Recent policy proposals, including one from the Harris-Walz campaign, have called for expanding coverage of in-home assistance with basic tasks that often become more difficult as people age, such as eating, bathing and dressing independently, to all Medicare beneficiaries with established care needs.

In addition to addressing care needs that are often unmet or handled by unpaid family members, this type of program could help households more efficiently manage risks at older ages, expand the productive capacity of the economy by providing more flexibility to would-be unpaid caregivers, and potentially reduce reliance on other public programs.

The growing number of people with long-term chronic conditions need support

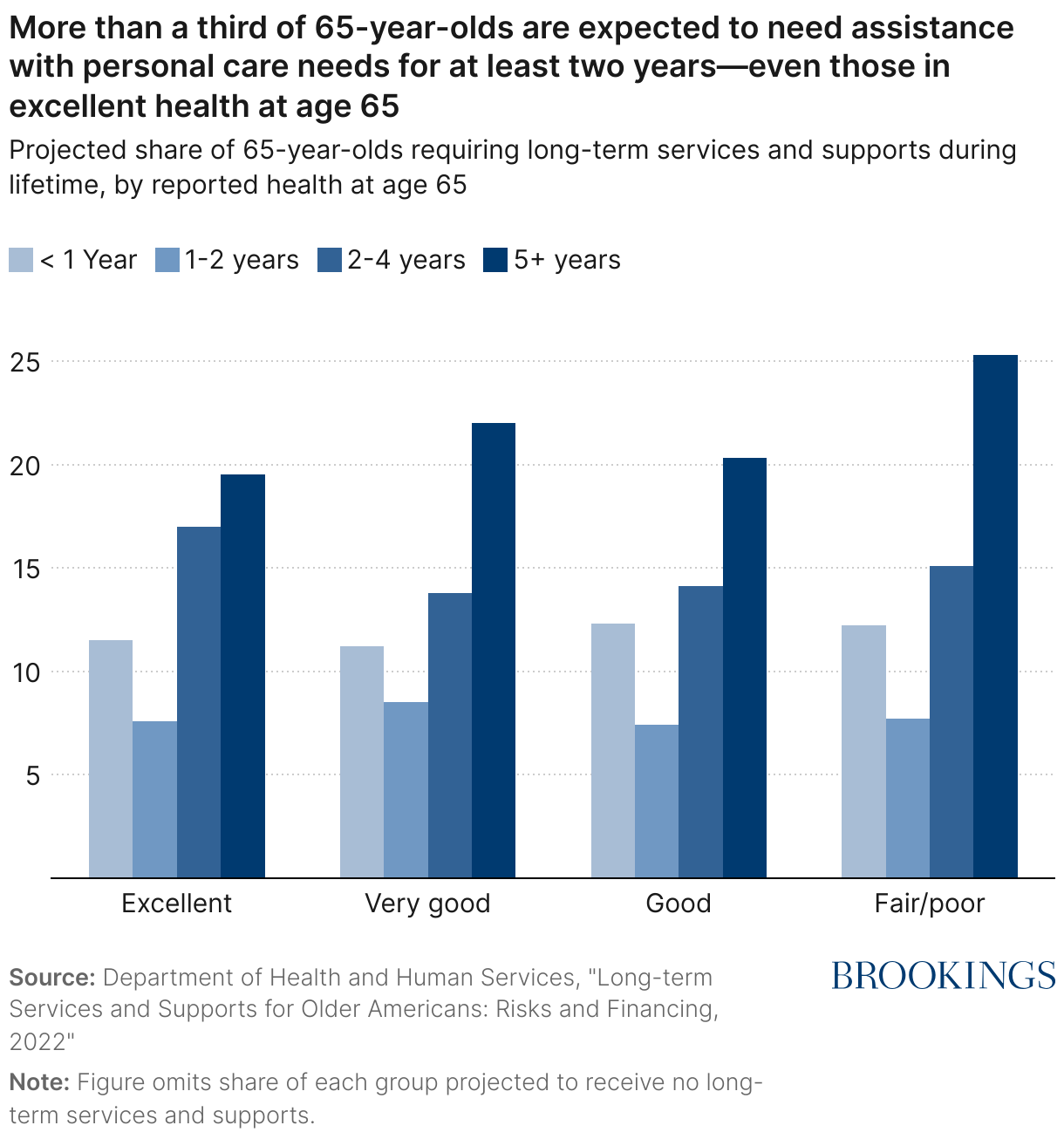

Many older Americans need assistance with “activities of daily living” such as bathing, eating, and dressing or suffer from severe cognitive impairment that requires close supervision. For some, this need is short-term in nature and results from an injury or hospitalization. For others, the need arises due to a long-term chronic condition like Parkinson’s disease or dementia and persists or grows with disease progression. Recent estimates suggest that over half of people turning 65 will develop a disability that will require assistance with personal tasks, and one in three will require assistance for two years or more—even those reporting excellent health at age 65 (see Figure 1). And due to a variety of different demographic trends, the population needing care is likely to grow over time.

