This article is part of the Brookings Center for Sustainable Development compendium “Innovations in public finance: A new fiscal paradigm for gender equality, climate adaptation, and care.” To learn more about the compendium’s chapters, cross-cutting themes, and policy-relevant insights, see the “Introduction: Six themes and key recommendations for embedding gender equality, care, and climate in fiscal policy.”

Introduction

Integrating a gender lens in a federal budget of an emerging country context is not easy, as it is a clarion call to go “beyond the gross domestic product (GDP)” paradigm. Gender budgeting, a macro-fiscal tool to tackle gender inequalities, has been increasingly recognized for its efficacy for fiscal transparency and accountability. Establishing the equity and efficiency aspects of gender budgeting is as crucial as convincing stakeholders of its importance from a human rights perspective. In India, the Ministry of Finance institutionalized gender budgeting in 2004-05 through two mandatory measures: issuing a budget circular (a call circular at the beginning of the budget cycle instructing fiscal agents on how they place their “demand for grants” to the finance minister) and publishing an annual expenditure profile statement.1 Implementation was supported with analytical matrices developed by researchers at the National Institute of Public Finance and Policy (NIPFP), under the Ministry of Finance.2

While in many countries, gender budgeting remained outside the purview of the Ministry of Finance—often led instead by civil society organizations playing a role in demystifying the budget for women—India has developed a credible, government-led initiative that has produced time-series data on gender budgeting since its inception. The availability of time-series data has enabled researchers to analyze the efficacy of gender budgeting on gender equality outcomes. Empirical evidence has shown that gender budgeting is linked to a decrease in violence against women, as well as a reduction in gender disparities in educational outcomes.3

The gender budgeting experiments have been carried out within the overall macro-fiscal rules framework of India, where it is instructed to undertake fiscal consolidation by maintaining the fiscal deficit-to-GDP ratio at 3% and with a “golden rule” of phasing out the revenue deficit. In the post-pandemic period, although a minor deviation occurred in the threshold ratios of the fiscal deficit-to-GDP ratio, the challenge of maintaining expenditure for gender budgeting within the rules-based fiscal framework persisted.4 However, a positive aspect is that gender budgeting has not faced any significant reductions; rather, it has maintained a steady and consistent ratio of the overall budget until recent times.

India provides an interesting study of the impact of fiscal policy on women and men, given its fiscal structure. Revenues are largely raised at the central or union level, but many major public expenditures are at the state and local levels.5 This asymmetry in the allocation of expenditure and revenue within India has created vertical imbalances in the fiscal relations among different levels of government. Intergovernmental fiscal transfers (IGFT) aim to tackle these fiscal imbalances. With the advent of fiscal decentralization, gender budgeting experiments have also gained momentum at the subnational government levels in India, using the same methodology and analytical matrices used at the national level.

This chapter provides an in-depth examination of how gender budgeting operates within India’s macro-fiscal framework, highlighting its role in advancing equity, fiscal transparency, and accountability. It is organized as follows: Section 1 sets out the macro-fiscal framework and its implications for fiscal space. Section 2 analyzes the incidence of revenue and expenditures to assess distributional outcomes. Section 3 examines the institutionalization and practice of gender budgeting in India, with attention to its effectiveness and limitations, and Section 4 presents the conclusions and policy lessons.

