Studies in this week’s Hutchins Roundup find that changes in individual stock prices after the US election reflect investors’ expectations about the new administration’s agenda, employment of foreign computer scientists in the US has benefitted US consumers but lowered wages for native-born programmers, and more.

Want to receive the Hutchins Roundup as an email? Sign up here to get it in your inbox every Thursday.

The election’s differential effects on stock prices reflect investors’ expectations about Trump’s agenda

Although most forecasters predicted a decline in the stock market if Trump won the election, the overall stock market rose considerably after the election. Using data on individual stock prices, Alexander Wagner and Alexandre Ziegler of the University of Zurich and Richard Zeckhauser of Harvard conclude that industries like mining and steel and financial firms were relative winners due to the new administration’s promise to resurrect heavy industry and deregulate banking. Firms currently paying high taxes and firms with more cyclical stocks were also among the winners, reflecting an expectation of tax cuts and higher economic growth. At the same time, healthcare, medical equipment, and pharmaceuticals were relative losers, possibly due to the expectation that the Affordable Care Act would be repealed. Trade-dependent firms were also among the losers.

Foreign-born high-skilled workers had beneficial effect on the economy overall, although native scientists negatively affected

Using data for 1994-2001, John Bound and Nicolas Morales of the University of Michigan and Gaurav Khanna of the University of California, San Diego, find that foreign computer scientists employed in the US on H1B work visas increased the overall welfare of US natives, but had significant distributional consequences. On the positive side, the foreign-born scientists contributed to innovation, lowered prices and raised output and profits in the IT sector. On the negative side, the influx of foreign computer scientists decreased wages for US-born computer scientists by 2.6 to 5.1 percent and employment by 6.1 to 10.8 percent in 2001.

Downward revisions to expected productivity growth may be responsible for weak GDP growth

Over the last four years, US GDP growth has been just 2.1 percent per year on average, despite near-zero interest rates. Olivier Blanchard of the Peterson Institute, Guido Lorenzoni of Northwestern, and Jean-Paul L’Huillier of the EIEF suggest that a series of downward revisions to expected productivity growth may have dimmed expectations about the future, decreasing consumption and investment and thus leading to a decline in demand of 0.6 to 1.0 percent a year since 2012. The authors suggest that, as these adjustments to expected productivity growth come to an end, demand may pick up and interest rates may increase substantially.

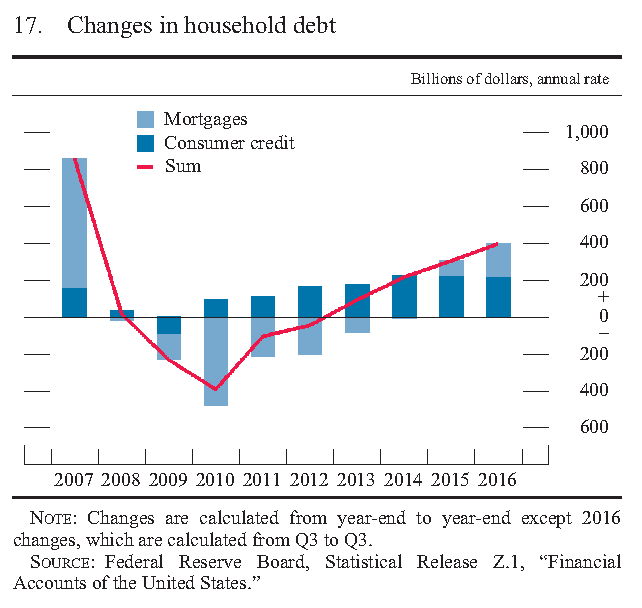

Chart of the week: Consumer credit continues to rise at a modest pace

Quote of the week: “The FOMC has annunciated that its longer run goal is to shrink our balance sheet to levels consistent with the efficient and effective implementation of monetary policy,” says Fed Chair Janet Yellen.

“And while… I can’t put a number on that, I would anticipate a balance sheet that’s substantially smaller than at the current time. In addition, we would like our balance sheet to again be primarily Treasury securities, whereas … we have substantial holdings of mortgage-backed securities. To adjust financial conditions in order to influence economic development in line with our dual mandate objectives, the committee would like to the maximum extent possible to rely on variations in our short-term overnight interest rate. It’s our traditional tool. It’s the one that we have the most confidence in, that markets best understand… and [that] we have the greatest confidence in our ability to calibrate relative to the needs of the economy. We do not want to use fluctuations in our balance sheet policy as an active tool of monetary policy management. What we would like to do is to find a time [to reduce the balance sheet] when we judge that our need to provide substantial accommodation to the economy in the coming years is minimal, when we have confidence that the economy is on a solid course and the federal funds rate has reached levels where we have some ability to address weakness by cutting it.”

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Hutchins Roundup: Stock market, foreign workers, and more

Thursday, February 16, 2016