While Medicare—the public health insurer for those over age 65 and individuals with long-term disability—covers many aspects of medical care, assistance with basic personal tasks is generally only covered for rehabilitative purposes over a short period of time or for those who are home-bound. Thus, those who need assistance over a longer period must finance these costs through alternative channels, and many do so out of personal savings as private insurance for long-term care is limited and dwindling. Once those with limited incomes have nearly exhausted their savings, they may qualify for Medicaid, the public health insurer for those with limited means.1

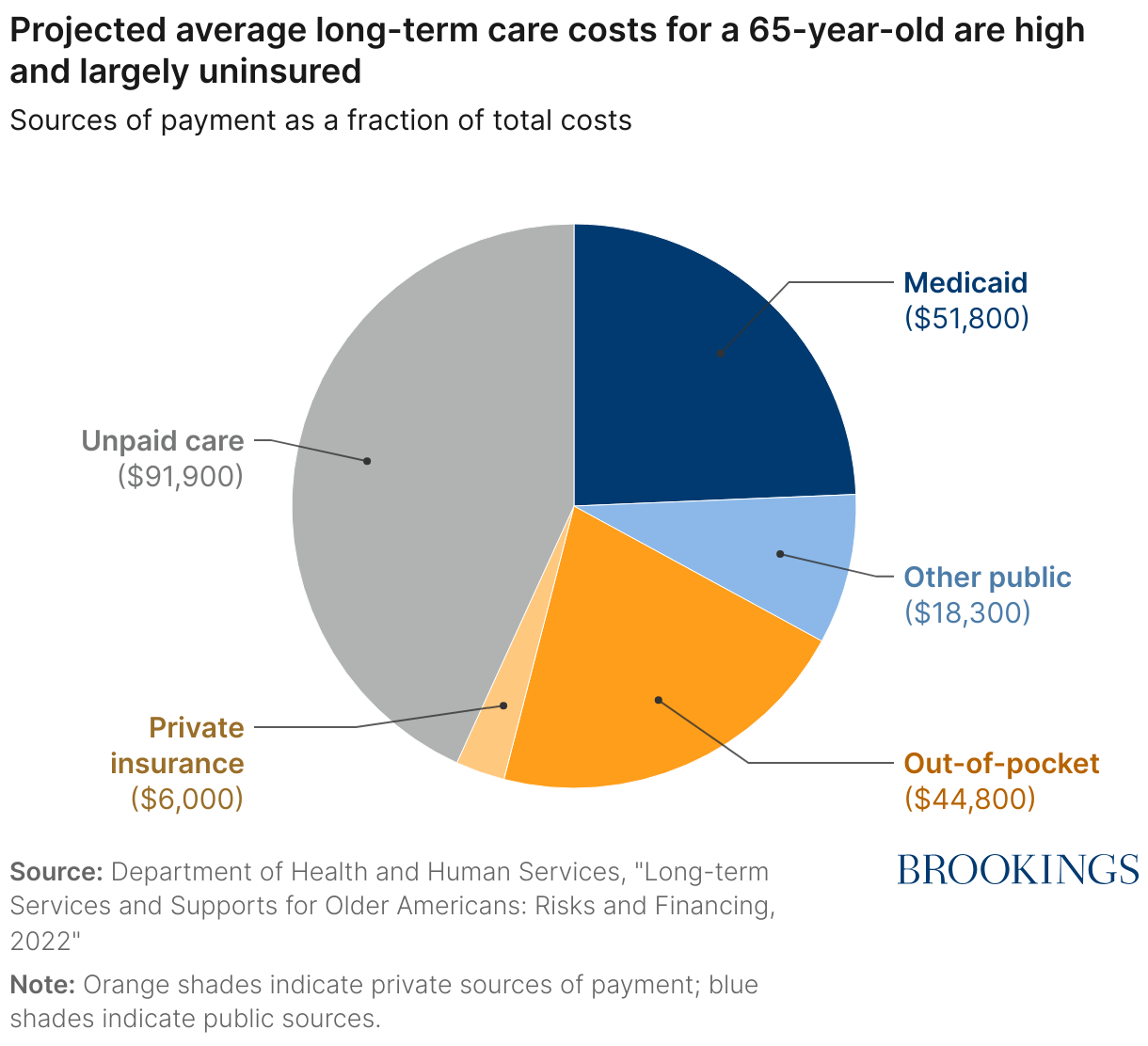

A great deal of long-term care is provided by spouses, children, and other unpaid relatives or friends. Recent estimates put the value of this unpaid care at approximately $150 billion annually in forgone wages of unpaid caregivers,2 but—similar to child care provided by parents—neither this amount nor any potential reduction in these “costs” show up in economic statistics. In addition, the figure above doesn’t take into account the impact that caregiving has on the health and well-being of the caregiver, which would drive up the implied cost of this care even further.