1. The macro-fiscal framework

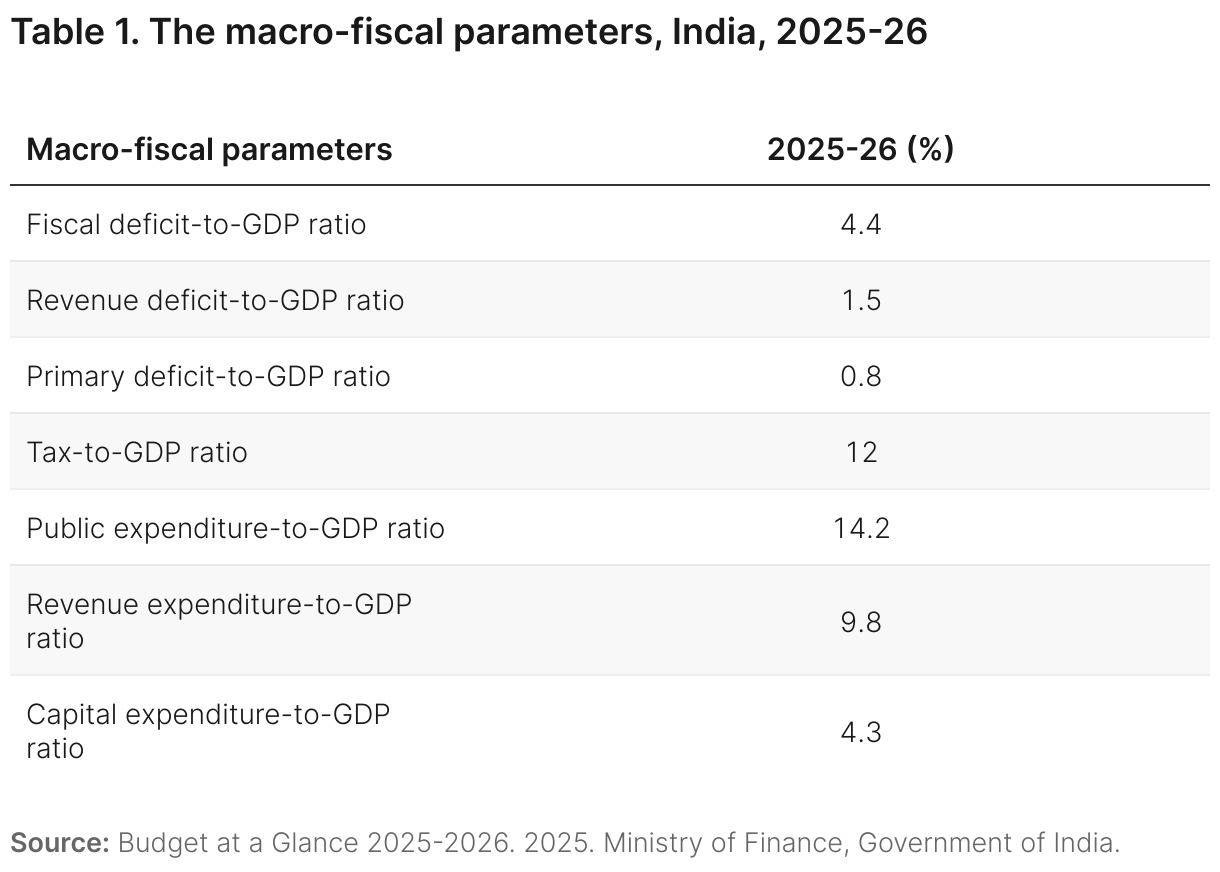

In the post-COVID fiscal strategy, India has continued to run high debts and high deficits, but the fiscal deficit-to-GDP ratio was brought down from 9.2% in 2020-21 to 4.4% in 2025-26.6 Fiscal rules in India stipulate that the fiscal deficit-to-GDP ratio of subnational governments should remain at 3.5%. The 2025-26 Union Budget reflects a goal of fiscal consolidation by setting a target of reducing the debt-to-GDP ratio to 50% (±1%) by 2030-31 (see Table 1).7 This target has implications for gender budgeting, depending on whether fiscal consolidation happens through expenditure compression rather than through revenue mobilization. While the government has pursued fiscal consolidation through expenditure cuts to meet deficit targets, allocations for gender budgeting have remained relatively protected. From 2004–05 to present, these allocations have not faced significant reductions, signaling a degree of policy commitment even under fiscal constraints.

The public expenditure-to-GDP ratio is 14.2%, while the tax-to-GDP ratio is 12%. Revenue stability is crucial for expenditure design (Table 1). In 2025-26, the revenue resource gap was financed through bond financing.8

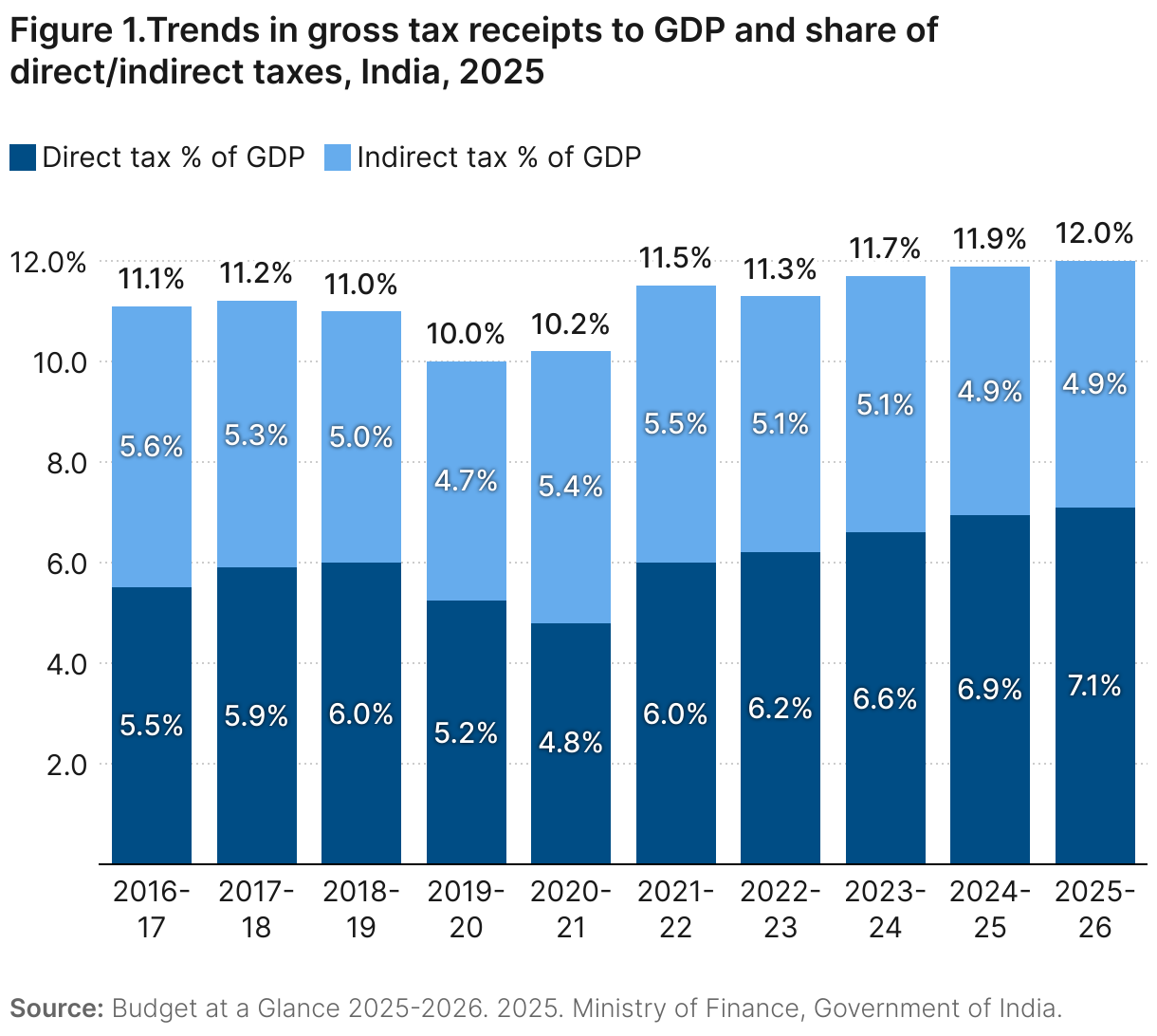

In India, the overall tax-to-GDP ratio has been increasing from 10.2% in the COVID-hit year to 12.0% by 2025-26 (Figure 1). The direct tax-to-GDP ratio, mainly from corporate income and personal income taxes, grew to 7.1%, while indirect taxes, mainly the Goods and Service Tax (GST), decreased marginally to 4.9% (Figure 1).9

