Artificial intelligence (AI) is used in a wide variety of products and services, including maps embedded on our smart phones and “chat bots” that help answer our questions on websites. Many hope that AI will transform our economy in ways that drive growth, similar to how steam engines did in the late 19th century and electricity did in the early 20th century. But it is hard to imagine that maps on smart phones, chatbots, and other existing AI-enabled services will drive the type of economic growth we saw from stream and electricity. What we need to see are some dramatic new AI-enabled products and services that transform our way of life—in short, we are waiting for an AI “killer app.”

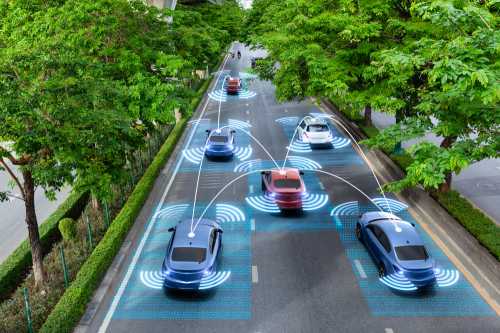

Autonomous vehicles (AVs)—vehicles that accelerate, brake, and turn on their own, requiring little or no input from a human driver—may be such a killer app that transforms our economy significantly. AI supports AVs in a variety of ways, including quickly processing and interpreting the large amounts of data generated by the vehicle’s cameras and sensors and helping to improve vehicle fuel efficiency and safety. The impacts of broad adoption of AVs are equally numerous, from potentially lowering transportation costs by limiting the need for drivers to possibly transforming mobility in urban and suburban environments. While the relative timing and scale of economic growth is not yet clear—and subject to some debate among scholars—a key step in maximizing the benefits of AVs is passing federal legislation, rather than relying on a patchwork of state and local guidelines. To inform the debate and help prepare policymakers for the task at hand, this report will examine the state of AVs, the potential for them to become a “killer app” with broad impacts, and the existing and potential regulations that could ensure net positive effects on the economy and society as a whole.

The current state and future of AVs

The current standards for autonomous driving were developed by the Society of Automotive Engineers (SAE International). According to the SAE standard, the automation capability of vehicles ranges from Level 0, with no autonomy, to Level 5, which is full automation. Level 1 features include park assist, lane assist and adaptive cruise control. Some Level 3 vehicles, which include full self-driving capabilities but require human intervention in complex situations such as traffic jams, may be commercially available in 2021. No Level 4 or 5 cars, which would not require any human intervention, are yet certified for use on regular roads, though there are some such as Google’s Waymo that are in development.

While the potential impacts of AVs are substantial, it will take time for them to be realized; AVs are still some years from being commercially available, let alone in widespread use. To give a reasonable sense of timing, Chris Urmson—a DARPA challenge winner, head of Google’s Waymo autonomous vehicle unit for many years, and now CEO of a self-driving vehicle software company named Aurora —argues it may take up to 30 to 50 years before widespread adoption of autonomous vehicles. Despite predictions to the contrary—e.g., Elon Musk’s 2019 prediction that there would be a Tesla driverless taxi fleet in some regions by 2020—time frames of this magnitude are common in the automobile industry. Choe, Oettl and Seamans (2021) report that widespread adoption of new innovations in the automobile sector historically can take several decades.1 There are a number of factors that contribute to technology adoption, and even if a new technology is feasible, it may not be available at a price point that many consumers will pay. For example, turbo-charged engines, which help to reduce the amount of fuel needed, did not start to become popular until oil prices started to rise in the 1970s.

In short, the timing of adoption of AVs and the economic impacts that will follow depend on many factors. For regulators and policymakers interested in shaping what will likely be considerable economic and societal impacts of AVs, now is the time.

Effect on our economy and society

Supporters of autonomous vehicles argue that they may provide a variety of benefits including fuel efficiency and safety. Indeed, the Brookings Institution recently published a book on the topic (Winston and Karpilow, 2020).2 The U.S. Energy Information Administration (EIA) argues that AVs are more fuel efficient than human-driven cars, which means fewer emissions. However, AVs may increase vehicle traffic, potentially nullifying emissions reduction from fuel efficiency. Kroger, Kuhnimhof, and Trommer (2019) project the adoption of autonomous vehicle technologies may increase vehicle traffic by 2-9 percent as a result of new automobile user groups as well as lower generalized costs of car travel.3

AVs will likely be safer than human-driven cars, in large part through reducing human error which the National Highway Traffic Safety Association (NHTSA) estimates accounts for 94 percent of crashes. While widespread adoption of AVs should ultimately result in safer roads, there have been several high profile accidents involving AVs, such as a Waymo van that crashed into a car in Arizona. Perhaps as a result of some of these high-profile accidents, consumer demand for AVs seems to be relatively low. According to a 2021 survey by the American Automobile Association, only 14 percent of drivers report that they would trust riding in a vehicle that drives itself, a response similar to the 2020 survey. It is possible, however, that consumer attitudes will change once Level 4 and 5 vehicles become commercially available.

