This analysis is part of USC-Brookings Schaeffer Initiative on Health Policy, which is a partnership between the Center for Health Policy at Brookings and the University of Southern California Schaeffer Center for Health Policy & Economics. The Initiative aims to inform the national health care debate with rigorous, evidence-based analysis leading to practical recommendations using the collaborative strengths of USC and Brookings.

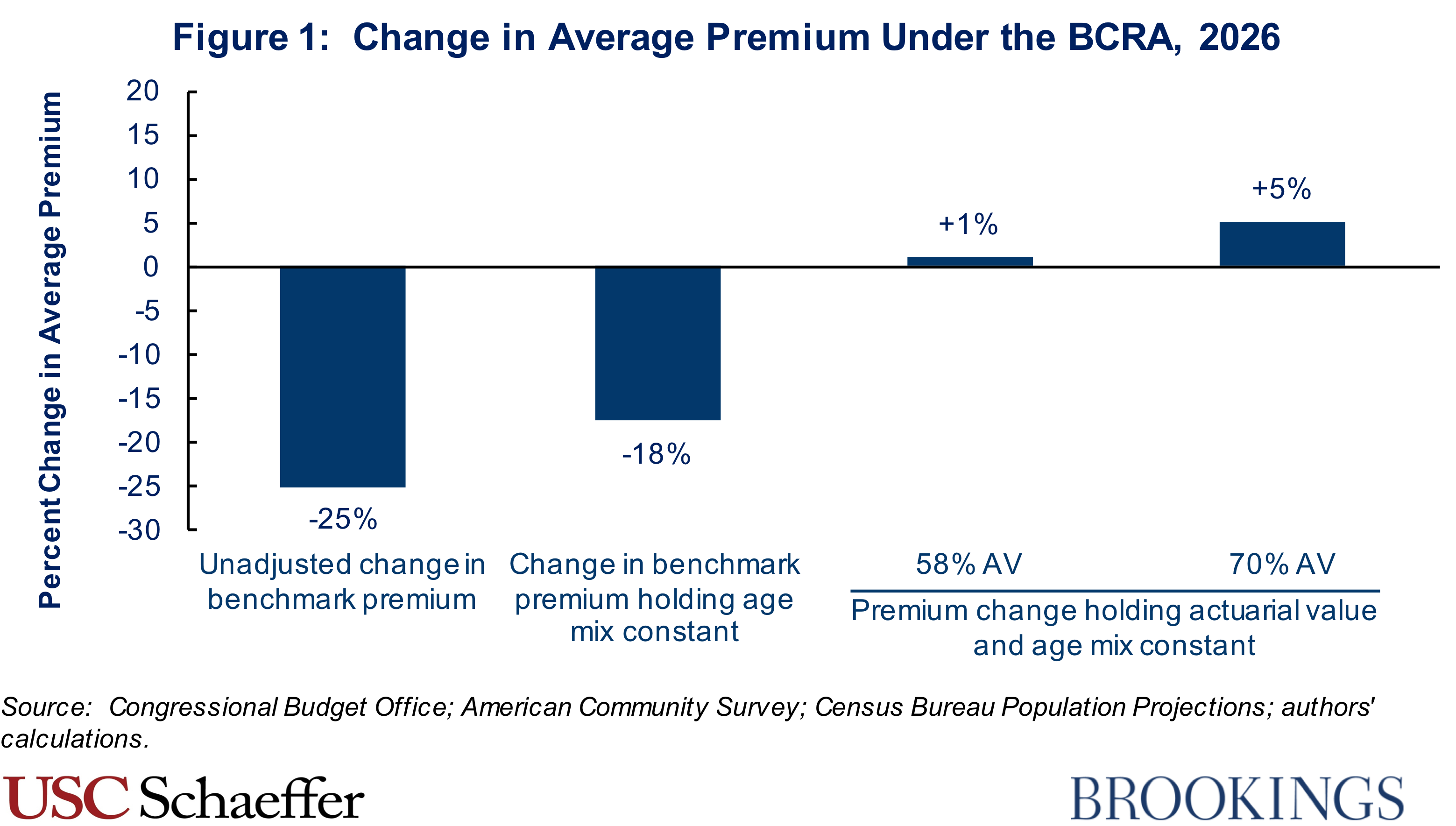

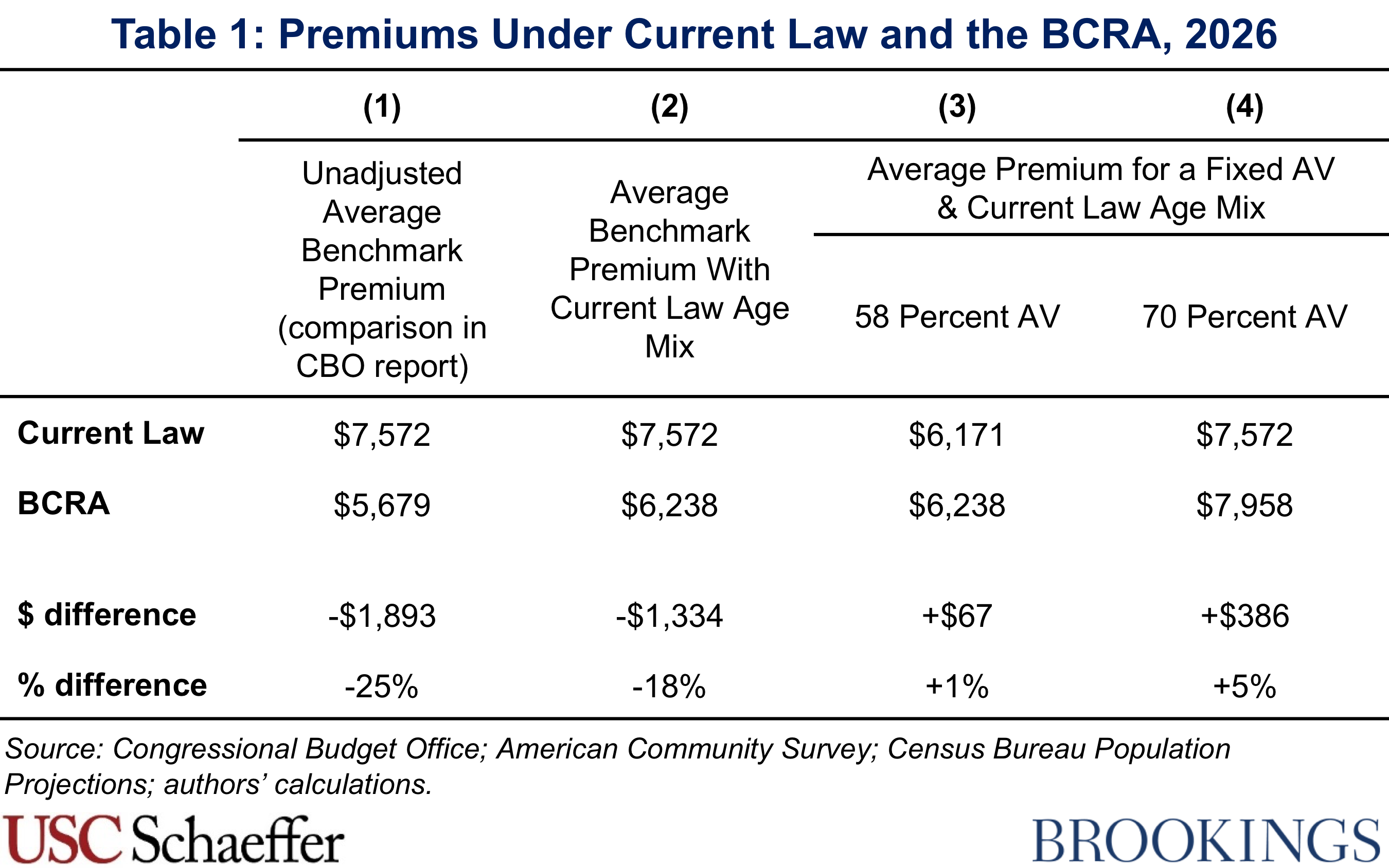

On Thursday, the Congressional Budget Office (CBO) published an analysis of an updated version of the Better Care Reconciliation Act (BCRA), Senate Republicans’ health care legislation, including how the BCRA would affect individual market premiums. In its report, CBO estimated that the average premium for the “benchmark” individual market plan—the plan used to determine the amount of premium tax credits—would be 25 percent lower under the BCRA than under current law by 2026.

But as we noted after CBO analyzed an earlier draft of the BCRA, this estimate must be interpreted with caution. In particular, while this estimate may be of interest if one’s objective is to estimate how the federal government’s cost of providing premium tax credits would change under the BCRA, it does not answer the question of greatest interest to enrollees, which is how the BCRA will affect average premiums for a given generosity of coverage and a fixed population of individual market enrollees.

