Last week, the World Bank released its biannual Africa’s Pulse report that provides an economic update for the region and includes special chapters on international financial flows and productivity in sub-Saharan Africa. The chapter on international financial flows documents a shift in capital inflows from traditional creditors to more direct investment and international bond issuances.

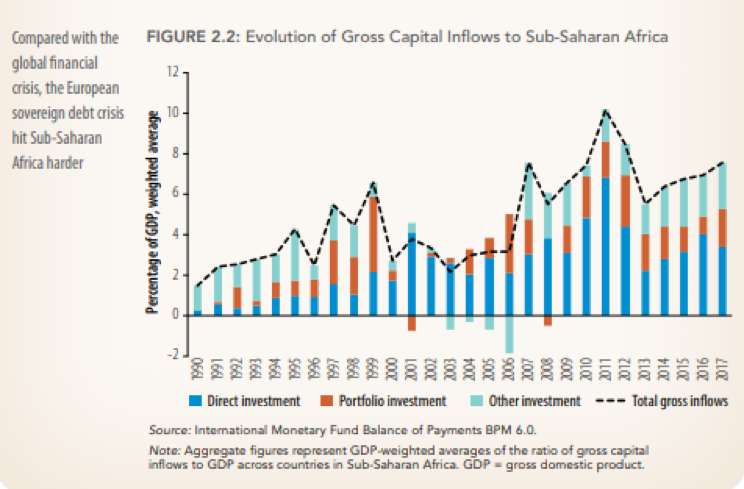

As Figure 2.2 shows, gross capital inflows to sub-Saharan Africa have been increasing for the past few years and were around 8 percent of GDP in 2017. The composition of capital inflows has changed significantly during this period; the average share of foreign direct investment (FDI) in total inflows increased from 24 percent in the 1990s to 75 percent during the 2000s. Nigeria and South Africa, the region’s two largest economies account for 50 percent of FDI and the top 10 countries capture 80 percent.

In recent years, both portfolio (stocks and bonds) and other investments (bilateral borrowing from non-Paris club countries) have increased in sub-Saharan Africa, making up a larger share of total capital inflows. The report attributes the growing share of non-FDI investment sources to external shocks including the 2008-09 global financial crisis, 2011-12 European debt crisis and the 2014 oil price shock. The first two shocks led the region’s transition away from traditional development partners (Paris club) toward China and private creditors. Subsequently, the low interest rate environment and the oil price crash in 2014, which led many countries to increase borrowing from international debt markets, also contributed to the increasing share of portfolio and other investment sources in total capital inflows.

The report also includes regression analysis on the determinants of capital flows, finding that countries with higher economic growth, strong fiscal discipline, and more trade and financial openness had higher capital inflows. Using this analysis, the report recommends developing local financial markets to attract investment in domestic financial instruments. Further, improving the business environment can create investment opportunities for foreign and domestic investors. Lastly, for commodity dependent countries, diversifying the economy can help reduce growth shocks from commodity price swings, leading to a more stable investment environment.

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Figure of the week: Capital inflows in sub-Saharan Africa

October 12, 2018