This chapter is part of USMCA Forward 2026.

The year 2025 was a whirlwind for the North American auto industry. The year started with one of the most generous electric vehicle (EV) consumer subsidy schemes in history, targeted tariffs that ensured that the industry would not be overwhelmed by Chinese low-priced imports, and projections of the strongest annual growth all decade.1 It ended with an elimination of the consumer subsidies for EVs, sweeping tariffs on all manner of products and countries, and ambiguous growth prospects.2 The upcoming renegotiation of the United States-Mexico-Canada Agreement (USMCA) offers a window for policymakers to think through how to best weather these storms and emerge stronger.

The auto industry has long been one of the most important industries in North America, and is the most traded regionally.3 It is a key driver of demand for foundational industries: Globally, the auto industry procures 12% of all steel (including 26% of U.S. steel), 13% of all semiconductors, and 75% of all lithium-ion batteries. By purchasing large quantities of these inputs, the auto industry drives economies of scale and learning-curve improvements that benefit a wide swath of other industries including data centers, aerospace, agricultural equipment, and appliances. EVs are particularly important drivers of innovation, not just in batteries but also in semiconductors, casting, and robotics.4

The path to USMCA: 1960-2020

From the 1965 U.S.-Canada Auto Pact, to the 1993 North American Free Trade Agreement (NAFTA), to the 2020 U.S.-Mexico Canada Agreement (USMCA), regional policymakers have sought to structure integration to improve efficiency and lower costs, promote economic development by encouraging the many industries that supply the industry, tackle competition from outside the bloc, create balance within the bloc, reduce wage gaps, and manage energy transitions. Achieving the desired mix of openness and protection has not been a linear process, and threats have been commonplace. In the 1960s, Canada attempted to address a ballooning auto trade deficit with the U.S. by subsidizing its parts industry. When the U.S. threatened countervailing duties, the 1965 compromise allowed zero tariffs on products containing 50% U.S. or Canadian content, and the U.S. companies that dominated the market (through subsidiaries) committed to produce one car in Canada for every one sold there.5 Around the same time, Mexico considered measures like nationalization to get auto companies to tolerate licensing schemes and tariffs to require auto companies to use 60% Mexican content if they wanted to sell in that nation, and later to meet export targets.6 For its part, the U.S. successfully used tariff threats to get Japanese automakers to localize production, though the Reagan administration as part of this deal promised a veto of 90% local content requirements that had passed the U.S. House of Representatives, while its labor board issued rulings that facilitated these companies’ use of non-union labor.7