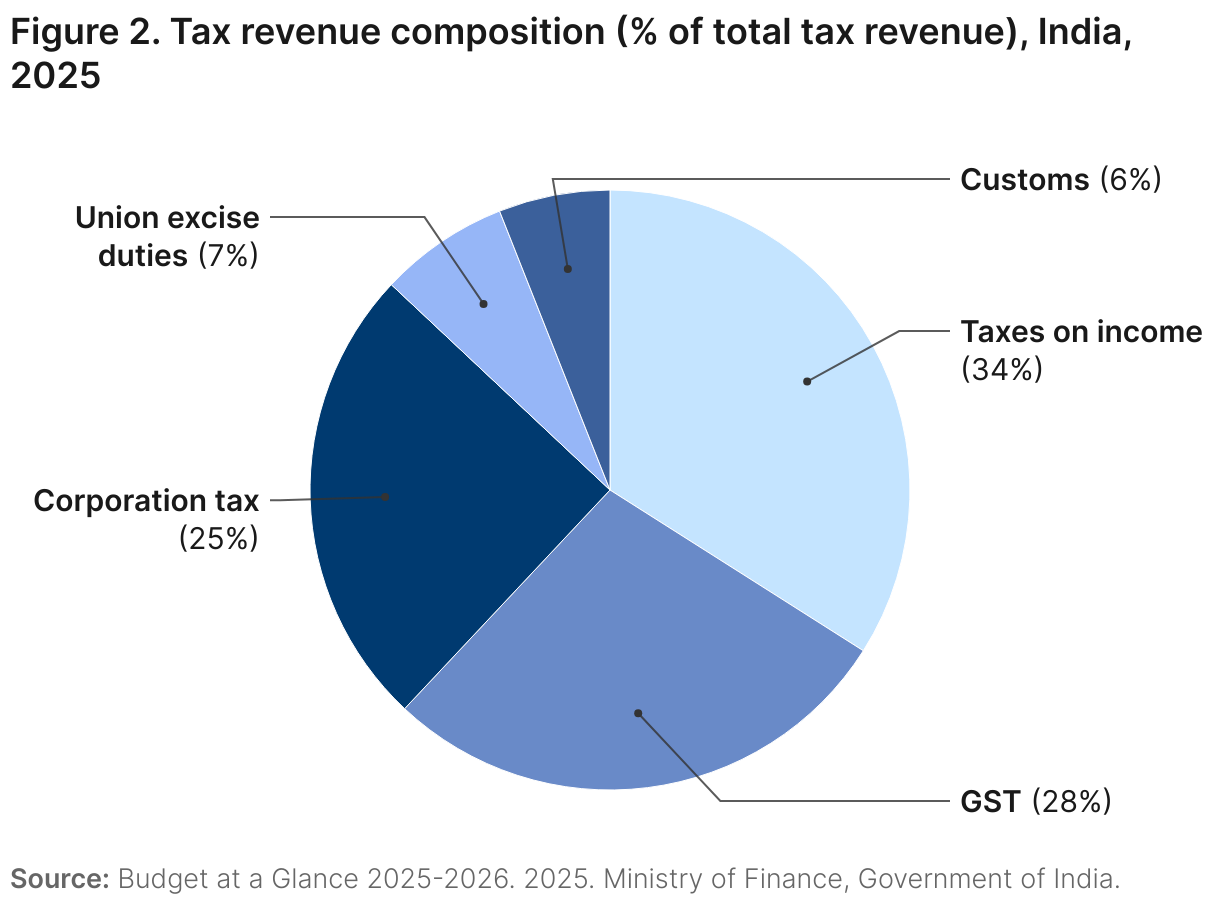

Income tax and corporate taxes contribute 34% and 25% respectively, while GST contributes 28% of total tax revenue. Union excise taxes and customs (taxes on imports) are insignificant at 7% and 6% respectively (Figure 2).10 Revenue policies at both national and sub-national levels address gender inequalities in different ways. Women were once granted exemptions under the personal income tax, though these were later revoked, and direct taxes are filed individually rather than jointly.11 In some provinces, property taxes are applied at differential rates for women property owners.

As noted above, India has a decentralized fiscal system. In fiscal federalism, tax transfers constitute a significant source of revenue for expenditure by subnational governments. According to Stotsky et al. (2019), “IGFTs account for more than half of state revenues.”12 Because Indian states have different administrative and technical capacities for raising local taxes and funding public expenditure, intergovernmental transfers can play a role in helping lower-capacity states. At the same time, fiscal federalism, with its inherent differences in revenue and expenditure assignments, may also result in both vertical and horizontal inequalities in the delivery of public services.

2. Incidence analysis of revenue and expenditures

Several studies have examined the incidence of taxation and public expenditure, but these have been carried out as independent exercises and not well-linked to gender budgeting exercises. Several studies have examined the impact of India’s tax system on women and men. One tax incidence study in 2010 showed that while tax structures are formally gender neutral, in practice, they reinforce existing economic inequalities.13 Indirect taxes are regressive, as women in low-income households spend a larger share of their resources on taxed essentials and therefore shoulder a disproportionate burden of consumption taxes. Structural biases in inheritance-related tax laws have historically restricted women’s ownership of property and narrowed their participation in the tax base.14

To address this disparity, some states and city governments in India have implemented tax incentives and additional preferential measures to promote property ownership among women.15 Analyses of these revenue policies—the stamp duty (a property transfer tax) and property tax discounts—show mixed results. Stamp duty discounts available to women seemed to have increased their property ownership (but not necessarily their control over property) while recurrent property tax discounts did not, and both measures had a limited impact on subnational revenues.16 The solution to overall gender inequality may therefore not lie within the tax system. Rather, strengthening women’s property rights, building up gender-based data sets in taxation, and institutionalizing gender-disaggregated incidence analysis in taxation may yield other ways to address gender disparities.

Conducting public expenditure benefit incidence analysis (BIA) is crucial to understanding the distributional impacts of spending. However, the non-availability of data thwarts BIA for many sectors. For instance, in the case of the health sector, BIA conducted by Chakraborty et al. (2012) showed that while health subsidies are sometimes progressive across income quintiles, they are inequitable across men and women.17 Men capture larger subsidies because they use more inpatient and tertiary care, where per-patient public spending is higher, while women rely more on preventive and maternal health services, which carry lower subsidies. The gender gap arises from several mechanisms, including lower female mobility, weaker decisionmaking power, concentration of spending on hospital services, and underinvestment in community-based care accessible to women. Policy implications include the need for gender-disaggregated BIA, greater investment in primary and preventive services, and the institutionalization of gender budgeting in health financing.18 Overall, the empirical evidence shows that while India’s public health spending has pro-poor aspects, it remains insufficiently gender-sensitive, and addressing these disparities is crucial for advancing both equity and efficiency.

