—provide a financial lifeline to millions of households. Remittance flows to low- and middle-income countries reached $550 billion in 2019, surpassing foreign direct investment and official development aid. These are only recorded flows; the true size—including those through informal channels—is even larger.

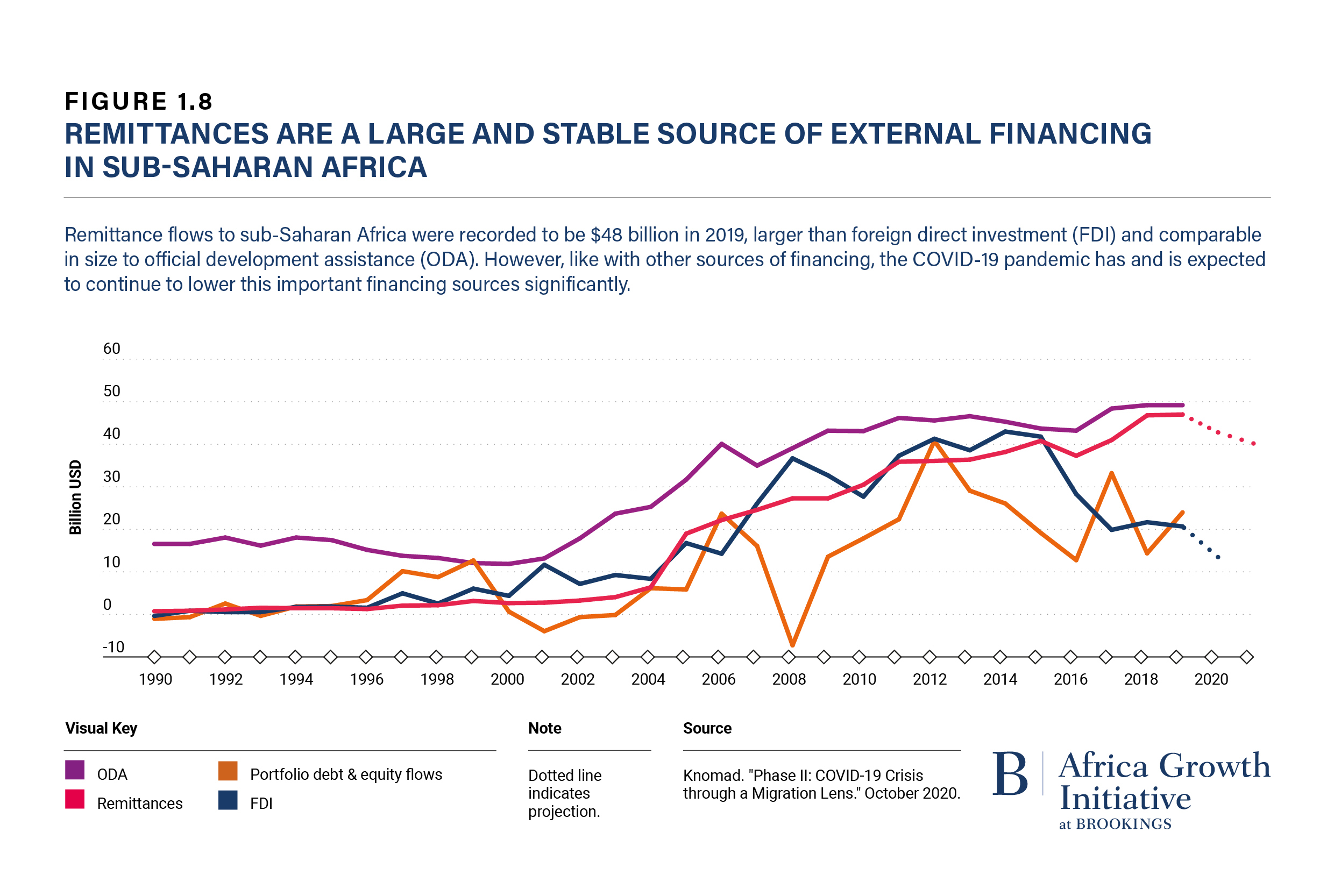

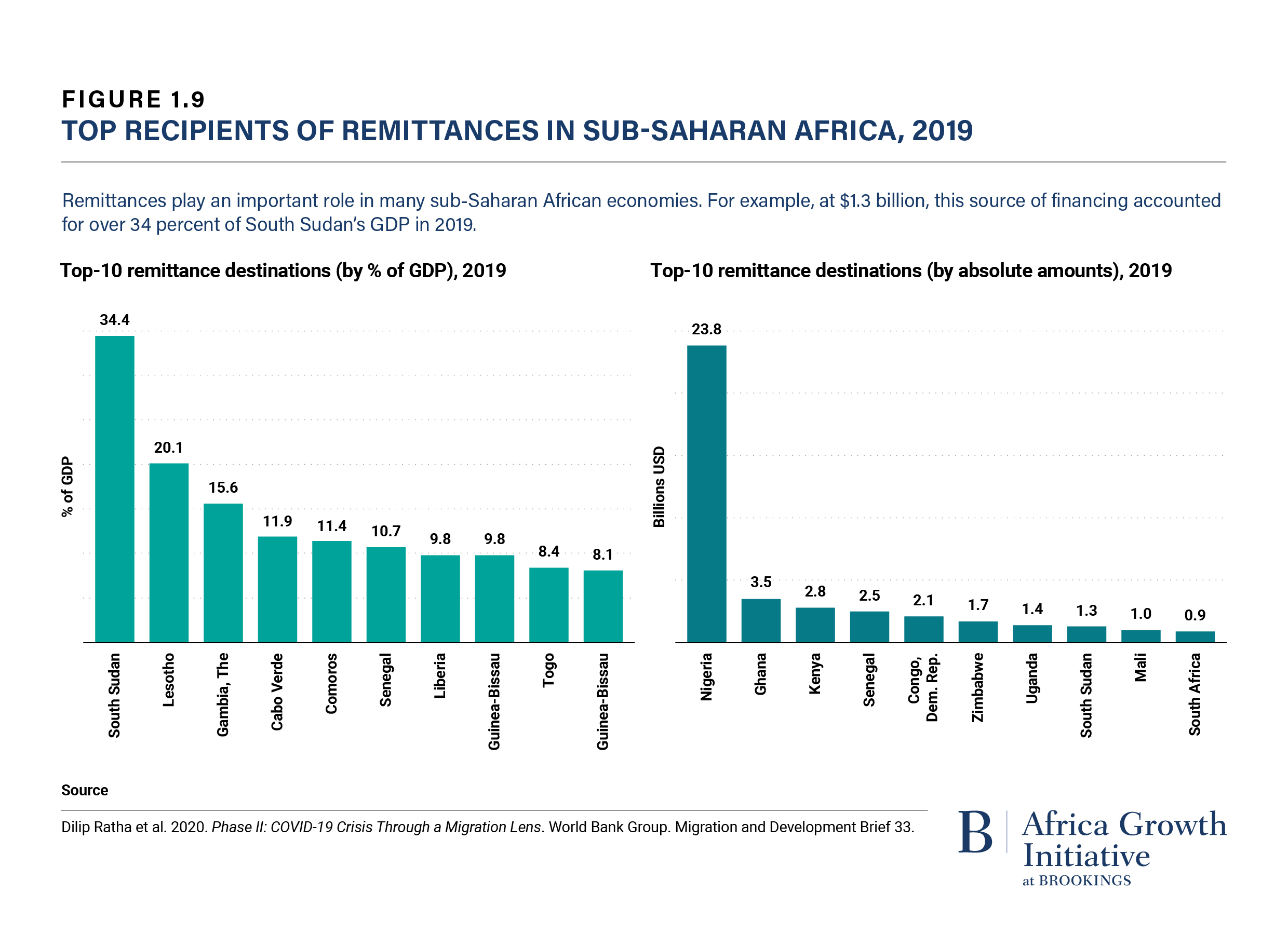

Remittance flows to sub-Saharan Africa were recorded to be $48 billion in 2019 (Figure 1.8), but the true total is likely to be significantly larger. Nigeria alone received about half of total remittance flows to sub-Saharan Africa (Figure 1.9, first panel). In general, the economies of smaller, poorer, and fragile countries are more dependent on remittances: Controlling for the size of the economy, the top recipient countries in the region in 2019 included South Sudan (35 percent of GDP), Lesotho (21 percent of GDP) and The Gambia (15 percent of GDP) (Figure 1.9, second panel). While data are not available for Somalia, the country is also known to be highly dependent on remittances as a source of income and external financing.

Impacts of the COVID-19 crisis

Remittance flows to sub-Saharan Africa are projected to decline by 8.8 percent, to $44 billion in 2020, followed by a further decline of 5.8 percent, to $41 billion in 2021. The COVID-19 pandemic has hit remittances providers in a variety of ways: Sub-Saharan migrant workers, especially those in high-income OECD countries, have lost jobs or seen their incomes plummet, reducing their ability to send money home. Weak oil prices have affected outward remittances to Africa from the Gulf Cooperation Council countries (Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates). Currency exchange rates also affect remittance flows: When source currencies (e.g., the euro) depreciate against the U.S. dollar, the