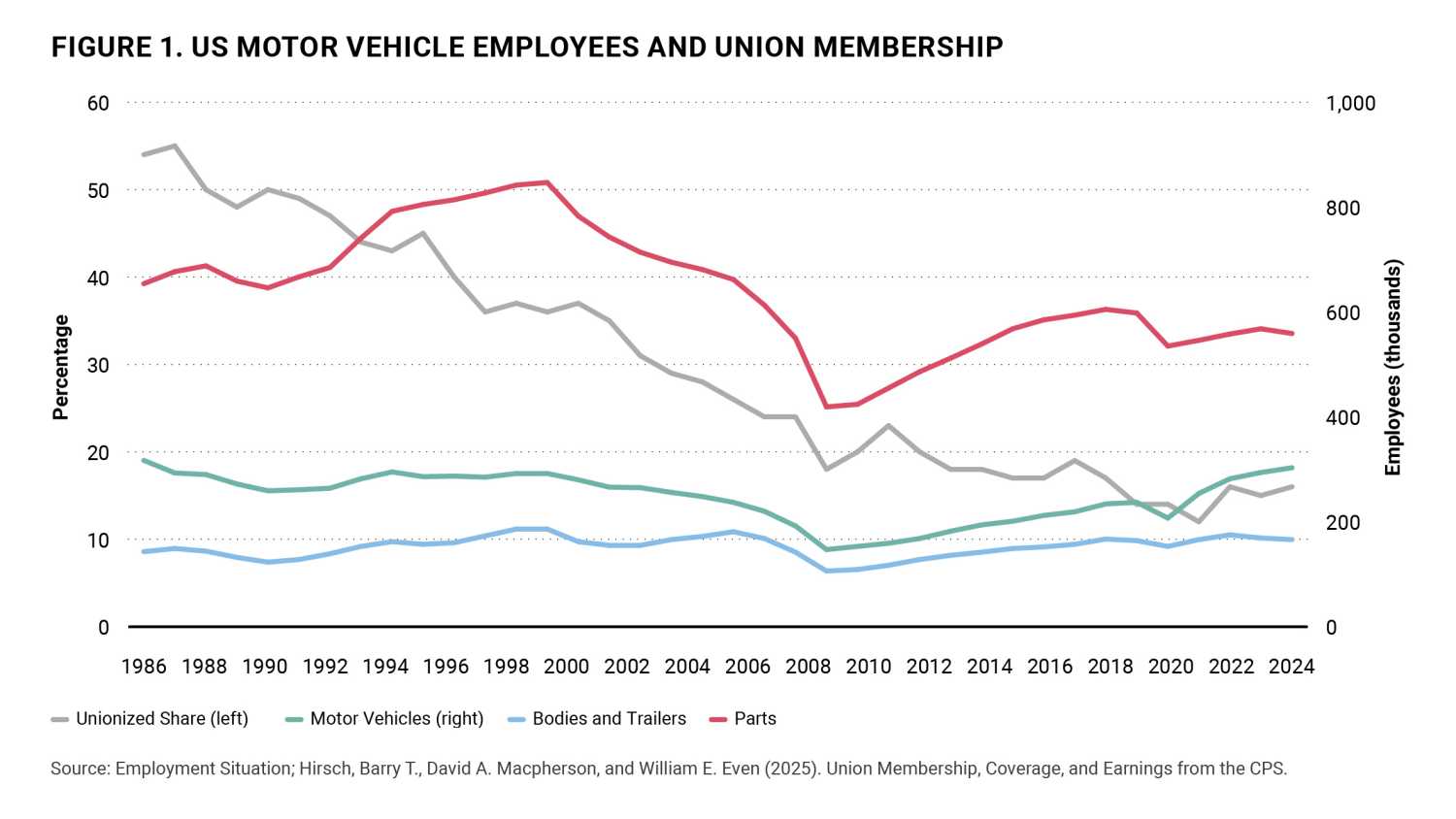

NAFTA brought duty-free trade to the entire continent, along with continental “rules of origin” (ROOs). At its signing, President Bill Clinton predicted that Mexico’s (NAFTA-required) wind-down of its industrial policies would lead to more U.S. autos being sold there and more U.S. jobs, while side deals on labor would ensure “there will be an even more rapid closing of the gap between our two wage rates” and noting the pact would enable better competition with European and Asian trading blocs.8 While NAFTA led to substantial regional integration over the next 25 years, some other promised benefits failed to materialize. Production in the U.S. and Canada did not expand, while Mexico’s share of North American production expanded considerably.9 The Mexican auto workforce grew from 167,000 in 1994 to nearly 1.3 million by 2018,10 but there was no convergence of Mexico’s wage rates with those of the U.S. and Canada.11 Moreover, the traditional Big Three U.S. companies lost domestic, regional, and global market share; U.S. auto parts jobs contracted by between a third and a half from 2000 to 2018. Unionization rates plummeted as companies used threats of relocation to Mexico and elsewhere to quash union drives (see Figure 1).12 Though some of this job loss was due to uncompetitive products and processes,13 the situation created a fertile environment for Donald Trump to paint the Clinton record negatively, and to commit in his 2016 campaign to “renegotiate NAFTA. If I can’t make a great deal, we’re going to tear it up.”14

Starting in 2017, the Trump administration took several steps that affected auto industry trade. First, his Commerce Department found that auto imports impaired U.S. national and economic security under Section 232 of the Trade Expansion Act of 1962 and recommended tariffs of 25% to 35%, including on North American nations. Yet this report was not published nor acted upon at the time.15 Second, of relevance to the auto sector as a major input, the administration imposed global 25% tariffs on imported steel and 10% on imported aluminum in July 2018 while negotiating side deals to dampen the impact on North American partners in May 2019.16 Third, NAFTA was re-negotiated over 2018–2019 to become the USMCA, which tightened ROOs still further—from NAFTA’s 62.5% regional content to a new 75% requirement. It also included requirements that 40% to 45% of a vehicle’s production value must be made by workers earning at least $16 per hour, and 70% of a vehicle manufacturer’s steel and aluminum purchase value must originate in North America.17

These changes have had mixed results. According to the U.S. International Trade Commission, the new ROOs led firms to make sourcing changes that created a small number of jobs in the auto parts and steel industries, while only modestly increasing consumer prices.18 However, U.S. firms responded to the higher compliance costs by increasing imports from non-USMCA countries, and by opting to not comply with USMCA duty-free rules and instead pay the U.S.’ 2.5% most-favored nation tariff on passenger vehicles.19 Rates of non-compliance for autos imported into the U.S. market quintupled (mostly driven by Mexican goods), while non-compliance for auto parts more than doubled for both Canadian and Mexican goods. The labor component of the ROOs did little to raise Mexican wages, as firms opted to meet this requirement through their U.S. and Canadian workers (The average hourly wage of automotive workers in Mexico in 2024 was $5.66, compared to $30.86 in the United States).20 In sum, the USMCA experience made clear that new trade deals alone did not constitute an effective response to U.S. auto sector challenges.

Rival visions: 2021-2025

In 2021, the incoming Biden administration built on the Trump administration’s approach on two fronts, focused on (re)building the social contract between the industry, workers, and the communities they serve. First, they initiated a torrent of labor rights cases under USMCA, using the Rapid Response Labor Mechanism (RRM)—a novel mechanism that Trump had negotiated (under pressure from Democrats in Congress) but never utilized.21 Instead of a cumbersome inter-state arbitration process that could take a decade to complete, the RRM allows for relatively rapid expert investigations culminating potentially in the impoundment of goods made at specific facilities until labor abuses are remedied.22 Biden initiated over 50 RRM actions—18 of which were in the automotive industry.23 These cases led to benefits for about 20,000 workers in Mexico, including reinstatement of workers, payment of backpay, and more democratic union representation.24