AVs may help to reduce labor input costs in driving-intensive industries. However, as Gittleman and Monaco (2017) point out, there are several types of drivers, and autonomous driving will likely affect some types more than others.4 Autonomous vehicles are more likely to be used for heavy and tractor trailer truck purposes (aka “long haul”) than local delivery given the relative ease of navigating on highways and all the other tasks associated with local delivery, including freight handling, paperwork, and customer service. Gittleman and Monaco estimate that Level 4 and 5 automation may ultimately displace 300,000 to 400,000 drivers. But the authors highlight that there are many practical limitations to automation. For example, they highlight that one of the important functions of a truck driver is to serve as a security guard for the freight.

A recent paper by Gelauff, Ossokina, and Teulings (2019) envisions some of the longer-term outcomes from AVs.5 The authors model two countervailing effects from AVs, each of which lead to differing outcomes on population distribution. On one hand, AVs may lead to improved use of time during car trips, which lowers the cost of living at a distance from cities. On the other hand, AVs may lead to improved public transit options in urban environments in the form of shared-ride autonomous vehicles (SAVs). The authors argue that SAVs may be more efficient than existing public transit and may make city living relatively more attractive leading to more population clustering in cities. The authors argue that the second effect may outweigh the first and ultimately may lead to overall population shifts towards large, attractive cities at the expense of smaller urban and non-urban areas. While the authors don’t speculate on the ultimate economic effects of such a change, it is worth noting that literature from economic geography suggests that there are many agglomeration effects from living in or close to cities, including greater economic growth and innovation.6 It is also worth noting that the COVID-19 pandemic has led to a large shift in population away from many urban environments, at least in the short run.

In short, AVs will likely affect our economy and society in a variety of ways. AVs may lead to fewer emissions and increased safety. By decreasing the need for humans to drive, AVs will likely transform the type of work done by humans in the transportation sector of the economy and may also change the way that humans commute to and from work. How all this plays out, however, depends on numerous factors including, importantly, existing and future regulations.

Current and prospective AV legislation

The National Conference of State Legislatures highlights that a number of states have introduced and enacted laws related to autonomous vehicles. Notably, in December 2020, California State Senator Ben Allen introduced a bill to establish a new Council on the Future of Transportation in California that would promote state legislation for autonomous vehicles, in addition to other transportation-related policy. Also, in November 2020 the California Public Utilities Commission approved autonomous vehicle regulatory framework that would make it easier for companies to provide autonomous vehicle transportation services to the public. While these laws indicate that state legislators are responsive to local concerns about autonomous vehicles, the risk is a resulting patchwork of state laws.

With this concern in mind, there have been attempts at federal legislation, notably in 2017 with the SELF DRIVE Act in the House and the AV START Act in the Senate. The SELF DRIVE Act (Safely Ensuring Lives Future Deployment and Research In Vehicle Evolution Act) was passed in the House in 2017 but did not advance in the Senate. The bill would have provided NHTSA with the authority to regulate AVs. NHTSA would be authorized to require safety assessment certifications and states would be preempted from enacting laws regarding the design, construction, or performance of AVs unless those laws enact standards identical to federal standards. In addition, the bill would have required that manufacturers of AVs develop written cybersecurity and privacy plans for such vehicles prior to offering them for sale. The AV START Act (American Vision for Safer Transportation through Advancement of Revolutionary Technologies Act) was introduced in the Senate in 2017 but did not advance. Like the SELF DRIVE Act, it would have established a framework for a federal role in oversight of AVs, preempting state laws and providing clarity to stakeholders including car manufacturers and insurance companies.

Related Content

2016

It remains to be seen when federal legislation on AVs will be passed, although there are promising signs. Reportedly, there is currently bipartisan support for federal legislation, notably from Republican Senator John Thune and Democratic Senator Gary Peters (who were co-sponsors of the AV START Act). While the Biden administration did not mention autonomous vehicles in its recently proposed infrastructure and jobs plan (instead focusing on electric vehicles and charging stations), Transportation Secretary Pete Buttigieg has stated, “Automated vehicle technology is coming, it’s advancing very quickly, it is something that holds the potential to be transformative, and I think in many ways policy has not kept up.”