value of remittances in U.S. dollar terms declines; when the currency of the recipient country (e.g., the Nigerian naira) depreciates, migrants may send more money home to take advantage of cheaper prices. In Africa, many countries still practice various forms of currency control, resulting in a divergence between the parallel and the market exchange rate and a diversion of flows to informal, unrecorded channels.

The decline in remittances is worrisome for the region where almost 40 percent of the population live in extreme poverty, and millions rely on remittances to put food on the table and have children stay in school. Thus, government efforts are needed to support households experiencing hardships, and international efforts are needed to keep remittances flowing to Africa.

Future of migration and remittances in Africa

The pandemic has significantly dampened new migration flows worldwide due to widespread travel restrictions, fear of the virus, and weak job prospects. In many host countries, employment levels for foreign workers have fallen, invariably more so than for native-born workers. A significant number of unemployed migrant workers are returning to their countries of origin, which are now facing the challenge of accommodating hundreds of thousands (if not millions) of returnees, including through the provision of health care, housing, jobs, and financial support.

While trying to impose travel and visa restrictions, host countries must not impose irreversible restrictions that could constrain businesses from hiring essential workers (including foreign workers) during the recovery phase.

In the long run, migration flows from Africa are expected to increase significantly, driven by income gaps, the rapidly growing working-age population, and climate change. Notably, the average income in high-income OECD countries is over 50 times the average income in low-income countries. At recent (pre-COVID-19) growth rates, it would take over a hundred years to close that gap; the pandemic is likely to worsen it.

What can be done?

A key lever for facilitating remittance flows during the crisis is reducing the cost of sending money: The fees paid to remittance service providers to send money to Africa average nearly 9 percent— the highest rate in the world and three times the Sustainable Development Goal target for remittance costs (3 percent). The cost of international remittances within Africa—intra-regional migration and remittances are large there—is even higher than the cost of remittances from the United States or Europe. Digital remittance channels, which have gained popularity during the crisis, also have high fees that have increased in recent months.

Lowering the burden of sending remittances can maximize this important flow of financing for development. Policymakers must work to make sure remittance service providers do not face difficulties in partnering with correspondent banks. Indeed, opening access of money transfer operators (MTOs) to partnerships with national post offices, national banks, and telecommunications companies could help remove entry barriers and increase competition in remittance markets. And these remittance channels can also be used to mobilize diaspora investments through diaspora bonds and bond financing through securitization of future flows of remittances. The global community should consider creating a non-profit remittance platform to provide a one-stop solution to keep remittances flowing and leverage them for development financing for the benefit of millions of poor people in Africa and the rest of the world.

Related Content

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Keep remittances flowing to Africa

March 15, 2021