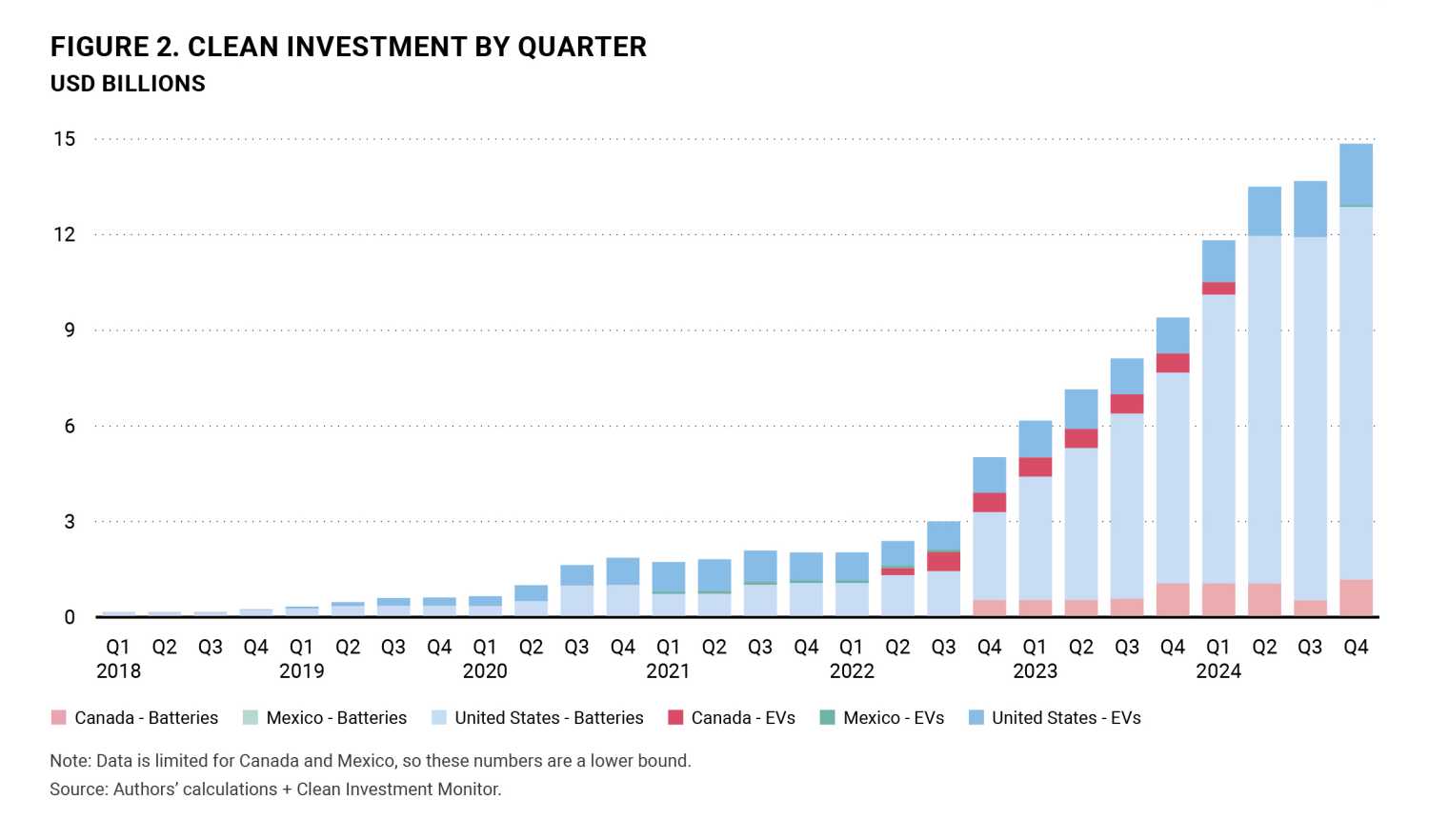

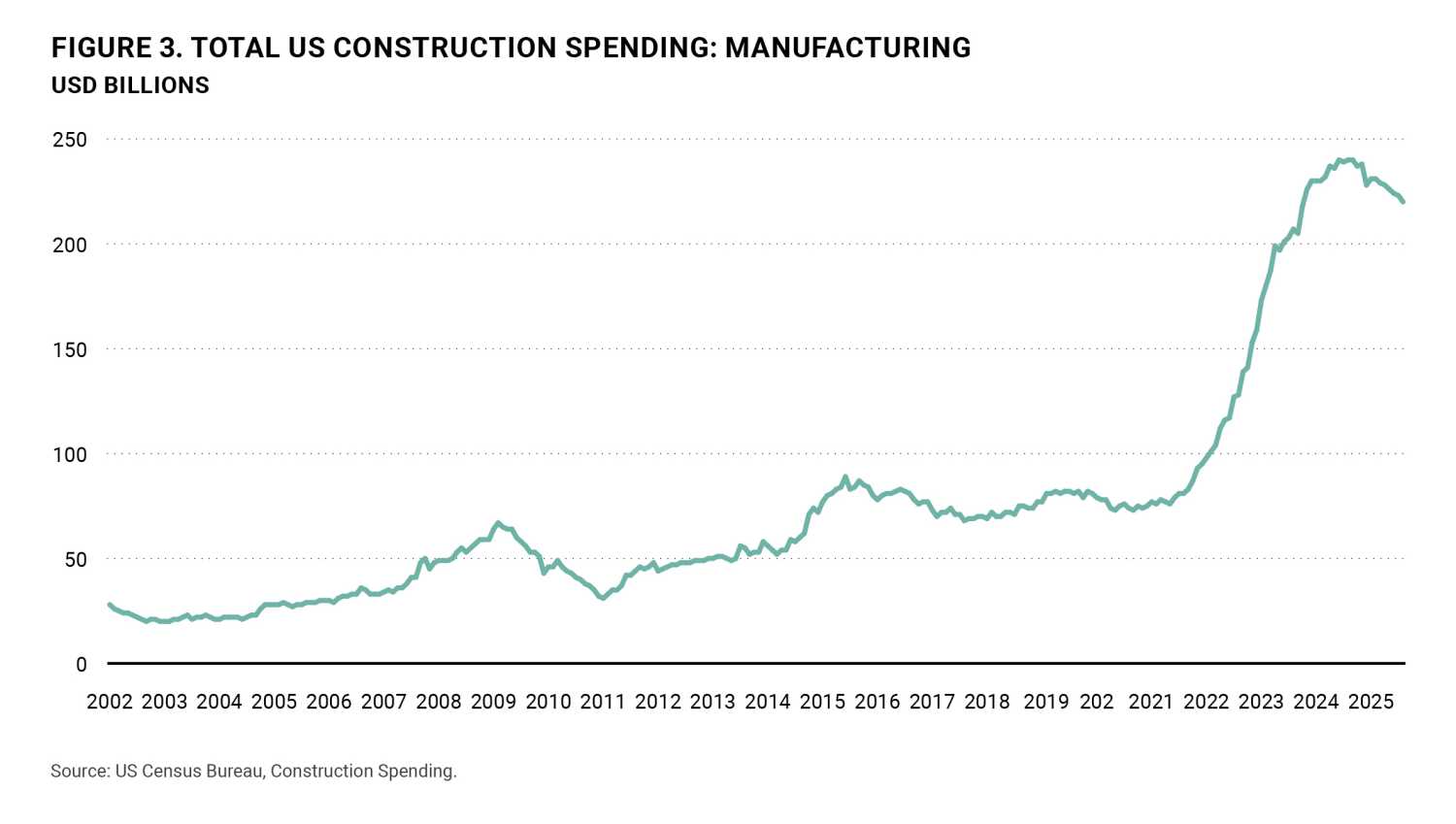

Second, Biden attempted to get auto companies to finally take on the challenge of international competition by transitioning to EVs. This was none too soon. While China was a negligible producer of EVs when NAFTA was signed and only a mid-range player when USMCA was negotiated, the country had rapidly expanded its production and exports. By the Biden years, low-cost producers like BYD were capable of supplying far more than Chinese domestic demand and over half of estimated global demand.25 This new challenge compounded the preexisting one that EV production would lead to dislocation of 200,000 workers making gas vehicle propulsion system parts.26 In response, the administration, through the Inflation Reduction Act (IRA) and Bipartisan Infrastructure Law (BIL), offered generous tax credits for EV producers and suppliers, consumer subsidies of up to $7,500 for EV purchases,27 and $39.9 billion in grants and loans for the EV supply chain through the Department of Energy—73 % of which went to firms that had partnerships with labor unions (Canada28 responded by investing $52.5 billion in its EV supply chain and Mexico29 is developing its own policies).30 Finally, in May 2024,31 the Biden administration imposed tariffs of 100% on Chinese EVs as a way to safeguard these substantial industrial policy investments (In September 2024, Canada32 matched and Mexico33 implemented a 50% tariff).34 The combined impact of these policies were impressive. As Figure 2 shows, new investment in electric vehicles and batteries increased more than 500% in North America between the second quarter of 2022 and the end of 2024, while manufacturing factory construction in the U.S. (including these and other sectors supported by Biden’s industrial policies) increased by an unprecedented 130%35 between January 2021 and June 2024 (see Figure 3).36