This is the case for two reasons. First, the BCRA substantially reduces the generosity of the benchmark plan. It directly reduces its actuarial value (AV)—the share of the total cost of covered services that are paid for by the insurance plan, rather than by the individual through cost sharing—from 70 percent to 58 percent, which CBO estimated would increase the deductible in such plans from around $5,000 under current law to around $13,000 under the BCRA in 2026. It would also make it easier for states to narrow the definition of “essential health benefits,” which would narrow the set of services covered by the benchmark plan in many states. Second, by allowing premiums to vary more widely by age and changing the structure of the premium tax credit, the BCRA would drive a significant shift in individual market enrollment toward younger individuals. Since younger individuals pay lower premiums, this shift would mechanically lower the average premium even if every individual’s premium remained the same.

Our earlier analysis showed how supplemental information included in the CBO report could be used to construct more informative premium comparisons. This blog post provides a brief update of that earlier analysis to reflect the new CBO estimates and also examines how premiums would change under the BCRA in the long run. Readers seeking greater methodological detail should refer to our earlier piece.

We find that the current population of individual market enrollees would pay more for the same level of coverage under the BCRA than under current law, before accounting for any premium tax credits for which individuals may be eligible.

We find that the current population of individual market enrollees would pay more for the same level of coverage under the BCRA than under current law, before accounting for any premium tax credits for which individuals may be eligible, as illustrated in Figure 1. Average premiums for a plan with a 58 percent actuarial value would be 1 percent higher under the BCRA than under current law in 2026, holding the individual market age distribution fixed at what it would be under current law. Similarly, average premiums for a plan with a 70 percent actuarial value would be 5 percent higher under the BCRA than under current law, holding the individual market age distribution fixed at what it would be under current law. The main reason these estimates differ from the 25 percent decline in the benchmark premium featured by CBO is that they hold actuarial value constant.