The political economy of gender budgeting is also crucial for better gender equality outcomes. Political will, institutional anchoring within the Ministry of Finance, and advocacy by women’s movements shape the introduction and survival of gender budgeting in a country.19 Unlike welfare-targeted schemes or freebies, gender budgeting is framed as a mainstream fiscal tool embedded in the budget process, intended to ensure that allocations and outcomes across sectors address gender inequalities. Empirical analysis shows, however, that while gender budgeting has generated awareness and transparency, its linkages with planning and fiscal outcomes vary across states. States with strong budgetary institutions and sustained political commitment, such as Kerala and Karnataka, have been able to integrate gender budgeting into planning and expenditure tracking. The political economy perspective thus underscores that gender budgeting’s effectiveness depends not only on technical tools such as incidence analysis but also on institutional incentives and broader fiscal federal dynamics.20

3. Gender budgeting in India

Generally, gender budgeting should be conducted within the overall framework of fiscal policy. As Chakraborty (2024) points out, “this includes budgetary allocations, actual expenditure, taxation, fiscal decentralization and ex-ante gender budgeting and fiscal devolution (IGFTs).”21 In India, the revenue side of gender budgeting is still in its early stages. Moreover, the literature on gender budgeting, as Chakraborty (2022) notes, “has largely dealt with budget allocations and/or expenditures in isolation from the overall fiscal policy framework, with a few exceptions in India, Mexico, Morocco, the Philippines, and South Africa, where studies within the framework of fiscal decentralization have been undertaken.”22 As a result, most gender budgeting analyses remain confined to the analysis of public expenditures rather than other aspects of fiscal policy.

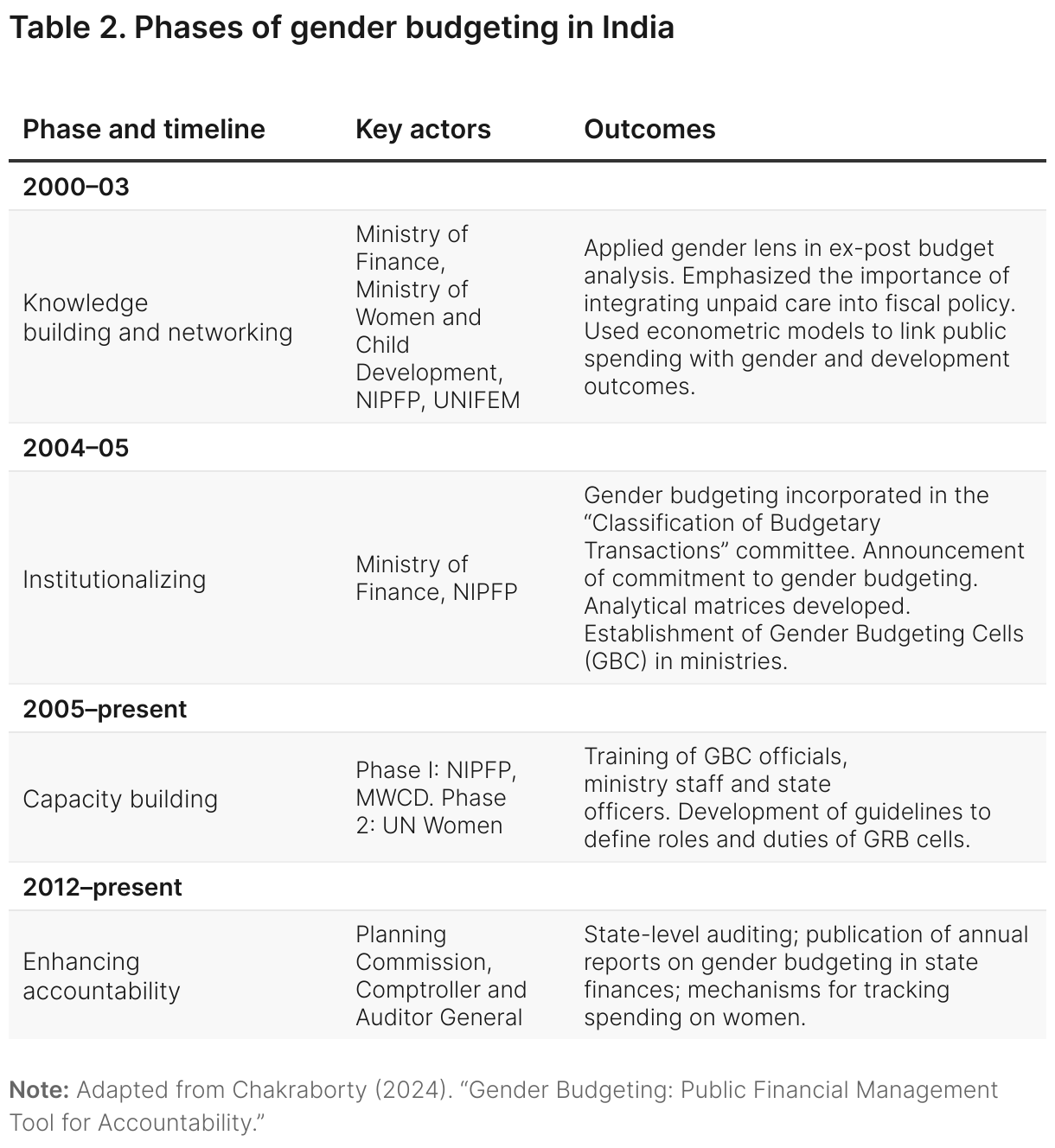

As a fiscal innovation, gender budgeting comprises four stages: knowledge building, creating institutional structures, capacity building, and installing accountability mechanisms.23 Table 3 displays the phases of gender budgeting in India.