The second Trump administration has introduced substantial new costs and uncertainty for the industry. First, in February 2025, the second Trump administration reinstated steel and aluminum tariffs that had been paused during the first Trump and Biden administrations, including on Canada and Mexico.37 In March, Canada retaliated by imposing 25% tariffs on U.S. steel and aluminum.38 These were later doubled. Second, in March, the administration picked up the previously-shelved 2019 auto report and imposed 25% tariffs39 on autos and auto parts under Section 23240—including those from Canada and Mexico.41 Canada retaliated in April with a 25% “surtax” on U.S. autos.42 Third, in April, on so-called “Liberation Day,” the administration announced across-the-board tariffs of 10% with even higher rates for trade-surplus countries. They then negotiated “Agreements on Reciprocal Trade” (ARTs) with major trading partners like the U.K., EU, Japan, and Korea, which lowered the 25% auto tariff these countries faced to 10% to 15%. As the Big Three American automakers noted,43 this is lower than what North American producers face on their imports from Canada and Mexico. Fourth, on July 4th, the One Big Beautiful Bill Act (OBBBA) repealed the EV consumer tax credit,44 leading to a sharp drop45 in the sale of EVs and several EV supplier46 facilities shuttering.47 This latter is especially ironic, given that the consumer subsidies included tough requirements48 for local and regional- and ally- sourcing of inputs like critical minerals and batteries—promotion of which is supposedly an Administration priority.49 Finally, through the OBBBA and other cuts, the budget for RRM and other USMCA enforcement (which has disproportionately aided autoworkers) was cut dramatically.50

Can USMCA 2.0 right the ship?