Existing regulatory barriers: Spectrum

One important issue to be resolved is around communication standards between autonomous vehicles. The 5.9 GHz spectrum, a 75 MHz band, had initially been set aside for use for vehicle-to-vehicle (V2V) communications in 1999, and NHTSA, car manufacturers, and device manufacturers spent the ensuing two decades working on a standard for V2V communications. However, the standard that emerged, called Dedicated Short-Range Communications (DSRC), continues to face considerable resistance, including from a competing standard called Cellular-Vehicle-to-Vehicle (C-V2V). DSRC allows direct communication between two DSRC-enabled devices without relying on an intermediary, such as a cellular network, which in principle makes it fast and deployable in areas without cellular coverage. However, research by Gyawali et al (2020) suggests that DSRC only works well when two vehicles are in sight of each other and not moving too fast.7C-V2V operates through a cellular network, which may limit its ability to function well in remote areas but handles communications between vehicles that are moving quickly (Gyawali et al 2020).

Separately, Wi-Fi demands have been growing, and the 5.9 GHz spectrum is increasingly being used for unlicensed Wi-Fi. A 2018 study by Rand Corporation estimated that the value of the consumer and producer surplus from using the entire band for Wi-Fi to be between $82.2 billion and $189.9 billion. In November 2019 Federal Communications Commission (FCC) Chairman Ajit Pai announced a plan whereby 45 MHz at the lower end of the band will be made available for Wi-Fi, the next 20 MHz for C-V2V, and the top 10 MHz potentially for C-V2V or DSRC. In November 2020 the FCC voted in favor of the proposal, despite objections by the Trump administration’s Department of Transportation. There are calls for the Biden administration to reverse the FCC’s decision. The plan would seem to bolster the C-V2V standard relative to DSRC, which may hasten resolution of the standards battle, and also favors use of Wi-Fi over transportation. It will be important for policymakers to consider the tradeoffs associated with use of the spectrum. On the one hand, demand for spectrum for Wi-Fi enabled devices is a growing and current need. In contrast, there is currently little need for spectrum for autonomous vehicles—there aren’t any commercially available and consumer demand seems low. On the other hand, spectrum for autonomous vehicles will likely be a future need, and the economic benefits of autonomous vehicles may outweigh the benefits of additional Wi-Fi.

Conclusion

Autonomous vehicles will likely transform our economy, including changing the role of humans in transportation-related industries and potentially reducing emissions and increasing safety, all of which should ultimately lead to economic growth. However, large-scale adoption of autonomous vehicles and the ensuing economic growth will likely take time. The technology is still in development and consumers remain wary of autonomous vehicles. Moreover, federal and state legislation is still nascent, and there are competing standards for communication between vehicles. All of this needs to be resolved before AVs can become a “killer app.”

Editor’s Note: This paper was updated from a previous version to reflect a change in Tesla vehicle’s SAE automation level from 3 to 2.

The authors did not receive financial support from any firm or person for this article or from any firm or person with a financial or political interest in this article. They are currently not an officer, director, or board member of any organization with an interest in this article.

Author

-

Footnotes

- Choe, D., Oettl, A., & Seamans, R. (2021). What’s Driving Entrepreneurship and Innovation in the Transport Sector? NBER working paper 27284

- Winston, C., & Karpilow, Q. (2020). Autonomous Vehicles: The Road to Economic Growth?. Brookings Institution Press.

- Kröger, L., Kuhnimhof, T., & Trommer, S. (2019). Does context matter? A comparative study modelling autonomous vehicle impact on travel behaviour for Germany and the USA. Transportation research part A: policy and practice, 122, 146-161.

- Gittleman, M., & Monaco, K. (2020). Truck-driving jobs: Are they headed for rapid elimination?. ILR Review, 73(1), 3-24.

- Gelauff, G., Ossokina, I., & Teulings, C. (2019). Spatial and welfare effects of automated driving: Will cities grow, decline or both?. Transportation research part A: policy and practice, 121, 277-294.

- Carlino, G., & Kerr, W. R. (2014). Agglomeration and innovation. https://www.nber.org/papers/w20367

- Gyawali, S., Xu, S., Qian, Y., & Hu, R. Q. (2020). Challenges and Solutions for Cellular based V2X Communications. IEEE Communications Surveys & Tutorials.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).