All in all, a 65-year-old is, on average, projected to incur $120,900 in paid care and receive unpaid care worth approximately $91,900 over their lifetime (see Figure 2). The value of unpaid care represents 44% of total projected costs, out-of-pocket expenditures are 21%, and Medicaid pays 24%. Less than 3% of costs are projected to be paid for by a private insurance policy.

The Harris-Walz plan calls for “sliding scale coverage,” where beneficiaries with lower levels of income and wealth pay a smaller share of costs than higher-income and wealthier beneficiaries. Eligibility for services would be determined by an independent evaluation of functional limitations and cognitive impairment, and covered services would include those provided by a licensed professional.

Importantly, these proposals include in-home care as a benefit for all Medicare beneficiaries, not just those who would qualify under the much more stringent asset and income requirements of the Medicaid program. The Kaiser Family Foundation estimates that approximately 15 million Medicare beneficiaries would be eligible for the new benefit based on reported levels of functional limitations in the 2022 Medicare Current Beneficiary Survey.

What are the potential consequences of expanding coverage for in-home care?

Expanding Medicare to provide coverage for home care represents a new benefit with new costs. Estimates of adding this benefit approximate $40 billion per year, representing roughly a 4% increase in annual Medicare expenditures. What would the potential impacts of this policy be? This section explores the broader economic impacts of this program, referring to prior evidence when available.

Amount and type of care utilization

Expanding coverage of paid home care would likely increase the use of paid in-home care because of moral hazard—that is, insured individuals will use more in-home care than they otherwise would have if they were paying the full price. For instance, private long-term care insurance has been shown to increase utilization of paid home care.3 While some of the increased utilization may be among those who only use care when it is subsidized, some may also reflect unmet need.

At the same time, the body of evidence suggests that expanded in-home care will reduce some unpaid family and friend care. For example, when Medicare reduced payments for home care for rehabilitative purposes, paid home care use declined and care from family and friends increased; acquiring private long-term care insurance caused higher-income parents to reduce expectations that their adult children would care for them in the future; and public home care provision reduced unpaid care from spouses and adult children for low-income families.4 In addition, slightly more older adults prefer to be cared for by paid providers at home than by unpaid family and friends.

Finally, expansion of home health care could help people that might otherwise go to a nursing home remain in their communities. Recent evidence indicates that increased Medicaid home care spending significantly reduced the use of nursing facilities. However, past expansions of home health care that were not well targeted to those at risk of entering a nursing home did not find similar effects. While unlikely, an expansion of Medicare coverage for paid care could also lead individuals living in nursing homes to transition back into the community.

Labor force participation and co-residence of unpaid caregivers

Because an expansion of Medicare to cover home care can reduce the reliance on unpaid caregivers, it may also increase flexibility among people who may have provided unpaid care in the absence of the expansion. These would-be caregivers may make larger investments in their careers and take opportunities in different geographic locations than they would have if they thought they were likely to be relied upon as a source of care. Subsidies for private long-term care insurance and the provision of paid home-care by Medicaid have been found to increase the labor market attachment of adult children and decrease the likelihood they reside with their parents. Increased work effort would also increase tax collections, offsetting part of the costs of the Medicare home care program.

Risk protection

Insurance provides financial protection in states of the world when covered individuals incur a shock, which is valued by risk averse individuals. This financial protection is valuable: One estimate valued the financial protection against out-of-pocket expenditure risk at almost 40% of the social costs of the Medicare program.5

By covering a portion of the costs incurred when a Medicare beneficiary needs long-term care services, the financial risk protection of the Medicare program improves. Coverage for paid home care protects people against a very undesirable outcome, where people exhaust most of their resources paying for long-term care and then quality for Medicaid.

This improvement in risk protection is important, as it means that retirees can get by on less than they would need otherwise. Many retirees know that they can expect to pay in full if the need for long-term care arises and set aside assets for the worst-case scenario. If they could instead insure this risk, there would be less of a need for amassing large amounts of retirement wealth and existing assets could be stretched farther in retirement.