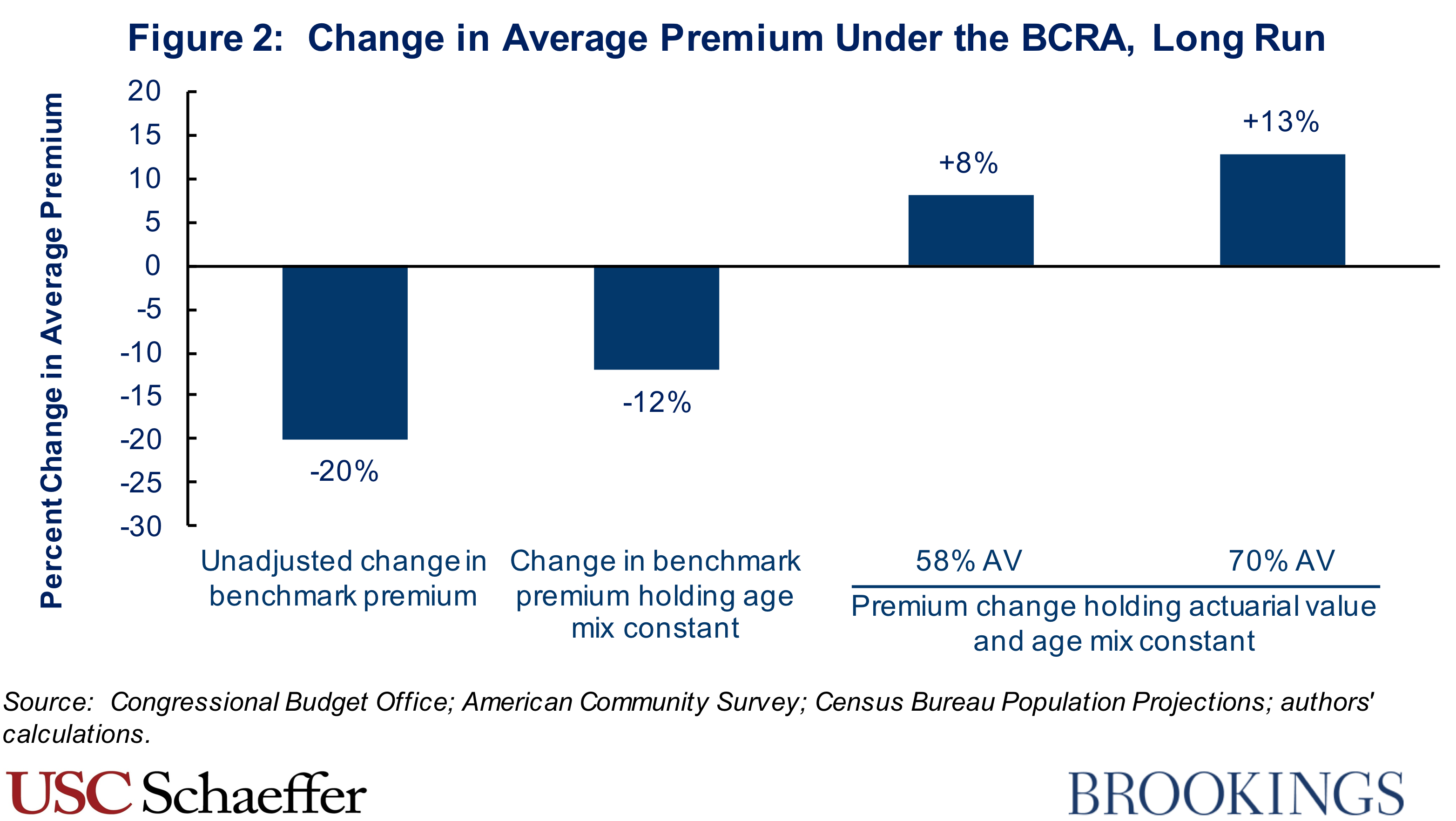

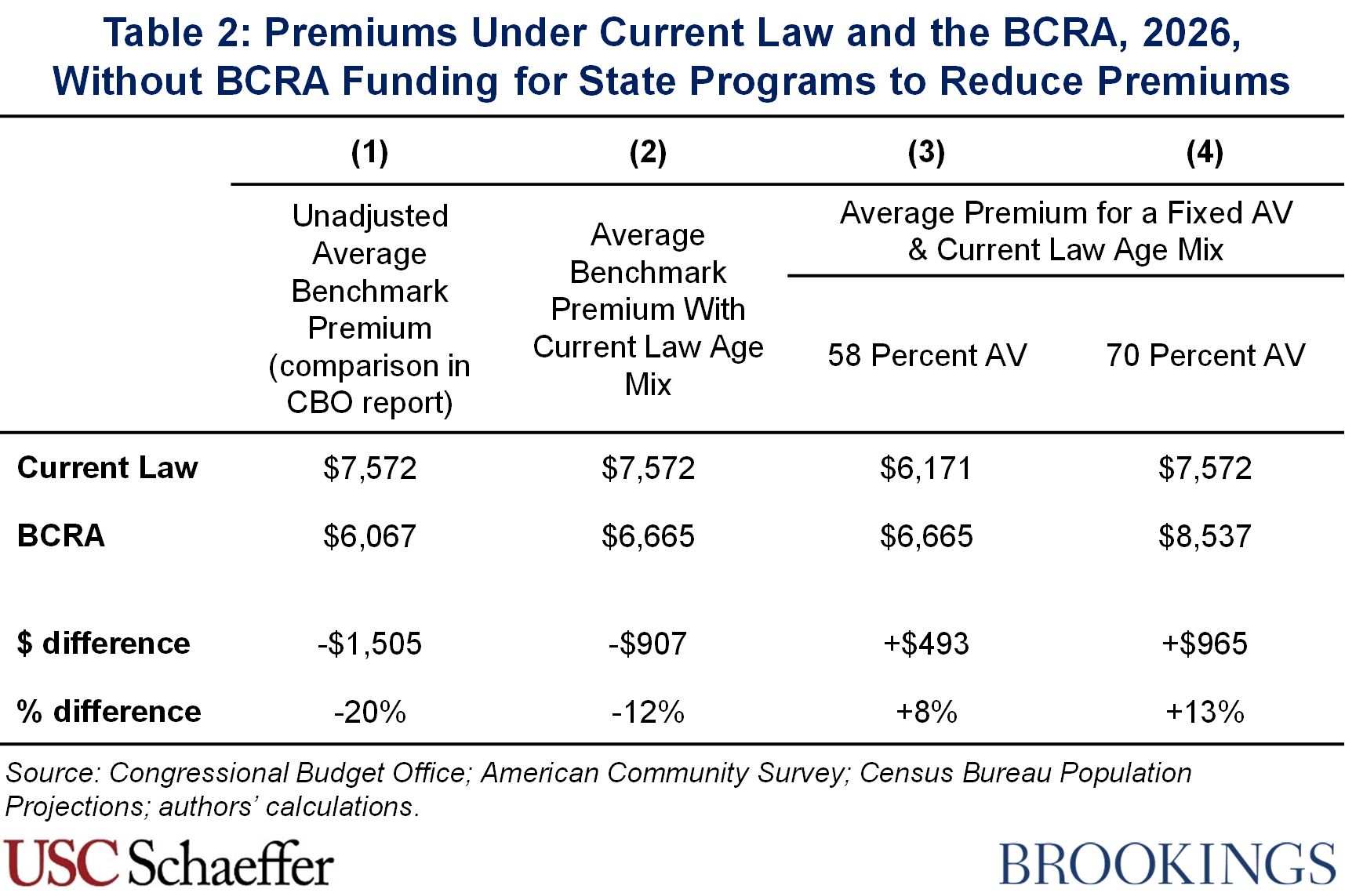

These estimates focus on 2026 because that is the year for which CBO provides detailed premium estimates, and they incorporate the effects of funding the BCRA would provide for state programs to reduce individual market premiums. Because the BCRA does not provide such funding for those programs for years after 2026, these estimates understate the increase in individual market premiums under the BCRA over the long run. The difference between the BCRA’s effects in 2026 and in the long run is larger than in prior drafts of the BCRA because the current draft would provide considerably more funding of this type in 2026 than prior drafts would have provided.

For this reason, to illustrate how the BCRA would affect the long run, we also provide estimates that adjust our 2026 estimates to remove the effects of the state funding. As shown in Figure 2, we find that the long-run increase in average premiums under the BCRA would be 7 or 8 percentage points larger than the increase in 2026. The details of our approach are provided in the methodological appendix.