The USMCA renegotiation offers an opportunity to put the North American auto industry on a firmer footing, especially about addressing challenges from China, the energy transition, and ongoing labor inequities. Here are some changes we would suggest, both incremental and fundamental, all of which have at least some political support. We think it is important to include some more ambitious proposals due to the volatile times we find ourselves in. In such an era, policymakers will be well advised to think less in terms of constitution-style policy lock-in (as in the original expiration-date-less NAFTA), and more in terms of using trade as a tool of industrial policy experimentation and learning over shorter (e.g., years- or decade-long) periods.51

Coordinate policies to address China competition and promote the energy transition

Given the high degree of integration of the industry, it makes sense to have the countries’ external postures be more consistent. The parties should adopt similar tariffs on EVs, steel, and auto products from outside the bloc, especially China. The U.S. and Canada had been mirroring each other to some extent; Mexico should match these. The U.S. should reinstate its EV subsidies (as recommended in Brookings’s USMCA Forward 2025 edition; Canada and Mexico should proportionately match them.52 A joint carbon import fee on goods from outside the bloc, an RRM-like mechanism to sanction polluters within the bloc (as called for by the Sierra Club53 and other environmental groups),54 and a joint critical minerals strategy (as called for by the Climate Leadership Council)55 are further useful steps. Moreover, recognizing that China’s advantage is in part due to superior technology, it will also be useful to agree on common terms under which Chinese investment in North America is allowed, including provisions for technology transfer and use of Chinese software (to avoid potential surveillance). Although blocked by high tariffs and software bans56 in the U.S. and Canada, Chinese automaker BYD is already the fourth largest automaker by sales in Mexico57 and is rumored again to be considering building a plant there.58 While allowing North Americans to buy $20,000 or $30,000 Chinese EVs would advance climate goals and save consumers money in the short-term, such a policy threatens regional security and high-standard production models, because China’s success is due to high subsidies and low labor and environmental standards59 as well as innovation.60 Chinese (and ideally other) investment should be allowed only if it includes requirements for neutrality towards union organizing, high environmental standards, and requirements for advanced technology transfer (mimicking Chinese policies toward U.S. multinationals, which traded market access in prior decades for technology transfer that was critical for their current development of superior technology).

Strengthen and modernize Rules of Origin (ROOs)

The ROO changes negotiated in the first Trump administration had less impact than desired, in part because of the low cost of non-compliance through paying the Most Favored Nation (MFN) tariff. Now, higher effective tariffs on imports from outside the bloc in all three countries should make the ROOs more effective. However, new distortions have been introduced by the ARTs, which disincentivize North American production. The ARTs should include similarly stringent local content, labor, and steel ROOs as the USMCA—and the USMCA 2.0 tariff rate should be lower than the ARTs’ rate in recognition of the high degree of regional integration. The American Automotive Policy Council61 and the United Autoworkers Union62 (UAW) have each advanced proposals to change ROO and related calculations to drive more regional procurement and investment.

Strengthen the Rapid Response Mechanism (RRM) and boost labor power

Finally, the renegotiation should acknowledge that much of the discontent with NAFTA and the USMCA is not about the total number of jobs in the industry, but job quality and persistent wage gaps within the bloc. Currently, the RRM applies only to Mexico. The parties should agree to make the mechanism trilateral, have all parties (including the U.S.) ratify all International Labor Organization conventions, and make other reforms recommended by the UAW,63 which has some of the most experience with the mechanism. Given the high degree of integration of the three economies’ auto sectors, the parties should consider experimenting with trinational sectoral labor bargaining. The UAW’s experience putting investment commitments into its collective bargaining agreements shows the value of labor unions as industrial policy partners. Moreover, they would restore foreign aid to fund union-capacity building in Mexico. Many of these calls are echoed by other labor unions, progressive advocacy groups, Mexican labor unions, and manufacturers.64

While the Trump administration is unlikely to take up all these reforms of their own initiative, the need for congressional support offers leverage to make the kinds of tough demands that have long characterized North American bargaining in the industry.

Authors

-

Acknowledgements and disclosures

The authors thank Oskar Dye-Furstenberg for excellent research assistance, and John Helveston, Brad Markell, and Rajiv Sicora for their insights.

-

Footnotes

- Michael Wayland, “U.S. auto sales next year expected to be best since 2019,” CNBC, December 18, 2024, https://www.cnbc.com/2024/12/18/2025-us-auto-sales-forecast.html

- Michael Wayland, “Cost and chaos continue to test resiliency of U.S. auto industry,” CNBC, October 20, 2025, https://www.cnbc.com/2025/10/20/tariffs-ford-tesla-gm-auto-industry-chaos.html

- José Zozaya and Odracir Barquera, “North America and the Automotive Industry Looking Forward,” Brookings, March 6, 2024, https://www.brookings.edu/articles/north-america-and-the-automotive-industry-looking-forward/

- Susan Helper et al., America’s Retreat in EVs: Economic Security, Prosperity, and the Industrial Future (Technology, Competitiveness, and Industrial Policy [TCIP] Study; Berkeley Roundtable on the International Economy [BRIE], November 9, 2025), https://brie.berkeley.edu/sites/default/files/publications/retreat.pdf

- Dimitry Anastakis, Auto Pact: Creating a Borderless North American Auto Industry, 1960-1971 (University of Toronto Press, 2005).

- Kenneth E. Sharpe and Douglas C. Bennett, Transnational Corporations versus the State: The Political Economy of the Mexican Auto Industry (Princeton University Press, 1985).

- Timothy J. Minchin, America’s Other Automakers: A History of the Foreign-Owned Automotive Sector in the United States, Since 1970: Histories of Contemporary America (University of Georgia Press, 2021), 20, 53. State governors hosting these so-called “transplants” also advocated against local content requirements and unions. Ibid, at 80.

