Corporate tax policy is increasingly shaped by multilateral coordination. The OECD/G20 global minimum tax, for example, establishes a common statutory floor intended to limit profit shifting and reduce harmful tax competition. But even when countries adopt similar tax rules, firms may respond to those rules differently. Understanding those differences is essential for interpreting the economic effects of coordinated corporate tax policy.

Using administrative corporate tax return data from 16 countries and a unified analytic framework, we estimate the corporate elasticity of taxable income—the measure of how strongly reported income responds to tax incentives. We find substantial cross-country differences in this responsiveness. In some countries, taxable income responds only modestly to changes in the tax rate. In others, the responsiveness is more than twice as large.

Much of this variation can be traced to observable features of tax systems and economies. We show that tax system characteristics explain roughly half of the cross-country variation in responsiveness, while firm composition and broader country fundamentals account for the remainder.

These differences have direct implications for tax policy. When countries implement similar statutory tax changes—as under coordinated reforms like the global minimum tax—the resulting revenue gains and economic tradeoffs depend on how strongly firms respond to tax incentives in each country. Measuring those responses is therefore central to evaluating both domestic tax reforms and multilateral coordination. To support policy evaluation, we make more than 200 country-specific elasticity estimates, revenue implications, welfare calculations, and prediction tools publicly available through the Global Tax Research Initiative.

Our work suggests that a harmonized statutory rate does not produce harmonized economic effects. Understanding how corporate tax responsiveness differs across countries is therefore central to evaluating both domestic reforms and multilateral coordination.

Multilateral rate alignment does not guarantee uniform economic effects

Multilateral corporate tax reform centers on statutory rates because differences in rates across countries create incentives for profit shifting. When one country lowers its corporate rate to attract investment or reported profits, others face pressure to respond. The resulting tax competition gradually erodes tax revenues from corporate profit, weakening a core source of public finance. The OECD/G20 global minimum tax addresses this dynamic directly by setting a 15% minimum corporate tax rate that participating countries agree to enforce.

Aligning rates addresses the competition problem. It does not, however, determine how corporate tax bases respond once those rates change.

Corporate tax revenue depends on both statutory rates and the size of the taxable base. When rates change, part of the revenue effect is mechanical: Applying a higher rate to the existing base raises revenue. Another part depends on how firms adjust their taxable income in response to the change. If firms reduce taxable income when rates rise—or increase taxable income when rates fall—this behavioral response can offset some of the mechanical effect.

Coordinated reforms often proceed as if these behavioral responses are comparable across countries. Under that view, harmonizing statutory rates should generate broadly similar fiscal and economic effects.

This assumption, however, is strong. Countries differ in their enforcement capacity, corporate tax rules, sectoral composition, firm size distributions, and exposure to cross-border capital flows. Each of these features can shape how strongly the corporate tax base responds to incentives.

If responsiveness differs systematically across countries, identical statutory reforms will not generate identical revenue or efficiency effects. Evaluating coordinated corporate tax policy therefore requires measuring how strongly corporate taxable income responds to tax incentives in each setting.

The elasticity of taxable income provides that measure.

The elasticity of taxable income summarizes how corporate tax bases respond to the tax system

The elasticity of taxable income measures how much reported corporate income changes when tax incentives change. It captures the degree to which firms adjust their taxable income in response to a change in the net-of-tax rate—the share of profits they keep after taxes.

When tax rates change, firms may adjust their employment or investment, shift profits across jurisdictions, adjust the timing of income or deductions, or reorganize operations. These behavioral responses shrink or expand reported taxable income and alter how much revenue is ultimately collected.

The elasticity of taxable income summarizes these behavioral responses in a single measure. A low elasticity means that firms adjust little when tax rates change, so most of the revenue effect reflects the statutory change itself. A high elasticity means firms adjust more strongly, so changes in statutory rates translate less directly into changes in revenue.

This parameter governs more than revenue projections. It also reflects the economic cost of raising tax revenue through the corporate tax. When firms adjust behavior in response to changing tax rates, resources are reallocated. The stronger the response, the larger the economic cost associated with raising an additional dollar of revenue.

For policymakers, the elasticity of taxable income functions as a reduced-form measure of corporate tax responsiveness. At the same time, it does not distinguish between responses driven by real changes in economic activity and changes in reporting behavior. Instead, it reflects the total response of the tax base to incentives within a given institutional setting. In some settings, these responses may also reflect shifts between the corporate sector and pass-through forms of business organization, which our estimates do not separately identify.