3.1 India’s four phases of gender budgeting

In India, the first stage of gender budgeting began in 2000 when the government commissioned the NIPFP to develop an analytical methodology. The study that NIPFP prepared, “gender diagnosis and budgeting,” established the first chapter on gender in the Economic Survey of India and was tabled in the Indian Parliament a day before the Budget Speech in 2001. Meanwhile, Indian states were asked to prepare gender budgets using the NIPFP methodology.24 These processes required “institutional mechanisms” to translate the gender budgeting research into a public policy imperative at the national and state levels.25

The second stage of gender budgeting as a fiscal innovation was to establish the “institutional mechanisms.” The Classification of Budgetary Transactions, a committee of the Ministry of Finance, incorporated gender budgeting as one of its Terms of Reference in 2003. In his 2004 Union Budget Speech, the finance minister accepted the recommendations of the committee and announced that India would begin gender budgeting from 2004-05 onward.26 To strengthen the process, the Ministry of Finance mandated that it become part of the Budget Call Circular (see “Fiscal policy for sustainable development,” published by Palgrave Macmillan, 2022).27

The institutional structure of a gender budgeting initiative can vary. In India, it includes a Gender Budgeting Secretariat placed in the Ministry of Finance and Gender Budgeting Cells located in the sectoral Ministries. While this is not codified in the budget law, the Classification of Budgetary Transactions Committee of the Ministry of Finance has clearly articulated the establishment of institutional mechanisms like Gender Budgeting Cells that undertake two types of analysis as summarized by Chakraborty (2024): “(a) ex-post gender budgeting, in which the existing budget is analyzed through a gender lens and (b) ex-ante gender budgeting, in which the needs of the women are identified first and then incorporated into the budget. Ex-ante gender budgeting is relatively easy at sub-national levels of government,” in which the needs of women are taken into account up front.28 To put it differently, ex-ante budgeting is a stronger approach to identifying gender gaps and targeting expenditures to that end; by contrast, the ex-post exercise is simply a gender auditing process applied to existing budgets.29

The third stage of gender budgeting is “capacity building” of officials across sectors in NIPFP, MWCD, and U.N. agencies at the national and subnational levels. The feminization of governance at the local level, with the mandatory 33% for women elected representatives at the third tier, helped in implementing gender budgeting by translating the preferences expressed by women into public expenditure decisions.30 This empirical evidence is captured through randomized control experiments in a few states in India.31 The capacity building of officials in the sectoral Gender Budgeting Cells has helped to catalyze the process of gender budgeting.

The fourth phase of gender budgeting is to build accountability mechanisms linking “resources to results” through appropriate fiscal marksmanship analysis (marksmanship is perfect when there is no deviation between what is announced in budget and the actual outlays) and auditing by the CAG. Often, gender budgets are subject to oversight by national parliaments or supreme audit institutions. In India, fiscal councils are absent. Usually, fiscal councils report the fiscal marksmanship and fiscal transparency issues. In the absence of fiscal councils, fiscal transparency and accountability analysis are undertaken by the NIPFP.32 The CAG auditing at the state level of gender budgeting processes has helped to decrease the deviation between the budget estimates and actual spending in the case of a state like Karnataka.33

3.2 The impact of India’s gender budget on outcomes for women

The approach of gender budgeting in India is to classify projected expenditures in three parts using a 0-100 scale. Part A examines programs specifically targeted to women, which are a tiny percentage of the budget. Part B aims to identify projected expenditures on programs where 30-99% of the allocations go to women, while Part C reflects projected expenditures on programs where allocations to women are less than 30%.34

As the model of gender budgeting has remained unchanged since 2004-05 at national and subnational levels, considerable time series (comparable) data exists for an analysis of the impact of gender budgeting on gender equality outcomes. Stotsky, Chakraborty, and Gandhi (2019) analyze data from 1991–2015 for 29 Indian states to study the impact of fiscal transfers on gender equality. They find that unconditional budgetary transfers (e.g., with no restrictions on their use), compared to conditional transfers (e.g., such as for education), improve gender equality.35 Earlier, Stotsky and Zaman (2016) investigated the effect of gender budgeting on gender equality outcomes and concluded that gender budgeting has a positive influence on gender equality in elementary education. Specifically, they find that states that work on gender budgeting have made more progress toward equal enrollment in primary schools than states that do not.36

As noted earlier, existing research on gender budgeting in India has generally not incorporated analysis of IGFTs. One exception is Chakraborty (2010), which examined how India’s federal architecture affects the implementation of gender budgeting. She argued that since many public services (health, education, and social protection) that meet women’s needs fall under state jurisdiction, intergovernmental transfers are critical for advancing gender equality.37 Yet, as subsequent empirical work with Stotsky, Chakraborty, and Gandhi (2019) shows, the transfer formulas rarely include gender criteria, limiting their redistributive potential.38 The federal context also creates wide inter-state variation in gender budgeting outcomes, with wealthier states better able to sustain programs that benefit women. Embedding gender development indicators into Finance Commission transfer formulas can help ensure a more equitable approach for states to implement gender budgeting.39 Chakraborty (2010) suggested two methods for revising the transfer formulas: (i) incorporating gender variables (such as the ratio of girls to boys in the 0-6 age group) into formula-based tax transfers and/or (ii) designing a new fiscal transfer to the subnational government level to support state-level gender budgeting initiatives.40 Singh and Chakraborty (2024) show that integrating gender and demographic transition variables in IGFT can enhance the progressivity of tax transfers to the states, but that has yet to be widely adopted and evaluated.41

3.3 Gender budgeting and care

India’s gender budget documents generally refer to care services, especially for children. However, a separate child budget is included in the union budgets, which has a comprehensive list of public finance for child care.42 A few state gender budgets also list eldercare items (e.g., homes for the aged, senior citizen programs). And while the official Union and state gender budget statements report allocations for these services, none estimate the “amount needed” for care as a percentage of the budget.43 On the revenue side, tax policy does not include tax credits for care for households.

