A critical step in building capital markets is to develop the “buy side,” encouraging greater participation by local institutional investors such as pension funds and insurance firms. But limited supply of investment vehicles can be a major challenge to developing the buy side in emerging and frontier markets. Findings from a recent survey by the Milken Institute of 44 institutional investors in four East African Community (EAC) countries—Kenya, Rwanda, Tanzania, and Uganda—highlight this unmet demand for more “product,” especially more longer-term investment vehicles. Investors have also expressed a desire for more products designed in a way that better matches their investment aims.

Savings managed by local institutional investors in these countries have nearly doubled in just four years, to about $19 billion by early 2016. Through our survey, we wanted to learn how these investors manage these growing savings across asset classes and countries—gauging whether and how they are diversifying their portfolios. We also asked institutional investors in these countries about the kinds of financial instruments they would have appetite for, if they were to become available in future.

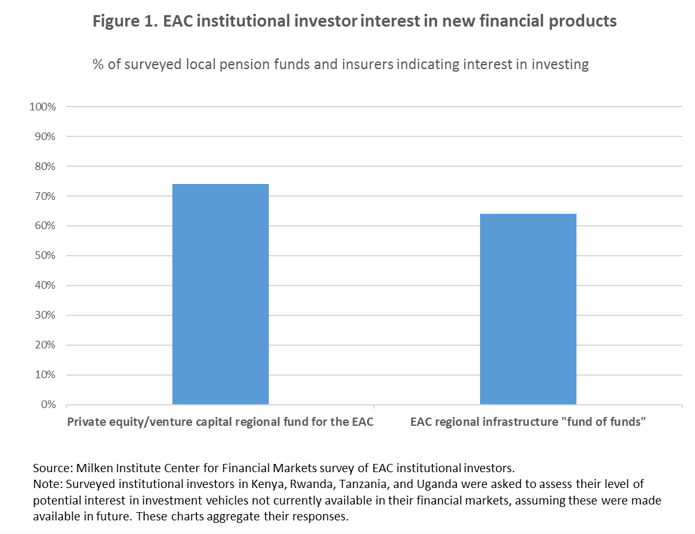

As many as three-quarters of surveyed institutional investors in the EAC said they would be interested in a regional infrastructure “fund of funds” that would invest in cross-border projects in the region (see Figure 1 below). If properly structured and managed, a fund of funds could help investors manage risk and may boost returns by channeling investment into a diverse portfolio of infrastructure projects across the EAC region. A fund of funds could be structured to pool resources of individual institutional investors in East Africa and invest in cross-border transport and energy projects.

Nearly two-thirds of institutional investors we surveyed in East Africa said they also would have strong appetite for a private equity/venture capital (PE/VC) regional fund—despite the fact that the small size of local capital markets generally means investors can find it difficult to exit and get other investors to take up stakes. An intraregional fund of funds investing specifically in PE/VC in the EAC could facilitate the ability of investors to diversify into this new asset class, while also managing some of the associated risk. By channeling some investment in PE/VC through this kind of vehicle as part of a balanced, well-managed portfolio, institutional investors may be able to generate higher returns. At the same time, it will be important for investors, as well as regulators and financial intermediaries, to boost their risk-evaluation capacity—and for financial market supervisory authorities in the EAC to further clarify evolving regulations for investors.

The EAC’s rapidly growing pension funds in particular would benefit from the opportunity to diversify their portfolios and invest in a pipeline of investible, well-managed projects.

This kind of regional approach to developing investment vehicles for the “buy side” could help develop the very small institutional investor base in countries such as Rwanda. The EAC’s rapidly growing pension funds in particular would benefit from the opportunity to diversify their portfolios and invest in a pipeline of investible, well-managed projects. Designing investment vehicles that are better geared to the needs and constraints of institutional investors in east Africa could help unlock more of this finance to develop infrastructure, create jobs, and spur socioeconomic development in the region.

Note: This blog reflects the views of the author only and does not reflect the views of the Africa Growth Initiative.

Commentary

East African institutional investors have strong unmet demand for regional investment funds

March 2, 2017