To see why the magnitude of this parameter matters, consider a simple example. Suppose an economy has $10 trillion in corporate taxable income and a statutory rate of 21%, generating $2.1 trillion in revenue. Now consider the effect of a small tax reduction—a 1% increase in the net-of-tax rate.

If the elasticity of taxable income is zero, firms do not adjust their behavior when faced with a tax change. Revenue changes are purely mechanical. At a 21% rate, a 1% increase in the net-of-tax rate corresponds to a 0.79 percentage point reduction in the statutory rate. Holding the tax base fixed, revenue would fall by $79 billion.

The total revenue effect of a tax change, however, also depends on how much firms adjust their taxable income in response. Table 1 shows how the outcome varies with the elasticity of taxable income.

|

Elasticity of Taxable Income |

Mechanical Revenue Change |

Behavioral Revenue Change |

Total Revenue Change |

|

0 |

-$79B |

$0B |

-$79B |

|

1 |

-$79B |

+$21B |

-$58B |

Assumptions: $10 trillion in taxable income, 21% statutory rate

When the elasticity is zero, revenue changes are entirely mechanical. When the elasticity is one, taxable income rises by 1% in response to the higher net-of-tax rate, offsetting roughly one-quarter of the mechanical loss. The mechanical component is fixed; what varies is the behavioral response of the tax base. Measuring that responsiveness is therefore central to understanding the fiscal and economic consequences of the corporate tax.

Applying a unified methodology enables credible cross-country comparisons

Estimating how strongly corporate taxable income responds to tax incentives is methodologically demanding. The elasticity of taxable income cannot be observed directly. It must be inferred from how firms adjust their reported income when marginal tax incentives change. That requires both detailed data and a consistent empirical approach.

The first constraint in this process relates to data access. Corporate taxable income is defined by national tax law. It reflects country-specific rules governing things like how to account for capital costs, how to deal with firm losses, how to treat members of complex corporate groups, minimum taxes, and cross-border flows. This requires access to administrative corporate tax return data. Financial accounting profits, which are observable for publicly traded companies, cannot serve as a substitute because these measures diverge from taxable income in systematic ways.

A second constraint relates to statistical power. The empirical strategy employed relies on observing how firms cluster around tax thresholds—points where marginal tax incentives change. In corporate taxation, the most common threshold occurs at zero taxable income: firms reporting losses face a zero marginal tax rate, while the first dollar of taxable income faces the statutory corporate tax rate. If firms adjust their behavior or reporting when faced with this change, that adjustment appears in the number of firms with taxable income near this threshold. Detecting that response requires large samples and complete coverage of the corporate population. Partial datasets or aggregate statistics are insufficient.

A third constraint is institutional. Corporate tax return data are usually protected by taxpayer privacy laws so are therefore confidential. They are housed within secure government systems and subject to strict privacy rules. Access to such data is governed by country-specific procedures. Data typically cannot be transferred across borders or pooled into a common international dataset. As a result, previous estimates have generally been produced country by country, often using different methods and definitions. That fragmentation makes cross-country comparisons difficult. Observed differences in elasticities, therefore, may reflect differences in estimation techniques rather than differences in firm behavior.

This project was structured to overcome those institutional barriers directly. We assembled a coordinated international research team, members of which retained authorized access to administrative corporate tax returns within their respective jurisdictions. In all, the research team included 26 researchers with access to data from 16 different countries. In countries where tax records are required to be housed within secure government environments, all estimation was conducted inside those systems. In other settings, researchers worked within the applicable legal and confidentiality frameworks governing access to the tax data. No confidential microdata was shared across research teams outside the authorized data access environment governing each country’s records.

At the same time, we developed a standardized estimation procedure that was implemented identically within each country. This approach isolates differences in firm responsiveness rather than differences driven by methodology.

The result is the first set of globally comparable corporate taxable income elasticities estimated using administrative data under a unified methodology. It represents the first large-scale, multilateral effort to generate directly comparable corporate taxable income elasticities across countries using administrative tax return data.

