After reaching $70 a barrel in early 2020, oil prices have plummeted to their lowest levels in 20 years at less than $20 a barrel due to the COVID-19 pandemic and the Saudi-Russian oil price war. This price crash once again demonstrates the perils of excessive economic dependence on natural resource revenues. Oil-dependent countries are bracing for a period of fiscal crisis on top of an ongoing economic shock caused by the COVID-19 pandemic. These effects will be severe in countries like Nigeria, Africa’s largest oil producer, which collects 57 percent of its government revenues and more than 94 percent of export earnings from petrodollars.

A vast body of “resource curse” research has explored the causes and implications of the negative relationship between resource wealth and economic and institutional development. In a new study, we analyzed the political economy of the resource curse to understand what drives economic diversification in resource-rich countries.

Ideally, natural resource revenues should provide a head start for poor countries seeking to develop their economies. Few resource-rich countries, however, have been able to turn their resources in the ground into physical and human capital that can be used to provide prosperity for their citizens. Like Nigeria, most exhibit low levels of economic and export diversification, as natural resources assume a dominant place in export income and government revenues. This in turn makes them vulnerable to economic shocks related to volatile commodity prices.

We looked into the diversification performance of 42 resource-dependent countries that had the highest share of resources in their exports in the 1970s. Between 1981 and 2014, these countries were moderately successful in registering non-resource growth. Initial resource wealth did not seem to have affected non-resource growth in subsequent years. Compared to resource-poor countries, however, these countries have registered slower average growth in services.

To explore policy-related factors that may have enabled successful diversification, we examined a number of potential ingredients: human capital attainment, public and intellectual capital development, and business capacity development. Examining these competitive capabilities can hint to the way resource wealth affects intermediate policy variables that drive economic diversification.

Initial resource wealth is negatively associated with some measures of human capital attainment, R&D and innovation performance, and financial access. In terms of infrastructure stock per person, however, we find a positive relationship. Moreover, this relationship depends on the way resource wealth is measured. Resource dependence (the share of resources in exports or GDP) is negatively associated with many competitive capabilities, whereas resource abundance (resource rents per person) has positive associations with some competitive capabilities.

The most successful diversifiers do not have uniformly high levels of competitive capabilities, and this is particularly the case for extremely resource-dependent countries. Among the relatively successful diversifiers, Chile and Norway—and to some extent Malaysia—have improved their competitive capabilities in most areas.

We looked closely at three countries—Oman, Laos, and Indonesia—that registered the highest level of manufacturing value added growth. Although Oman has the fastest growth rate in our sample, its manufacturing sector today contributes only 10 percent of GDP, and remains concentrated on resource-related activities, suggesting that diversification success remains elusive for countries that start as extremely resource dependent.

The experiences of Indonesia and, to a lesser extent, Laos, suggest that active diversification policies can yield fruitful results under favorable conditions that include access to markets and foreign technologies. In these countries, diversification was kickstarted through a centralized development policy with a stable business-government relationship in the deals environment. However, the domestic value addition of manufacturing in both countries is relatively low, pointing to the limited efficacy of their diversification strategies.