It is important to note that there are two important respects in which these estimates understate the premium increases that individual market enrollees would face for a plan with fixed generosity.

First, as noted above, the BCRA would make it easier for states to narrow the definition of essential health benefits, causing individual market plans in many states to cover a smaller set of services. Ideally, therefore, we would make an upward adjustment to CBO’s premium estimates under the BCRA, but CBO does not provide the information required to make such an adjustment.

Second, our estimates reflect premiums before accounting for subsidies available to people purchasing individual market coverage. The subsidies available under the BCRA would, on average, be significantly smaller than the subsidies available under current law. As a result, average post-subsidy premiums would increase by considerably more than average pre-subsidy premiums.

The increase in average premiums under the BCRA should not be surprising in light of the fact that the BCRA would repeal the individual mandate and curtail subsidies for people purchasing individual market coverage. Both of these policies would likely reduce individual market enrollment, particularly among the healthy, necessitating higher premiums to cover the claims costs of the worsened risk pool. Our earlier analysis discusses why the BCRA would have these effects on premiums in somewhat greater detail.

Methodological Appendix: Method for Estimating Long-Run Premium Effects of BCRA

As described in the main text, to illustrate how the BCRA would affect individual market premiums over the long run, we present estimates of the BCRA’s effects on premiums in 2026 that remove the effects of the BCRA’s funding for state programs intended to reduce premiums. To do so, we first replace CBO’s estimates of premiums under the current version of the BCRA with its estimates under the prior version of the BCRA, as CBO indicates that the only reason its premium estimates differ between these two versions of the legislation is the additional state funding included in the current version.

We then adjust CBO’s estimate of the prior version of the BCRA to remove the effect of state funding included in that version of the BCRA. We estimate the required percentage increase in three steps:

- Step 1 – Estimate aggregate individual market premiums in 2026: CBO’s estimate of this version of the BCRA, together with its March 2016 baseline projections, indicate that 18 million people would have been enrolled in the individual market in 2026 under the BCRA. We assume, likely conservatively for these purposes, that the average premium would equal the average premium for a plan with a 70 percent actuarial value, roughly the average actuarial value under current law. To derive that premium, we take the estimate of the average benchmark premium under the BCRA from our prior analysis ($6,058) and scale it up by CBO’s estimate of the ratio of premiums for a plan with a 70 percent actuarial value to premiums for a plan with a 58 percent actuarial value (1.28). Multiplying the estimated average premium by estimated enrollment yields projected aggregate individual market premium revenue of $140 billion in 2026 under the BCRA.

- Step 2 – Estimate total outlays for premium-reducing programs in 2026: The prior version of the BCRA would have appropriated $4 billion for its State Stability and Innovation Fund in 2026, of which CBO estimated that three-quarters would be devoted to reducing individual market premiums. Accounting for the requirement for states to provide matching funds equal to 35 percent of total program costs, this implies that the prior version of the BCRA would have generated total outlays on these programs of $4.6 billion for the 2026 plan year.

- Step 3 – Estimate the percentage increase in individual market premiums: Assuming that $4.6 billion in funding estimated in step 2 would be passed through to consumers under the BCRA, this implies that premiums would have been 3.3 percent higher in the absence of this funding. Note that this estimate may modestly understate the effect that removing this funding would have on premiums since the mechanical increase in premiums caused by removing this funding would likely worsen the individual market risk pool, necessitating a modest additional premium increase.