Impact on the private insurance market

Any public form of insurance provided or offered by the government can impact related private insurance markets. For example, if the government expands health insurance coverage, some of those newly eligible will drop their existing private insurance policy, possibly leading to government costs and impacts on private insurers.

In the case of long-term care, the market for private insurance is small and shrinking. The National Association of Insurance Commissioners reports that the number of insured lives was approximately 6.6 million in 2018, down from a peak of 7.4 million in 2012, and the number of companies selling new policies has declined. While there are both demand-side and supply-side reasons for this decline, one factor is that because Medicaid acts as a payer of last resort, it is not advantageous for almost two-thirds of the wealth distribution to purchase private long-term care insurance.

How would a Medicare in-home care benefit impact the private insurance market? Given that the private insurance market is already limited, an expansion of Medicare into home care provision is unlikely to have a large impact. It may also improve the functioning of the private market if insurance companies develop innovative “top-up” plans that offer less downside risk to the insurer.

Health care utilization and spillovers to other government programs

In theory, expanded access to paid home care could also impact overall health care utilization. If paid caregivers prevent those with functional limitations from falling or acquiring other acute health care conditions, a reduction in overall Medicare expenditures could partially offset the costs of expanded coverage. While there is some evidence that Medicare payments declined overall when patients were discharged from the hospital with support from a home health aide rather than to a skilled nursing facility, the study also found higher rates of re-admission and may not generalize to other scenarios. There is also some evidence that private long-term care insurance results in lower enrollment in Medicaid and the Supplemental Nutrition Assistance Program (SNAP). More research in this area would be helpful.

Supply of care workers

Depending on how a new in-home care benefit would impact care utilization, it is possible that demand for direct care workers would increase and that these demands would not be met by the existing supply of workers. Strengthening the direct care workforce should be an important consideration as the details of the plan are worked out: If the hourly rate that Medicare pays home care workers is at or below the rates that Medicaid currently pays, the supply of home care workers is unlikely to expand, and access to care among Medicare beneficiaries may not improve. Other important factors are the training and licensing requirements that would need to be met by direct care workers to qualify and ensuring labor markets for home health care workers are competitive. Increasing levels of legal immigration could also be helpful in meeting the greater demand needs.

Conclusion

The introduction of Medicare in 1965 provided valuable health insurance coverage to seniors, a need that the private market had been unable to meet. However, as in all aspects of policy, the needs of the population the program serves have evolved, and the program has evolved with these changing needs. For example, prior to the Medicare Modernization Act of 2003 that was signed by President George W. Bush, Medicare did not provide coverage for prescription drugs, which had a much more limited role in health care in 1965. This amendment to the Medicare program created a new entitlement to prescription drug coverage in response to the growing use of prescription drugs that were becoming harder for seniors to afford. This program has been found to increase prescription drug coverage and expenditures, some of which has been offset by reduced medical costs, and improve the financial protection of the elderly.

Similarly, long-term care was not an important form of care at Medicare’s founding, but the expenditure risks associated with long-term care are one of the biggest financial risks facing retirees today. Expanding Medicare to cover in-home care for beneficiaries with functional and/or cognitive disabilities, as proposed in early October 2024 by the Harris-Walz campaign, would mark a “once in a quarter century” change to the program that would improve risk protection, reduce out-of-pocket costs, and expand access to in-home care for about 25% of Medicare beneficiaries, filling gaps in long-term care affordability and insurance coverage. However, the program should ensure that the paid home care workforce expands to meet its higher demands and that costs are sustainable over time.

Related Content

Authors

-

Acknowledgements and disclosures

The Brookings Institution is financed through the support of a diverse array of foundations, corporations, governments, individuals, as well as an endowment. A list of donors can be found in our annual reports published online here. The findings, interpretations, and conclusions in this report are solely those of its author(s) and are not influenced by any donation.

-

Footnotes

- Medicaid is a state-administered program that is required to provide nursing home care to those who are eligible, but most coverage for home- and community-based services is optional and varies widely across states.

- The value of unpaid care is less, approximately $100 billion, if using the median or mean wage rate for a paid caregiver rather than forgone wages of the unpaid caregivers themselves.

- There is no evidence that demand for nursing home care increases due to private insurance coverage or more generous coverage from Medicaid. The finding that reducing the price of paid care increases paid care at home and not nursing home care is consistent with the idea that most older adults and adults with disability prefer to remain at home.

- However, one study suggests that increased professional assistance increases unpaid care from adult children.

- The social costs of the Medicare program include the inefficiency costs of raising public funds to pay for the program through the tax system and inefficiencies resulting from potential overuse of medical care through moral hazard.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Expanding in-home care coverage is a needed evolution of Medicare

October 28, 2024