Uniform tax rules are unlikely to produce uniform outcomes

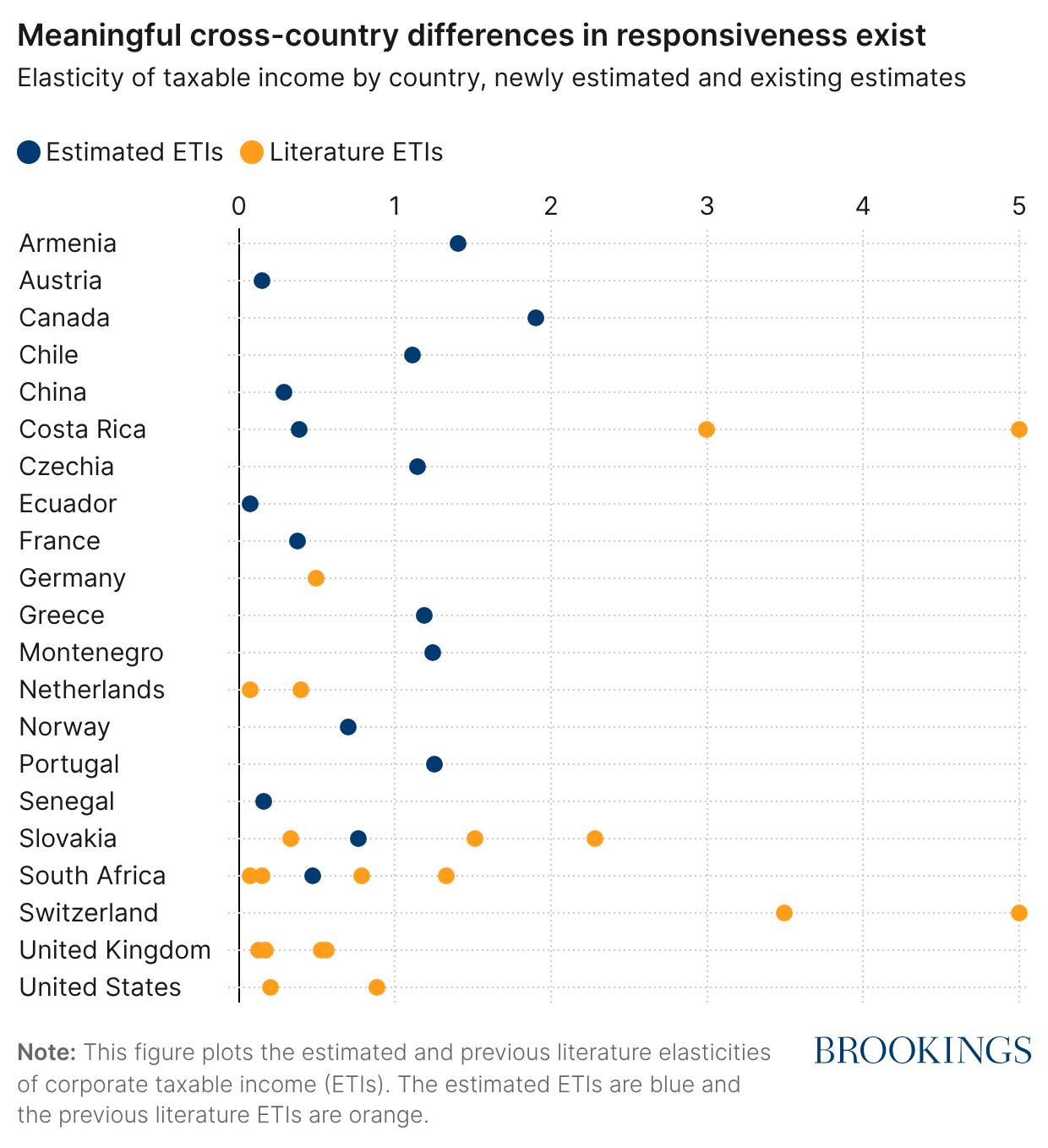

The resulting estimates show meaningful cross-country heterogeneity. Figure 1 presents the full set of country estimates using the harmonized methodology (red dots) alongside previously published corporate elasticity estimates from the literature (green triangles).

Elasticities span a wide interval across countries, ranging from values close to zero to just under two, with an average of 0.79. An elasticity close to zero implies that firms make little adjustment to reported taxable income when tax rates change. In that case, the revenue effect of a rate increase is driven almost entirely by the mechanical application of the higher rate to the existing base. An elasticity near one implies that reported taxable income moves nearly proportionally with changes in the net-of-tax rate. Higher values indicate even stronger behavioral responses.

An average elasticity of 0.79 across these 16 countries implies that a 10% increase in the net-of-tax rate leads to a roughly 8% increase in reported taxable income. In other words, firms respond to tax incentives but not one-for-one.

For context, recent estimates for the United States using administrative tax return data place the corporate elasticity of taxable income at approximately 0.89. The average elasticity in our cross-country sample is somewhat lower but of similar magnitude. Many countries cluster around values comparable to the U.S. benchmark, but others differ in meaningful ways, with implications for revenue forecasting and efficiency analysis.