- The White House, Office of the Press Secretary, “Remarks by President Clinton, President Bush, President Carter, President Ford, and Vice President Gore in Signing of NAFTA Side Agreements,” September 14, 1993, https://clintonwhitehouse6.archives.gov/1993/09/1993-09-14-remarks-by-clinton-and-former-presidents-on-nafta.html

- Clemente Ruiz Durán, “Mexico’s Participation in the North American Automotive Manufacturing Industry,” in The North American Auto Industry since NAFTA, ed. Greig Mordue and Dimitry Anastakis (Toronto: University of Toronto Press, 2024), 86–101, https://doi.org/10.3138/9781487527389

- Jorge Carreto Sanginés et al., “Mexico’s Automotive Industry: A Success Story?,” Institute for New Economic Thinking Working Paper no. 166 (October 5, 2021), https://www.ineteconomics.org/uploads/papers/WP_166-Simonazzi-et-al.pdf

- U.S. International Trade Commission, USMCA Automotive Rules of Origin: Economic Impact and Operation, 2025 Report, Publication no. 5642 (Washington, DC: U.S. International Trade Commission, 2025), 143, https://www.usitc.gov/publications/332/pub5642.pdf

- Kate Bronfenbrenner, Uneasy Terrain: The Impact of Capital Mobility on Workers, Wages, and Union Organizing (Washington, DC: U.S. Trade Deficit Review Commission, 2000), https://ecommons.cornell.edu/server/api/core/bitstreams/e433b22a-cab8-438b-a779-761d5892acdd/content. Zachary Schaller, “The Decline of U.S. Labor Unions: Import Competition and NLRB Elections,” Labor Studies Journal 48, no. 1 (2023): 5–34, https://doi.org/10.1177/0160449X221126534

- Susan Helper and Rebecca Henderson, “Management Practices, Relational Contracts, and the Decline of General Motors,” Journal of Economic Perspectives 28, no. 1 (Winter 2014): 49–72, https://www.aeaweb.org/articles?id=10.1257/jep.28.1.49

- Donald J. Trump (@realDonaldTrump), “I will renegotiate NAFTA. If I can’t make a great deal, we’re going to tear it up. We’re going to get this economy running again. #Debate,” Twitter, October 19, 2016, https://twitter.com/realdonaldtrump/status/788919099275390976

- The Biden administration released the report in 2021 in response to congressional demands. See Doug Palmer, “Commerce Releases Trump-Era Report Justifying Auto Tariffs on National Security Grounds,” POLITICO, July 7, 2021, https://www.politico.com/news/2021/07/07/commerce-trump-era-report-auto-tariffs-498531.

- Office of the United States Trade Representative, “United States Announces Deal with Canada and Mexico to Lift Retaliatory Tariffs,” May 17, 2019, https://ustr.gov/about-us/policy-offices/press-office/press-releases/2019/may/united-states-announces-deal-canada-and

- Congressional Research Service, “USMCA: Automotive Rules of Origin,” In Focus IF12082 (updated December 6, 2024), https://www.congress.gov/crs-product/IF12082

- U.S. International Trade Commission, USMCA Automotive Rules of Origin: Economic Impact and Operation, 2025 Report, Publication no. 5642 (Washington, DC: U.S. International Trade Commission, 2025), https://www.usitc.gov/publications/332/pub5642.pdf

- Ed Gresser, “Trade Fact of the Week: U.S. Auto Production Unchanged since ‘USMCA’ Replaced ‘NAFTA’ in 2020,” Progressive Policy Institute, May 15, 2024, https://www.progressivepolicy.org/trade-fact-of-the-week-u-s-auto-production-unchanged-since-usmca-replaced-nafta-in-2020

- U.S. International Trade Commission, USMCA Automotive Rules of Origin: Economic Impact and Operation, 2025 Report, Publication no. 5642 (Washington, DC: U.S. International Trade Commission, 2025), 143, https://www.usitc.gov/publications/332/pub5642.pdf

- U.S. International Trade Commission, USMCA Automotive Rules of Origin: Economic Impact and Operation, 2025 Report (corrected August 2025), Investigation No. 332-600, USITC Publication 5642 (Washington, DC: USITC, July 2025), 60, https://www.usitc.gov/publications/332/pub5642.pdf

- Kathleen Claussen and Chad P. Bown, “Corporate Accountability by Treaty: The New North American Rapid Response Labor Mechanism,” American Journal of International Law 118, no. 1 (2024): 98–119, https://doi.org/10.1017/ajil.2023.64.

- The Brookings Institution, “USMCA Tracker: Disputes,” https://www.brookings.edu/articles/usmca-trade-tracker/#/disputes

- Office of the United States Trade Representative, “Fact Sheet: USMCA Rapid Response Mechanism Delivers for Workers,” September 4, 2024, https://ustr.gov/about-us/policy-offices/press-office/fact-sheets/2024/september/fact-sheet-usmca-rapid-response-mechanism-delivers-workers; Independent Mexico Labor Expert Board, Report (report to the Interagency Labor Committee and the U.S. Congress pursuant to Section 734 of the United States–Mexico–Canada Agreement Implementation Act, P.L. 116-113), October 6, 2025, PDF, https://aflcio.org/sites/default/files/2025-10/IMLEB_REPORT_2025_10_06.pdf

- Brad W. Setser, “Will China Take Over the Global Auto Industry?,” Council on Foreign Relations, December 8, 2024, https://www.cfr.org/articles/will-china-take-over-global-auto-industry

- Susan Helper et al., America’s Retreat in EVs: Economic Security, Prosperity, and the Industrial Future (Technology, Competitiveness, and Industrial Policy [TCIP] Study; Berkeley Roundtable on the International Economy [BRIE], November 9, 2025), https://brie.berkeley.edu/sites/default/files/publications/retreat.pdf

- Nicholas E. Buffie and Donald J. Marples, “Clean Vehicle Tax Credits,” CRS In Focus IF12600 (Washington, DC: Congressional Research Service, December 26, 2024), https://www.congress.gov/crs-product/IF12600