However, there is ample scope to incorporate the issue of care services into gender budgeting initiatives and macroeconomic frameworks. The COVID-19 pandemic reinforced the urgency of incorporating care into fiscal policy. Chakraborty (2022) documented how the pandemic amplified women’s unpaid care responsibilities, with significant implications for labor market participation and time poverty. With time-use data, the study showed that lockdowns and school closures intensified women’s unpaid domestic and caregiving work, while fiscal responses largely overlooked this dimension. Fiscal stimulus measures, including cash transfers and food subsidies, while important, were insufficient to address the care crisis. Recommending the integration of care infrastructure—such as childcare centers and eldercare facilities into recovery packages—was framed not as social welfare but as macroeconomic policy that boosts aggregate demand and labor supply. As a result, the analysis situated unpaid care squarely within larger fiscal policy debates and highlighted gender budgeting as the institutional mechanism for identifying the trade-offs between paid and unpaid work. This strand of work expands the scope of gender budgeting beyond financial allocations to include time as a crucial dimension of gender inequality.44

Gender budgeting exercises have shown that national- and state-level governments’ policies that were considered gender neutral were in fact not gender neutral. For instance, as a result of gender budgeting, during the Union Budget for 2016-17, the finance minister incorporated an initiative in the energy sector designed to help low-income women. Specifically, the initiative provided free liquified petroleum gas connections to women in households living below the poverty line. It was approved by the Cabinet Committee on Economic Affairs, chaired by the prime minister. This marked the first instance in India’s history where the Ministry of Petroleum and Natural Gas executed a welfare scheme that benefited many women from the poorest households, serving as a notable example of how a ministry typically perceived as gender-neutral can create a policy that addresses the needs of women.45

4. Conclusion

At the macro level, GDP-centric approaches to fiscal policy obscure unpaid care and intra-household inequalities and limit effectiveness. Gender budgeting, when embedded in macroeconomic frameworks, can correct these blind spots by aligning fiscal priorities with broader measures of human development and well-being. Importantly, gender budgeting must move beyond expenditure to include taxation.

The Indian experience with gender budgeting demonstrates that fiscal innovations can promote equity and accountability when they are institutionalized and diligently implemented. Key lessons include:

- Institutional anchoring is essential: Embedding gender budgeting within the Ministry of Finance, supported by Gender Budgeting Cells across line ministries, has helped establish it as a core fiscal instrument rather than a tangential initiative. However, many of these cells still primarily act as reporting units with limited analytical capacity. Enhancing their capacity to collect outcome indicators and analyse the data is an important next step. Finally, gender budgeting should be made legally mandatory within India’s fiscal legislation to secure its sustainability.

- Accountability and outcome monitoring strengthen effectiveness: Oversight through fiscal marksmanship analysis, audits by the CAG, and parliamentary review has reduced gaps between allocations and actual spending, with CAG reports increasingly incorporating gender budgeting audits at the state level. At the same time, India’s shift from only tracking financial inputs to aligning expenditures with actual outcomes for men and women in results frameworks reflects an important evolution. While progress has been made with sex-disaggregated fiscal data and time-use statistics—enabling benefit incidence and longitudinal analysis—significant gaps in administrative and tax data persist. Closing these gaps and ensuring monitoring systems focus on outcomes and compliance will be key to advancing gender budgeting.

- Political commitment drives effectiveness: States with strong political will and resilient institutions have integrated gender budgeting into planning and expenditure tracking, showing what is possible when leadership is sustained. In contrast, where political commitment is weaker, gender budgeting risks becoming a box-ticking exercise with little impact on spending or policy design.

- Capacity building supports implementation: Ongoing training of officials at both national and subnational levels has been critical for applying gender-responsive approaches and ensuring commitments turn into action. Uneven training coverage and frequent turnover, however, weaken institutional memory. These challenges highlight the need to invest in systematic, continuous programs that institutionalize knowledge and create more resilient practices.

- IGFTs as a lever for equity: Because many essential services for women—including health, education, and social protection—are delivered at the state level, IGFTs could be a powerful tool for advancing equity. Yet transfer formulas rarely include gender-sensitive criteria, which leaves poorer states at a disadvantage compared to wealthier ones. Integrating gender and demographic indicators into transfer systems would help ensure more equitable outcomes.

Author

-

Acknowledgements and disclosures

The Brookings Institution is a nonprofit organization devoted to independent research and policy solutions. Its mission is to conduct high-quality, independent research and based on that research, to provide innovative, practical recommendations for policymakers and the public. The conclusions and recommendations of any Brookings publication are solely those of its author(s), and do not reflect the views or policies of the Institution, its management, its other scholars, or the funders acknowledged below.

This publication is supported by the Gates Foundation, the William and Flora Hewlett Foundation, and the Norwegian Agency for Development Cooperation (Norad). The findings and conclusions contained within are those of the authors and do not necessarily reflect positions or policies of the donors.

Brookings recognizes that the value it provides is in its absolute commitment to quality, independence, and impact. Activities supported by its donors reflect this commitment.

-

Footnotes

-

Chakraborty, Lekha. 2014. “Gender Responsive Budgeting, as Fiscal Innovation: Evidence from India on ‘Processes.’” 14/128. Working Paper 128. Preprint, National Institute of Public Finance and Policy, January. https://nipfp.org.in/media/documents/WP_2014_128.pdf.; Chakraborty, Lekha. 2022. Fiscal Policy for Sustainable Development in Asia-Pacific: Gender Budgeting in India. Palgrave Macmillan.

https://link.springer.com/book/10.1007/978-981-19-3281-6. - Chakraborty. “Gender Responsive Budgeting”; Chakraborty. Fiscal Policy for Sustainable Development in Asia-Pacific.

- “Gender Responsive Planning and Budgeting: State Journeys.” UNWOMEN. N.d. https://asiapacific.unwomen.org/sites/default/files/2024-02/in-c639-annex-40-state-grb-journeys-compendium.pdf ; Stotsky, Janet Gale, and Asad Zaman. 2016. “The Influence of Gender Budgeting in Indian States on Gender Inequality and Fiscal Spending.” IMF Working Paper 16/227. Preprint, IMF. https://www.imf.org/en/Publications/WP/Issues/2016/12/31/The-Influence-of-Gender-Budgeting-in-Indian-States-on-Gender-Inequality-and-Fiscal-Spending-44411.