The literature estimates plotted in Figure 1 span an even wider range, in some cases reaching elasticities as high as five. By applying a unified analytical framework to administrative tax return data, our analysis provides directly comparable estimates across jurisdictions. We show that even under consistent measurement, meaningful differences in corporate tax responsiveness persist across countries. Identical statutory changes are therefore expected to generate different revenue and welfare consequences across borders.

Revenue consequences of identical statutory changes differ sharply across countries

A 1 percentage point increase in the statutory corporate tax rate does not produce the same revenue gain everywhere.

Figure 2 shows the implied revenue effect of a 1 percentage point increase in the statutory corporate tax rate across the 16 countries in our study.

The revenue increase varies meaningfully across countries because firms adjust differently to a higher tax rate. In countries where firms respond only modestly, most of the expected revenue gain is preserved. In countries where firms respond more strongly, a larger share of that gain is offset by a reduction in taxable income.

Revenue differences, however, are only part of the story.

Efficiency costs per dollar of revenue raised differ even more than revenue effects

Raising corporate revenue involves an economic tradeoff. The additional revenue comes at a cost: Firms adjust their behavior in ways that affect investment, production, and overall output.

The magnitude of the cost varies substantially across countries. In some countries, raising an additional dollar of corporate tax revenue is associated with only a few cents of economic cost. In others, the cost approaches 80 cents per dollar raised.

This spread is large enough to raise questions about how the same reform should be evaluated when implemented across multiple jurisdictions. A country where each additional dollar of revenue raised comes at a relatively low economic cost faces a different trade off than a country where the cost is several times larger.

For coordinated reform, this matters directly. The OECD’s global minimum tax sets a common 15% statutory floor across participating countries. But harmonizing the rate does not harmonize the underlying economic tradeoffs. Even under a shared statutory rate, countries can face meaningfully different efficiency costs because firms respond differently within each institutional setting.

This raises a practical question for decisionmakers: What explains these differences, and can they be anticipated?

Tax system features and economic structure explain much of the variation in firm responsiveness

Corporate tax responsiveness is not random. It systematically relates to observable features of tax systems and economic structure.

We show that roughly half the variation in responsiveness across the 16 countries in our sample is associated with tax system characteristics. These include differences in statutory corporate rates, the generosity of how tax systems accommodate loss-making firms, the treatment of corporate groups, and other design features that affect how easily firms can adjust their taxable income. Countries with more flexible loss provisions or greater scope for income shifting tend to exhibit higher responsiveness. Countries with tighter rules or higher baseline rates tend to exhibit lower responsiveness.

The remaining variation is linked to firm composition and broader country fundamentals, including industrial structure, manufacturing intensity, and exposure to foreign direct investment.

Figure 3 summarizes this decomposition for all countries in our sample. The figure shows the how much each set of factors contributes to the cross-country differences in responsiveness.

Responsiveness can be predicted using observable characteristics

The relationship shown in Figure 3 allows us to move from explanation to prediction.

Because corporate responsiveness is systematically related to observable features of tax systems and economic structures, it can be approximated even in countries where administrative tax return data are not available to policymakers.

Using publicly available indicators, we generate predicted elasticity estimates for countries beyond the 16 included in our sample. These predictions track closely with estimates obtained from administrative data where both are available.

Figure 4 compares estimated and predicted elasticities across countries in our sample.

While the prediction exercise is not a substitute for administrative data, it provides a practical tool for forward-looking policy analysis. Through the Global Tax Research Initiative, we maintain a public database of country-specific predicted elasticity estimates, including corresponding revenue and efficiency calculations derived from tax return data.

The website further makes available a standardized coding package that allows researchers with secure access to administrative tax data to implement the harmonized framework within their own country.

For countries evaluating corporate tax reforms, these tools provide a structured way to assess how reforms are likely to affect revenue and economic tradeoffs in their own institutional setting.

Conclusion

Corporate tax policy is increasingly shaped by multilateral coordination. The OECD/G20 global minimum tax reflects a shared effort to limit harmful competition and stabilize corporate tax revenues. But aligning statutory rates does not align how the corporate tax base responds to those rates.

Our new research shows that corporate tax responsiveness differs systematically across countries. Those differences translate into uneven revenue gains and even more uneven economic tradeoffs. Even under a common statutory floor, countries face different fiscal and efficiency consequences because firms respond differently within each institutional setting.

For policymakers, the implication is straightforward. Coordinated tax rules reduce tax competition, but they do not eliminate underlying economic differences. Evaluating corporate tax reform—whether domestic or multilateral—requires understanding how responsive the corporate tax base is in each country.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).