In April 2015, the board of governors at the Asian Development Bank (ADB) approved a groundbreaking innovation. For over 40 years, the bank’s mission led it to handle two types of loans quite separately. Low-income countries received generous, concessional loans and grants from the ADB’s concessional window, the Asian Development Fund (ADF). And normal, market-based loans were made to middle-income countries from its “ordinary capital resources.” Now, with a stroke of the pen, these two lending operations will be combined from January 1, 2017 onwards.

Established in 1973, the ADF is a special fund regularly replenished by donor contributions. ADF loans are concessional, with lower interest rates than normal and longer maturity periods.

But the ADB also assists middle-income countries with loans at market-based rates. These “OCR” loans come from the ordinary capital resources balance sheet, and are financed by leveraging the equity of the ADB that has been contributed by its shareholders.

The combination of ADF and OCR loans radically changes this traditional approach to lending, which until now has been the standard at multilateral institutions. Going forward, the ADF will focus exclusively on providing grant assistance to the most debt-distressed countries in the Asia and Pacific region. Lower-income countries currently eligible for ADF loans will continue to receive concessional loans on the same terms and conditions as current ADF loans, but these loans will henceforth be provided from the expanded OCR balance sheet. They key difference: Donor contributions will no longer be required to support concessional lending operations.

Before this innovation of combining the balance sheets, it had become increasingly challenging for the ADB to meet the financial requirements of both lower-income and middle-income countries. The resources of the ADF were constrained by donors’ ability to contribute sufficient funds, and OCR resources were constrained by the bank’s limited equity.

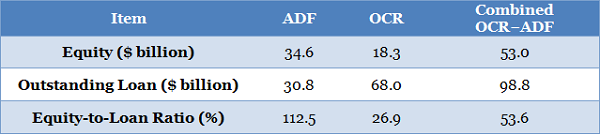

The combination relieves these financial constraints by transferring ADF equity to OCR equity, enhancing ADB’s ability to leverage the combined resources by significantly expanding the equity base of ADB, and by using the expanded OCR balance sheet more efficiently and effectively. Table 1 shows the difference.

Currently, OCR equity is leveraged 3.7 times. On the other hand, ADF equity is currently not leveraged (and thus is being used less efficiently than possible). With the addition of ADF equity, OCR equity will by January 2017 almost triple to about $53 billion.

Figure 1. Balance sheet of combined ADF and OCR scenario, as of 1/1/2017

Source: Asian Development Bank

This is a win-win-win initiative. It increases the ADB’s capacity to support both lower-income countries as well as middle-income countries. It also enhances ADB’s risk-bearing capacity to further support private sector operations. The Asian Development Bank will be in a stronger financial position to respond to any future economic crises and natural disasters. At the same time, the initiative substantially reduces the burden for ADF donors. Donor contributions to continued ADF grant operations will be reduced by up to 50 percent, beginning with the next ADF replenishment in 2017.

The main benefit of the combination is the ability to raise ADB assistance to its developing member countries in the coming years by up to 50 percent. Lower-income countries—those currently receiving ADF loans—will be the key beneficiaries. ADB assistance to these countries will rise by up to 70 percent.

The combination is not expected to adversely affect the ADB’s credit ratings. While combining the ADF and OCR loan portfolios will entail a higher overall credit risk, this will be mitigated by increasing the minimum equity-to-loan ratio (37 percent instead of 25 percent) and improving diversification of the combined loan portfolio.

Four factors were key in helping to push through the innovation:

- The purpose of the combined equity remains unchanged after the merger. Therefore, the proposal did not require approvals of parliaments in donor countries, which could have unduly delayed the process.

- The ADF is a special fund and not a separate legal entity, which made the process simpler.

- A number of ADF countries are likely to graduate in next decade, which makes the financial model viable.

- The proposal does not change the voting shares in ADB, which would have been a politically contentious issue.

The innovation is just a beginning. The increased financial resources are important for enhancing the ADB’s contribution to poverty reduction in the Asia and Pacific region. But how these resources are used is even more important. To that end, the ADB has already begun to identify appropriate projects that will now be possible with the bank’s increased financing capacity. It has started building project pipelines for new ideas, and started a reform process to further capitalize on increased financing capacity by improving project efficiency and effectiveness. If implemented well, the innovation will unleash more than $100 billion additional resources over the next 10 years to eradicate poverty in the Asia and Pacific region.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Innovatively using the Asian Development Bank’s balance sheet to eradicate poverty

May 27, 2015