Supplemental Tables and Figures

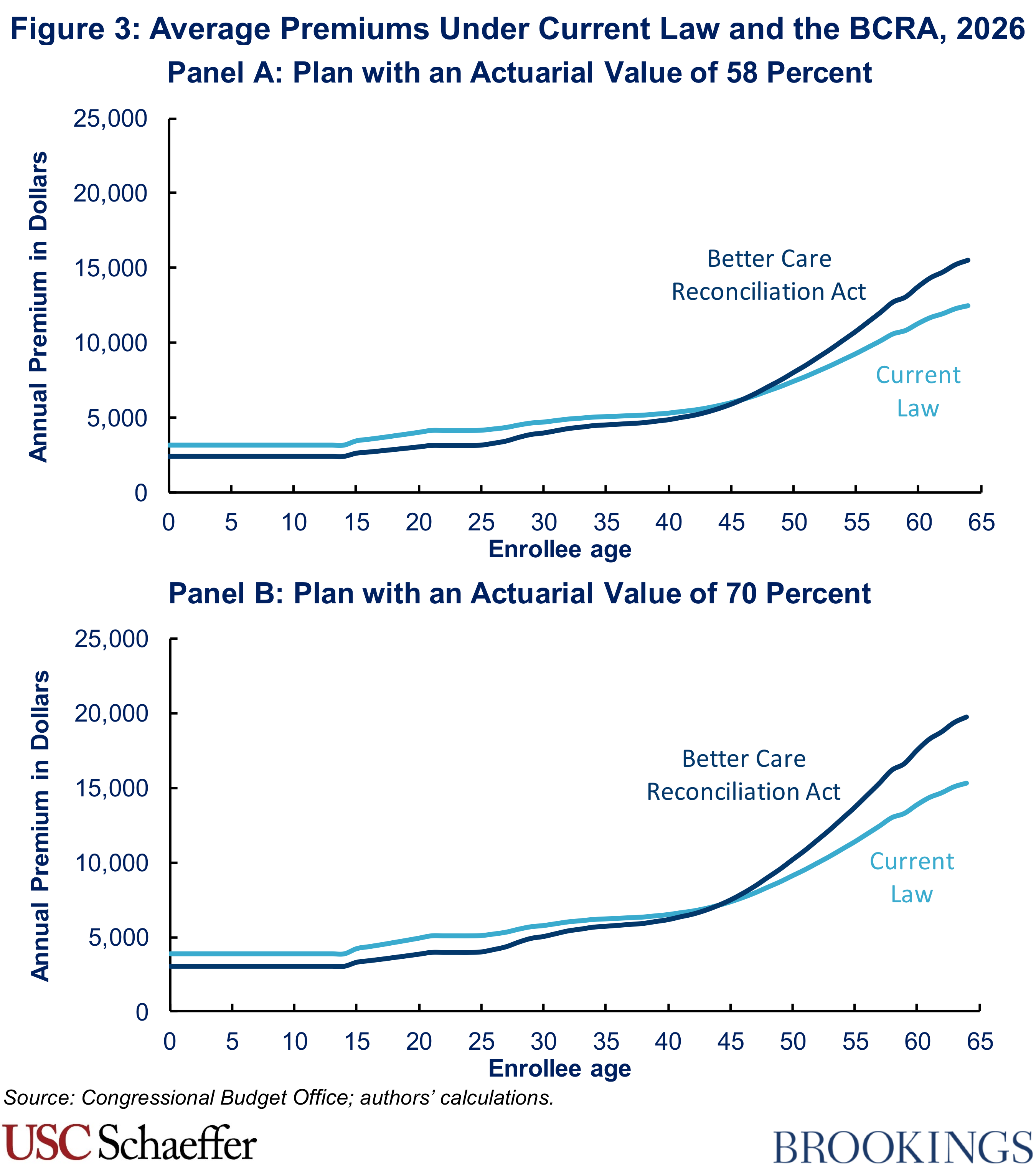

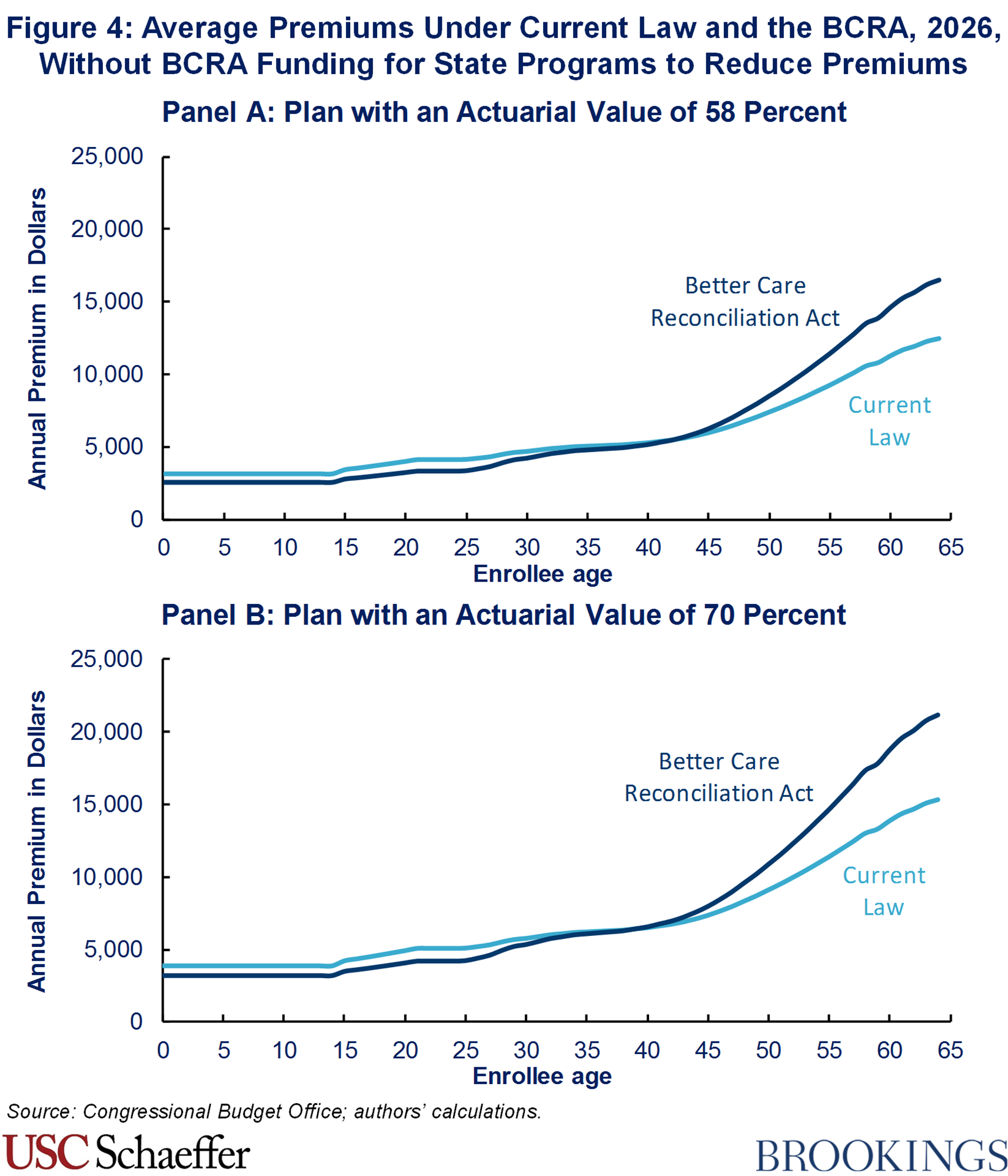

Our prior analysis included a figure illustrating how premiums would change by age under the BCRA, as well as a table reporting the estimates of average premiums that underlie our estimates of premium changes under the BCRA. Updated versions of those figures are provided here for completeness. For additional details on the calculations that underlie these figures, please refer to our prior analysis.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

How would the revised Senate health care bill affect individual market premiums in 2026 and over the long run?

July 24, 2017