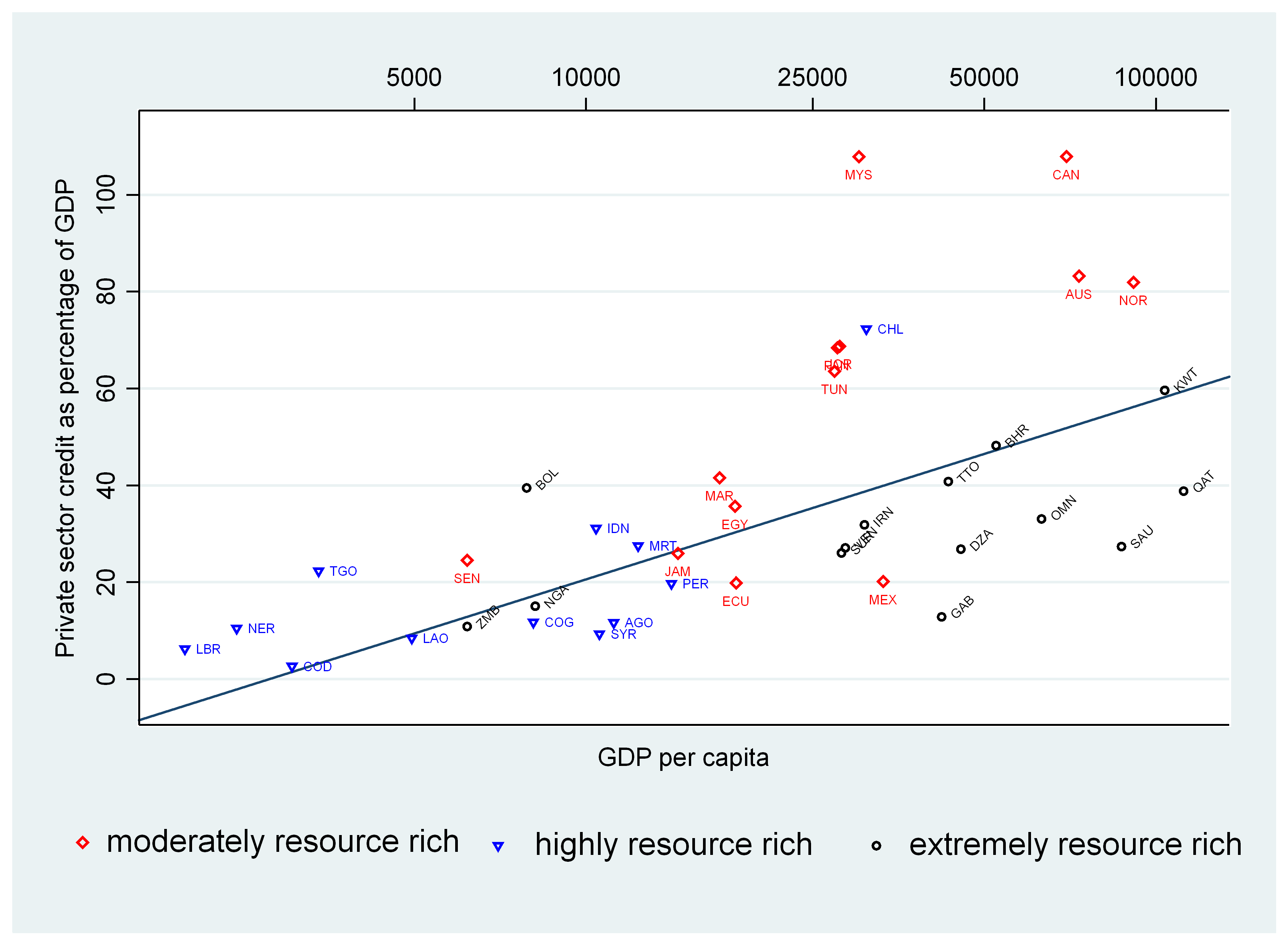

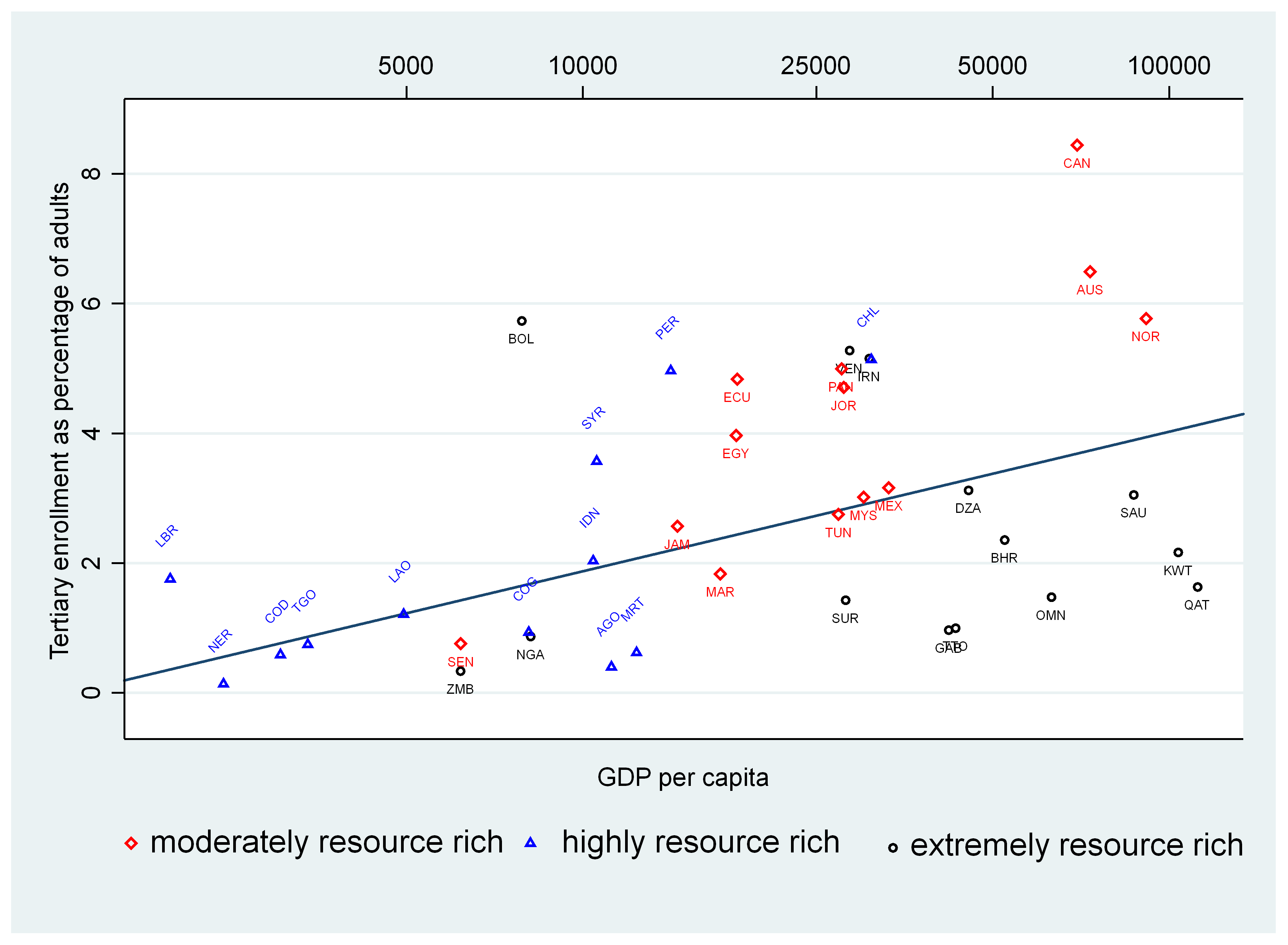

Overall, the results reveal the importance of breaking down the data to identify how economic diversification plays out across different sectors of the economy. The examination of competitive capabilities and the case studies indicate the varied diversification experiences of countries. Among highly resource (oil)-dependent countries, limited overall diversification success seems to persist even when non-resource growth rates are high; those countries have also failed to build competitive capabilities such as credit access (Figure 1) and higher education (Figure 2) given their income levels.

Relatively successful diversification in other less resource-dependent countries has been stimulated by different internal and external drivers, and builds on natural endowments (e.g., agribusiness and labor-intensive manufacturing in Indonesia). Countries also leveraged different types of competitiveness policies and capabilities, with no single formula for success emerging from the sample.

If the current slump in commodity prices persists beyond the COVID-19 crisis, resource-rich countries will need to change gears quickly. The best route is to devise active diversification policies that are tailored to their specific market and institutional conditions.

Figure 1. A scatter plot and linear regression fit of private sector credit against GDP per capita

Figure 2. A scatter plot and linear regression fit of tertiary education enrollment against GDP per capita

Related Content

Related Books

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

As oil prices plummet, how can resource-rich countries diversify their economies?

April 3, 2020