- Chakraborty, Lekha. 2021. “Covid-19 and Gender Budgeting: Applying a ‘Gender Lens’ to Union Budget in India.” NIPFP Working Paper Series 362. Preprint, National Institute of Public Finance and Policy. https://www.nipfp.org.in/media/medialibrary/2021/12/WP_362_2021.pdf.

- India has a three-tiered federal structure, with 28 state governments and eight centrally administered Union Territories and more than a quarter million local self-governments in states, in both rural and urban areas.

-

Budget at a Glance 2025-2026. 2025. Ministry of Finance, Government of India.

https://www.indiabudget.gov.in/doc/Budget_at_Glance/budget_at_a_glance.pdf. -

Nagpal, Resham, and Abhishek Singh. 2025. A New Fiscal Consolidation Roadmap. NIPFP. March 24.

https://www.nipfp.org.in/publication-index-page/blog-index-page/a-new-fiscal-consolidation-roadmap/?year=2024. - Budget at a Glance 2025-2026. 2025. Ministry of Finance, Government of India.

- Ibid.

- Ibid.

-

Individual taxation is more gender equitable than joint taxation which imposes higher burdens on women. Coelho Maria, Aieshwarya Davis, and Alexander D Klemm. “Gendered Taxes: The Interaction of Tax Policy with Gender Equality”, IMF Working Papers 2022, 026 (2022), accessed September 25, 2025.

https://www.imf.org/en/Publications/WP/Issues/2022/02/04/Gendered-Taxes-The-Interaction-of-Tax-Policy-with-Gender-Equality-512231 -

Stotsky, Janet Gale, Lekha Chakraborty, and Piyush Gandhi. 2019. “Impact of Intergovernmental Fiscal Transfers on Gender Equality in India: An Empirical Analysis.” NIPFP Working Paper Series 240. Preprint, National Institute of Public Finance and Policy.

https://nipfp.org.in/media/medialibrary/2019/04/WP-240_2019.pdf. -

Chakraborty, Pinaki, Lekha Chakraborty, Krishanu Karmakar, and Shashi M. Kapila. 2010. “Gender Equality and Taxation in India: An Unequal Burden?” In Taxation and Gender Equity: A Comparative Analysis of Direct and Indirect Taxes in Developing and Developed Countries. Routledge.

https://www.taylorfrancis.com/chapters/edit/10.4324/9780203852958-12/gender-equality-taxation-india-unequal-burden-pinaki-chakraborty-lekha-chakraborty. - Ibid.

-

Awasthi, Rajul, Katie Pyle, Namita Aggarwal, and Parvina Rakhimova. 2023. “Gender-Based Discounts on Taxes Related to Property: Role in Encouraging Female Ownership: A Case Study of Indian States and Cities.” Policy Research Working Paper 10287. Preprint, World Bank.

https://openknowledge.worldbank.org/server/api/core/bitstreams/8e3e02fe-3ced-426c-8355-080ece2408c6/content. - Ibid.

-

Chakraborty, Lekha, Yadawendra Singh, and Jannet Farida Jacob. 2012. “Public Expenditure Benefit Incidence on Health: Selective Evidence from India.” 12/111. Working Paper 111. Preprint, National Institute of Public Finance and Policy.

https://www.nipfp.org.in/media/medialibrary/2013/04/wp_2012_111.pdf. - Ibid.

- Chakraborty. “Asia: A Survey of Gender Budgeting Efforts.”

- Ibid.

-

Chakraborty, Lekha. 2024. “Gender Budgeting: Public Financial Management Tool for Accountability.” NIPFP Working Paper No. 409, National Institute of Public Finance and Policy, May 24, 2024.

https://nipfp.org.in/media/medialibrary/2024/05/WP_409_2024_GdYJyh7.pdf - Chakraborty. Fiscal Policy for Sustainable Development in Asia-Pacific.

- Chakraborty. “Asia: A Survey of Gender Budgeting Efforts.”

-

In 2002, the NIPFP also worked with the Finance Ministry of Sri Lanka to adapt the NIPFP methodology to the country’s budget. See: Chakraborty, Lekha. 2003. Budgetary Allocations and Gender in Sri Lanka: A Categorization of Financial Inputs. UNIFEM.

https://www.semanticscholar.org/paper/Budgetary-allocations-and-gender-in-Sri-Lanka%3A-a-of-Chakraborty/68f3888dc24253e4b5aa5fd4eeb4ad664bb7a1aa?utm_source=direct_link. - Chakraborty. “Gender Responsive Budgeting, as Fiscal Innovation.”

- Ibid.

- Chakraborty. Fiscal Policy for Sustainable Development in Asia-Pacific.

- Chakraborty. “Gender Budgeting: Public Financial Management Tool for Accountability.”

- Chakraborty. “Gender Responsive Budgeting, as Fiscal Innovation”

- Ibid.

-

Chattopadhyay, Raghabendra, and Esther Duflo. 2004. “Women as Policy Makers: Evidence from a India-Wide Randomized Policy Experiment.” Econometrica 72 (5): 8615.

https://economics.mit.edu/sites/default/files/2022-08/Women%20as%20Policy%20Makers%20Evidence%20from%20a%20Randomized.pdf - Chakraborty. “Gender Responsive Budgeting, as Fiscal Innovation”

-

Mohammed, Akram. 2021. “CAG Flags Karnataka’s Gender Budget as a ‘Mere Allocation Exercise.’” Deccan Herald, September 19.

https://www.deccanherald.com/india/karnataka/cag-flags-karnatakas-gender-budget-as-a-mere-allocation-exercise-1032164.html#google_vignette. -

The analytical matrices that collate the fiscal data for the three categories can be found in the Appendix B p. 56 of the IMF’s Asia: A Survey of Gender Budgeting Efforts.” See: Chakraborty. “Asia: A Survey of Gender Budgeting Efforts.”; “Expenditure Profile 2025-2026.” 2025. Government of India, Ministry of Finance Budget Division, February.

https://www.indiabudget.gov.in/doc/eb/stat13.pdf - Stotsky et al. “Impact of Intergovernmental Fiscal Transfers on Gender Equality in India.”