- Office of the Parliamentary Budget Officer, “Tallying Government Support for EV Investment in Canada,” May 9, 2025, https://www.pbo-dpb.ca/en/additional-analyses–analyses-complementaires/BLOG-2425-004–tallying-government-support-ev-investment-in-canada–bilan-aide-gouvernementale-investissement-dans-ve-canada

- MBN Staff, “Mexico’s Electric Vehicle Revolution: Update 2025,” Mexico Business News, May 28, 2025, https://mexicobusiness.news/automotive/news/mexicos-electric-vehicle-revolution-update-2025

- Roosevelt Institute analysis of Department of Energy data. Note the original Build Back Better Act passed by the US House of Representatives in 2021 was even more ambitious, including a “union premium” for consumers that bought union-made cars – a provision that foreign diplomats and producers teamed up with Sen. Joe Manchin to kill, as one of us noted in 2023 commentary for Brookings.

- The White House, “Fact Sheet: President Biden Takes Action to Protect American Workers and Businesses from China’s Unfair Trade Practices,” May 14, 2024, https://bidenwhitehouse.archives.gov/briefing-room/statements-releases/2024/05/14/fact-sheet-president-biden-takes-action-to-protect-american-workers-and-businesses-from-chinas-unfair-trade-practices/

- China Surtax Order (2024), SOR/2024-187, Canada Gazette, Part II, vol. 158, no. 21 (October 9, 2024), https://gazette.gc.ca/rp-pr/p2/2024/2024-10-09/html/sor-dors187-eng.html

- S&P Global Ratings, “Mexican Tariffs: A Speedbump to Chinese Auto Firms’ Overseas Expansion,” S&P Global Ratings (Regulatory), September 17, 2025, https://www.spglobal.com/ratings/en/regulatory/article/mexican-tariffs-a-speedbump-to-chinese-auto-firms-overseas-expansion-s101645512

- As this chapter went to press, Canada struck a deal with China to allow some Chinese EVs to enter Canada in exchange for lower Chinese tariffs on some Canadian exports. From press reports, it was not immediately clear what impact this would have on USMCA negotiations.

- U.S. Census Bureau, “Total Construction Spending: Manufacturing in the United States (TLMFGCONS),” FRED, Federal Reserve Bank of St. Louis, https://fred.stlouisfed.org/series/TLMFGCONS

- For more on these policies and impacts, see Todd N. Tucker, The New US Trade Agenda: Institutionalizing Middle-Out Economics in Foreign Commercial Policy (Roosevelt Institute, 2024), https://rooseveltinstitute.org/publications/the-new-us-trade-agenda/.

- “Proclamation 10896—Adjusting Imports of Steel Into the United States,” February 10, 2025, The American Presidency Project, https://www.presidency.ucsb.edu/documents/proclamation-10896-adjusting-imports-steel-into-the-united-states

- Canada Border Services Agency, “Customs Notice 25-11: United States Surtax Order (Steel and Aluminum 2025),” March 13, 2025, https://www.cbsa-asfc.gc.ca/publications/cn-ad/cn25-11-eng.html.

- “Proclamation 10908—Adjusting Imports of Automobiles and Automobile Parts Into the United States,” March 26, 2025, published in Federal Register 90 (April 3, 2025): 14705–14714, https://www.govinfo.gov/app/details/FR-2025-04-03/2025-05930

- Joshua P. Meltzer, “The Impact of U.S. Tariffs on North American Auto Manufacturing and Implications for USMCA,” Brookings, May 13, 2025, https://www.brookings.edu/articles/the-impact-of-us-tariffs-on-north-american-auto-manufacturing-and-implications-for-usmca/

- On October 17, this tariff regime was extended to medium and heavy-duty trucks and buses. Separately, while the US Supreme Court may dial back the controversial IEEPA tariffs, it is unlikely to rule against actions taken under the long court-approved Section 232. Indeed, it is expected that the Trump administration will rely more heavily on Section 232 to replicate the effects of its current tariffs.

- Canada Border Services Agency, “Customs Notice 25-15: United States Surtax Order (Motor Vehicles 2025),” April 9, 2025, https://www.cbsa-asfc.gc.ca/publications/cn-ad/cn25-15-eng.html.

- American Automotive Policy Council, “Comment Details” (submission to Office of the United States Trade Representative public comments portal, RID XK932MXVTR), USTR Comments Portal, https://comments.ustr.gov/s/commentdetails?rid=XK932MXVTR

- Shane Londagin, Avi Zevin, Luke Bassett, and the REPEAT Project, “A Brief Overview of Major US Clean Energy Tax Policy (2005–2025)” (PDF, n.d.), https://roar-assets-auto.rbl.ms/files/83728/Brief%20Overview%20of%20Major%20US%20Clean%20Energy%20Tax%20Policy%20(1).pdf

- “Electric Vehicles Are in Trouble After Trump Killed Tax Credits,” MSN, https://www.msn.com/en-us/autos/news/electric-vehicles-are-in-trouble-after-trump-killed-tax-credits/ar-AA1QuNFj

- Rachel Frazin, “Companies Hit the Brakes on EVs, Laying Off Thousands of Workers,” The Hill, n.d., https://thehill.com/policy/energy-environment/5589084-evs-electric-vehicles-tax-credits-layoffs-gm-cox-rivian/.

- For now, the producer-specific subsidies for EV supply chains are still in effect.

