Studies in this week’s Hutchins Roundup find that accounting for productivity mismeasurement re-allocates growth between high-tech sectors and the rest of the economy, firms whose executives visit the White House experience an increase in value following the visit, and more.

Want to receive the Hutchins Roundup as an email? Sign up here to get it in your inbox every Thursday.

Mismeasurement of multi-factor productivity, although small, matters

David Byrne of the Federal Reserve Board, Stephen Oliner of the American Enterprise Institute, and Daniel Sichel of Wellesley find that, adjusted for mismeasurement in the official statistics of the declines in the prices of high-tech products, multi-factor productivity grew faster in the high-tech sector and slower outside the high-tech sectors than the official statistics suggest. Although this mismeasurement has only a small effect on aggregate productivity measures, the re-allocation implies that innovation in the tech sector has been more rapid than implied by official statistics, deepening the puzzle posed by sluggish productivity growth but also potentially providing a reason to be more optimistic about future prospects for productivity.

Top executives’ visits to the White House raise their firms’ value

Using logs of visitors to the White House between 2009 and 2015, Jeffrey Brown and Jiekun Huang of the University of Illinois at Urbana-Champaign find that corporate executives’ meetings with key policymakers are associated with abnormally high stock returns and that, following meetings with government officials, firms get more government contracts and are more likely to receive regulatory relief. Firms with access to Obama administration officials saw significantly lower stock-market returns following the November election than otherwise similar firms.

Decentralized firms were better able to withstand the Great Recession than their centralized rivals

Using data on 1,300 firms in 10 OECD countries, Philippe Aghion of the College de France, Nicholas Bloom and Brian Lucking of Stanford, Raffaella Sadun of Harvard, and John Van Reenen of MIT conclude that firms that decentralized power to plant managers from headquarters weathered the Great Recession better than more centralized firms – in terms of survival and growth of sales, productivity and profits – in sectors most affected by the crisis. The authors suggest decentralized firms were better able to take advantage of local information and take urgent actions. Corporate organizational differences among countries account for 16 percent of cross-country differences in post-crisis GDP growth, they find.

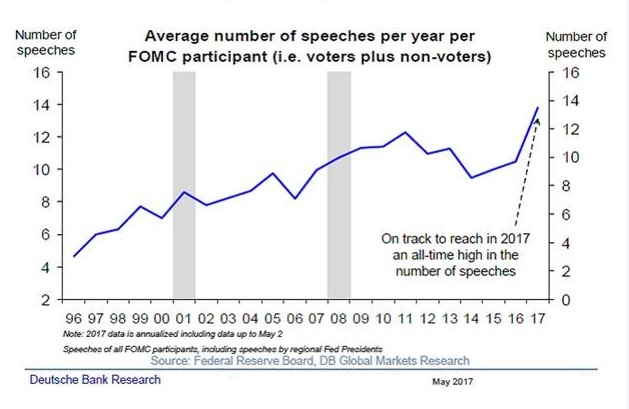

Chart of the week: The number of speeches given by Fed officials is at all-time high this year

Quote of the week: “In many respects, the global financial system is at a fork in the road,” says Bank of England governor Mark Carney.

“On one path, trust and cooperation diminishes, fragmentation hardens, capital flows are disrupted, and trade and innovation are curtailed. If authorities do not have sufficient confidence that their efforts to promote financial stability are being reciprocated elsewhere, then concerns about the risks of openness could intensify. If that happens, domestic authorities could impose local requirements on domestic entities of foreign firms. In a world where many banks and FMIs [financial market intermediaries] are highly interconnected that would generate significant inefficiencies, frustrating the benefits that flow from open trade and investment. Taking this low road would be sub-optimal for all, with fewer jobs, lower growth and higher domestic risks. But there is another path: the high road. This builds on the foundations of a new responsible global financial system that are being put in place. The combination of robust international standards and greater trust as a consequence of transparent implementation and intensive supervisory cooperation can create a system of enhanced equivalence and mutual deference. Such an approach would allow capital to move more freely, efficiently and sustainably between jurisdictions. With robust standards consistently applied, wholesale financial services could be brought more fully into trade agreements, keeping the global financial system open and resilient, and supporting greater trade, investment and innovation. This high road leads to more jobs, higher sustainable growth, and better risk management across the G20.”

Related Content

Related Books

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Hutchins Roundup: Productivity mismeasurement, political access, and more

Thursday, May 4, 2017