-

Beyond India, the impact of gender budgeting on sectoral gender outcomes is examined by Chakraborty, Ingrams, and Singh (2017) for the Asia Pacific area. The researchers conclude that gender budgeting has a statistically significant influence on educational and health outcomes but no effect on labor force participation rates. They also highlight that public expenditure significantly improved gender equality. The increase in labor force participation rates requires conscious care economy infrastructure, presently lacking in most countries, so is a significant thrust of gender budgeting. See: Chakraborty, Lekha, Marian Ingram, and Yadawendra Singh. 2017. “Effectiveness of Gender Budgeting on Gender Equality and Fiscal Space: Empirical Evidence from Asia Pacific.” GrOW Working Paper Series. Preprint, Institute for the Study of International Development (ISID), McGill University.

https://grow.research.mcgill.ca/publications/working-papers/gwp-2017-09.pdf. Stotsky & Zaman. “The Influence of Gender Budgeting in Indian States on Gender Inequality and Fiscal Spending.” -

Chakraborty, Lekha. 2010. “Determining Gender Equity in Fiscal Federalism: Analytical Issues and Empirical Evidence from India.” Levy Economics Institute Working Papers Series 590. Preprint, Levy Economics Institute of Bard College, March.

https://www.levyinstitute.org/wp-content/uploads/2024/02/wp_590.pdf. - In India, the tax transfer formula is developed by Finance Commissions, constituted by the President.

- Stotsky et al. “Impact of Intergovernmental Fiscal Transfers on Gender Equality in India.”

- Stotsky et al.“Impact of Intergovernmental Fiscal Transfers on Gender Equality in India.”, Chakraborty. “Determining Gender Equity in Fiscal Federalism.”

- Singh, Yadawendra, and Lekha Chakraborty. 2024. “Tax Transfers and Demographic Transition: Empirical Evidence for 16th Finance Commission.” NIPFP Working Paper Series 417. Preprint, National Institute of Public Finance and Policy. https://nipfp.org.in/media/medialibrary/2024/08/WP_417_2024.pdf.

-

Expenditure Profile 2025-2026. 2025. Government of India, Ministry of Finance Budget Division.

https://www.indiabudget.gov.in/doc/eb/stat12.pdf. -

Expenditure Profile 2025-2026. 2025. Government of India, Ministry of Finance Budget Division.; “Gender Budgeting in the Annual Budget 2024-2025.” 2024. Open Budgets India.

https://openbudgetsindia.org/dataset/ad54dc64-21b2-4897-8110-c2813c4fc8e2/resource/3dbe6d17-250e-482c-8044-6dabc817a965/download/delhi-budget-2024-25-gender-budget.pdf. Government of Odisha, Finance Department. “Gender Budget. 2024-2025” https://finance.odisha.gov.in/sites/default/files/2024-07/14-Gender_Budget.pdf -

Chakraborty, Lekha. 2022. “Covid19 and Unpaid Care Economy: Evidence on Fiscal Policy and Time Allocation in India.” 372, NIPFP Working Paper Series. Preprint, National Institute of Public Finance and Policy.

https://nipfp.org.in/media/medialibrary/2022/02/WP_372_2022.pdf. - Ibid.

-

Chakraborty, Lekha. 2014. “Gender Responsive Budgeting, as Fiscal Innovation: Evidence from India on ‘Processes.’” 14/128. Working Paper 128. Preprint, National Institute of Public Finance and Policy, January. https://nipfp.org.in/media/documents/WP_2014_128.pdf.; Chakraborty, Lekha. 2022. Fiscal Policy for Sustainable Development in Asia-Pacific: Gender Budgeting in India. Palgrave Macmillan.

https://link.springer.com/book/10.1007/978-981-19-3281-6.

https://www.indiabudget.gov.in/doc/Budget_at_Glance/budget_at_a_glance.pdf.

https://www.nipfp.org.in/publication-index-page/blog-index-page/a-new-fiscal-consolidation-roadmap/?year=2024.

https://www.imf.org/en/Publications/WP/Issues/2022/02/04/Gendered-Taxes-The-Interaction-of-Tax-Policy-with-Gender-Equality-512231

https://nipfp.org.in/media/medialibrary/2019/04/WP-240_2019.pdf.

https://www.taylorfrancis.com/chapters/edit/10.4324/9780203852958-12/gender-equality-taxation-india-unequal-burden-pinaki-chakraborty-lekha-chakraborty.

https://openknowledge.worldbank.org/server/api/core/bitstreams/8e3e02fe-3ced-426c-8355-080ece2408c6/content.

https://www.nipfp.org.in/media/medialibrary/2013/04/wp_2012_111.pdf.

https://nipfp.org.in/media/medialibrary/2024/05/WP_409_2024_GdYJyh7.pdf

https://www.semanticscholar.org/paper/Budgetary-allocations-and-gender-in-Sri-Lanka%3A-a-of-Chakraborty/68f3888dc24253e4b5aa5fd4eeb4ad664bb7a1aa?utm_source=direct_link.

https://economics.mit.edu/sites/default/files/2022-08/Women%20as%20Policy%20Makers%20Evidence%20from%20a%20Randomized.pdf

https://www.deccanherald.com/india/karnataka/cag-flags-karnatakas-gender-budget-as-a-mere-allocation-exercise-1032164.html#google_vignette.

https://www.indiabudget.gov.in/doc/eb/stat13.pdf

https://grow.research.mcgill.ca/publications/working-papers/gwp-2017-09.pdf. Stotsky & Zaman. “The Influence of Gender Budgeting in Indian States on Gender Inequality and Fiscal Spending.”

https://www.levyinstitute.org/wp-content/uploads/2024/02/wp_590.pdf.

https://www.indiabudget.gov.in/doc/eb/stat12.pdf.

https://openbudgetsindia.org/dataset/ad54dc64-21b2-4897-8110-c2813c4fc8e2/resource/3dbe6d17-250e-482c-8044-6dabc817a965/download/delhi-budget-2024-25-gender-budget.pdf. Government of Odisha, Finance Department. “Gender Budget. 2024-2025” https://finance.odisha.gov.in/sites/default/files/2024-07/14-Gender_Budget.pdf

https://nipfp.org.in/media/medialibrary/2022/02/WP_372_2022.pdf.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).