- Jael Holzman, “How Manchin Kneecapped the Climate Bill’s EV Tax Credit,” E&E News (POLITICO), August 8, 2022, https://www.eenews.net/articles/how-manchin-kneecapped-the-climate-bills-ev-tax-credit/.

- Susan Helper et al., America’s Retreat in EVs: Economic Security, Prosperity, and the Industrial Future (Technology, Competitiveness, and Industrial Policy [TCIP] Study; Berkeley Roundtable on the International Economy [BRIE], November 9, 2025), 15, https://brie.berkeley.edu/sites/default/files/publications/retreat.pdf

- Independent Mexico Labor Expert Board, Report (October 6, 2025), submitted to the Interagency Labor Committee and the U.S. Congress pursuant to § 734 of the United States–Mexico–Canada Agreement Implementation Act (P.L. 116-113), https://aflcio.org/sites/default/files/2025-10/IMLEB_REPORT_2025_10_06.pdf.

- Charles F. Sabel and David G. Victor, Fixing the Climate: Strategies for an Uncertain World (Princeton University Press, 2022).

- Diana E. Páez, “Staying in the Fast Lane: Why North America Can’t Afford to Slow Down on Electric Vehicles,” Brookings, March 5, 2025, https://www.brookings.edu/articles/staying-in-the-fast-lane-why-north-america-cant-afford-to-slow-down-on-electric-vehicles/.

- Sierra Club, “Comment Details” (submission to Office of the United States Trade Representative public comments portal, RID BKH7GWJM8J), USTR Comments Portal, https://comments.ustr.gov/s/commentdetails?rid=BKH7GWJM8J

- This would expand upon the model of Clean Air Act enforcement in the U.S., where facilities are barred from emitting pollutants above certain levels, and subject to monitoring and fines to ensure compliance. For present gaps, see Claire Ewing et al., “Patterns of Air Pollution Enforcement in Canada: Environmental Priorities versus Enforcement Outcomes,” Elementa: Science of the Anthropocene 12, no. 1 (2024): 00062, https://doi.org/10.1525/elementa.2023.00062.

- Climate Leadership Council, “Comment Details” (submission to Office of the United States Trade Representative public comments portal, RID QGT9DHH7WH), USTR Comments Portal, https://comments.ustr.gov/s/commentdetails?rid=QGT9DHH7WH

- U.S. Department of Commerce, Bureau of Industry and Security, “Connected Vehicles (CV),” January 14, 2025, https://www.bis.gov/connected-vehicles.

- MBN Staff, “BYD Hits 80,000 Sales, Ranks Fourth in Mexico’s Auto Market,” Mexico Business News, August 14, 2025, https://mexicobusiness.news/automotive/news/byd-hits-80000-sales-ranks-fourth-mexicos-auto-market.

- “BYD’s Plans to Build a Mexican EV Factory Are Back On, Company VP Hints,” Mexico News Daily, November 13, 2025, https://mexiconewsdaily.com/business/byds-plans-to-build-a-mexican-ev-factory/.

- Keith Bradsher, “China Has Paid a High Price for Its Dominance in Rare Earths,” New York Times, July 5, 2025, https://www.nytimes.com/2025/07/05/business/china-rare-earth-environment.html.

- Susan Helper et al., America’s Retreat in EVs: Economic Security, Prosperity, and the Industrial Future (Technology, Competitiveness, and Industrial Policy [TCIP] Study; Berkeley Roundtable on the International Economy [BRIE], November 9, 2025), https://brie.berkeley.edu/sites/default/files/publications/retreat.pdf

- American Automotive Policy Council, “Comment Details” (submission to Office of the United States Trade Representative public comments portal, RID XK932MXVTR), USTR Comments Portal, https://comments.ustr.gov/s/commentdetails?rid=XK932MXVTR.

- United Auto Workers, “Comment” (submission to Office of the United States Trade Representative, docket USTR-2025-0004; CAT 12370), November 4, 2025, PDF, https://uaw.org/wp-content/uploads/2025/11/USTR-2025-0004-00122247-CAT-12370-Public-Document_110425.pdf.

- United Auto Workers, “Comment” (submission to Office of the United States Trade Representative, docket USTR-2025-0004; CAT 12370), November 4, 2025, PDF, https://uaw.org/wp-content/uploads/2025/11/USTR-2025-0004-00122247-CAT-12370-Public-Document_110425.pdf.

- Labor Advisory Committee, “Comment Details” (submission to Office of the United States Trade Representative public comments portal, RID WBP29Y7GR6), USTR Comments Portal, https://comments.ustr.gov/s/commentdetails?rid=WBP29Y7GR6; International Association of Machinists and Aerospace Workers, “Comment Details” (submission to Office of the United States Trade Representative public comments portal, RID X3CRV3CJQC), USTR Comments Portal, https://comments.ustr.gov/s/commentdetails?rid=X3CRV3CJQC; BlueGreen Alliance, “Comment Details” (submission to Office of the United States Trade Representative public comments portal, RID DQBKCJBX2G), USTR Comments Portal, https://comments.ustr.gov/s/commentdetails?rid=DQBKCJBX2G; Consejo Nacional Laboral, “Comment Details” (submission to Office of the United States Trade Representative public comments portal, RID MTFW2DRYY4), USTR Comments Portal, https://comments.ustr.gov/s/commentdetails?rid=MTFW2DRYY4; Mexican Association of the Automotive Industry (AMIA), “Comment Details” (submission to Office of the United States Trade Representative public comments portal, RID 7JY3CJTQTK), USTR Comments Portal, https://comments.ustr.gov/s/commentdetails?rid=7JY3CJTQTK

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).